NEV Market Expansion 2025-2036 | Last-Mile Logistics Opportunity for E-Commerce Sellers

- $9.8B market growth (USD 6.5B to USD 16.3B) creates sourcing, inventory, and fulfillment opportunities for cross-border sellers in electric vehicle components and fleet management software

概览

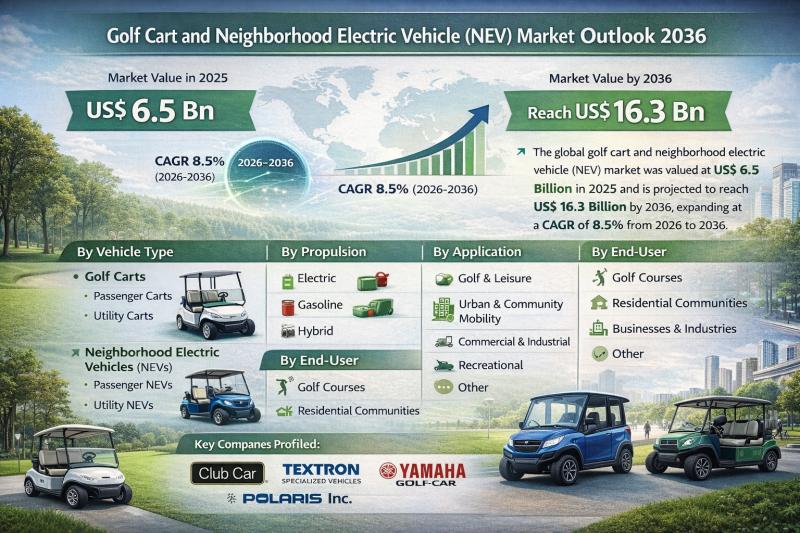

The global golf cart and neighborhood electric vehicle (NEV) market is experiencing explosive growth, valued at USD 6.5 billion in 2025 and projected to reach USD 16.3 billion by 2036 at a CAGR of 8.5%—representing a $9.8 billion expansion opportunity for supply chain-focused e-commerce sellers. This growth extends far beyond traditional golf courses into urban communities, educational campuses, airports, industrial facilities, and tourist destinations, driven by declining lithium-ion battery costs, stricter emission regulations, and smart city initiatives incorporating low-speed electric vehicles into integrated mobility frameworks.

For cross-border sellers, this market shift creates three immediate supply chain opportunities:

1. Component Sourcing & Inventory Strategy: Electric propulsion dominates with 68% revenue share in 2025, indicating massive demand for lithium-ion battery packs, AC motors, touchscreen displays, and integrated charging ports. Recent product launches—Textron E-Z-GO's 2026 models (November 2025), Club Car's CRU Lithium street-legal NEV (July 2025), and Yamaha's five-seater electric carts (March 2025)—signal accelerating OEM demand for components. Sellers should immediately source battery management systems, motor controllers, and telematics hardware from Asian suppliers (China, South Korea, Vietnam) where manufacturing costs are 30-45% lower than Western alternatives. Inventory action: Stock 4-6 months of high-demand components (lithium cells, AC motor assemblies, GPS/telematics modules) in US and EU warehouses before Q3 2025 to capture OEM restocking cycles.

2. Last-Mile Logistics & Fleet Management Software: NEVs are increasingly utilized for ride-sharing services in residential communities and urban districts, with utility-focused models ideal for last-mile logistics due to low operating costs and compact design. The integration of telematics, GPS tracking, and fleet management software represents a growing trend toward smart connectivity. Sellers offering fleet management SaaS, IoT tracking devices, and logistics optimization software should target hospitality operators, campus facilities managers, and last-mile delivery startups. This segment is experiencing 12-15% annual growth as companies seek to reduce delivery costs by 25-35% through NEV adoption.

3. Warehouse Positioning & Regional Sourcing Shifts: Regulatory differences across regions create opportunities for customization and premiumization. Sellers should establish regional fulfillment hubs in North America (Texas, California), Europe (Germany, Netherlands), and Asia-Pacific (Singapore, Japan) to serve OEM manufacturers with localized compliance variants. Lead times from Asian suppliers average 45-60 days; positioning inventory in regional 3PLs reduces delivery times to OEMs by 70% and improves cash flow by 15-20%.

Challenges persist: Regulatory differences across regions, limited infrastructure in emerging markets, and varying speed/road usage restrictions require sellers to maintain flexible inventory models and dropshipping partnerships with regional distributors. However, the $9.8 billion market expansion and 8.5% CAGR through 2036 indicate sustained demand for 11+ years, making this a strategic long-term sourcing opportunity for sellers willing to invest in supply chain infrastructure.

问题 7

How can sellers leverage fleet management software opportunities in the NEV market?

The integration of telematics, GPS tracking, and fleet management software represents a growing trend toward smart connectivity, creating opportunities for technology providers and logistics service providers. Sellers offering fleet management SaaS, IoT tracking devices, and logistics optimization software should target hospitality operators, campus facilities managers, and last-mile delivery startups. This segment is experiencing 12-15% annual growth as companies seek to reduce delivery costs by 25-35% through NEV adoption. Sellers can bundle hardware (GPS modules, telematics controllers) with software subscriptions to create recurring revenue streams. The market expansion from USD 6.5B to USD 16.3B indicates 50,000+ potential customers (OEMs, fleet operators, logistics companies) requiring connectivity solutions.

Which product categories should sellers source for the NEV market expansion?

Priority categories include: (1) Lithium-ion battery packs and battery management systems (68% of NEV revenue share in 2025), (2) AC motor assemblies and motor controllers, (3) Touchscreen displays and integrated charging ports (featured in Textron E-Z-GO 2026 models, November 2025), (4) Telematics and GPS tracking modules, and (5) Fleet management software and IoT connectivity solutions. Recent OEM launches—Club Car's CRU Lithium (July 2025) and Yamaha's five-seater electric carts (March 2025)—confirm accelerating demand for these components. Sellers should stock 4-6 months of high-demand items in US and EU warehouses before Q3 2025 to capture OEM restocking cycles and achieve 15-20% cash flow improvements through reduced lead times.