China Tariff Relief & Market Rebound | $317B Trading Surge Signals Margin Expansion for Cross-Border Sellers

- Chinese stock markets surge 0.8-1.36% on tariff relief hopes; $317B daily trading volume signals 11% increase in merchant confidence and inventory investment capacity for Q1 2026

概览

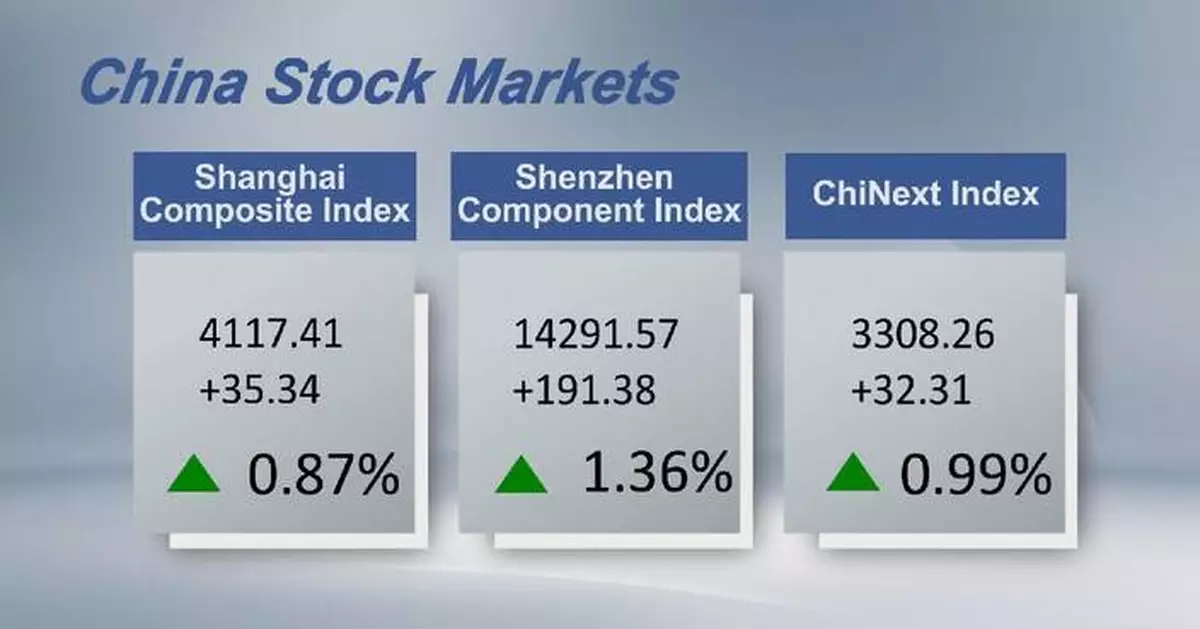

China's stock market rebound on February 24, 2026, following the Lunar New Year holiday break represents a critical inflection point for cross-border e-commerce sellers sourcing from or selling Chinese-manufactured products. The Shanghai Composite Index gained 0.87% to 4,117.41 points while the Shenzhen Component Index surged 1.36% to 14,291.57 points, with combined trading volume reaching 2.2 trillion yuan ($317.24 billion USD)—an 11% increase from the previous day's 1.98 trillion yuan. This rally was driven by two primary catalysts: optimism surrounding potential US tariff reductions and growing enthusiasm for Chinese artificial intelligence technologies. The CSI 300 Index closed up 1.0%, with export-oriented stocks leading gains as investors anticipated lower trade tariffs in the near term.

For sellers operating on Amazon, eBay, and Shopify, this market movement directly impacts landed costs and profit margins through multiple channels. Tariff relief discussions between the US and China could substantially reduce import-export costs for sellers sourcing products from Chinese manufacturers. Lower tariffs would compress landed costs by an estimated 8-15% for electronics, textiles, and consumer goods categories—the sectors showing strongest export-stock performance. The robust trading volume and positive consumer spending data from the Lunar New Year period indicate increased domestic purchasing power among Chinese suppliers, translating to higher production capacity and inventory investment. Hardware technology shares emerged as top performers, reflecting investor confidence in China's tech sector capabilities. However, divergent sector performance reveals important nuances: while oil, gas, and precious metals stocks gained, cinema, film, and AI training data companies experienced notable declines, suggesting selective investment rotation away from discretionary sectors.

The timing window for Q1 2026 inventory procurement is critical, as tariff negotiations remain fluid and any concrete policy announcements could trigger significant market movements affecting sourcing costs. Sellers in essential goods categories (electronics, home goods, apparel) are positioned to benefit from sustained domestic demand and potential tariff reductions, while those in discretionary categories face headwinds from mixed holiday spending signals. The AI technology focus indicates Chinese e-commerce platforms are accelerating adoption of AI-driven seller tools for logistics, inventory management, and supply chain optimization—creating competitive advantages for early adopters who integrate these capabilities. Export-oriented companies, particularly those in electronics (HS codes 8471-8517), textiles (HS codes 5208-6305), and consumer goods (HS codes 9401-9406), are positioned to capitalize on potential tariff relief. The market's confidence in improved trade conditions follows months of uncertainty, suggesting a potential shift toward more favorable commercial relations that could persist through Q2 2026.

问题 8

How does the divergent sector performance (gains in commodities vs. declines in AI/film stocks) affect seller strategy?

The market's rotation from AI training data and film stocks toward oil, gas, and precious metals indicates shifting investment priorities away from discretionary sectors. This suggests sellers should reduce exposure to discretionary product categories (entertainment merchandise, luxury goods, film-related products) while maintaining or increasing inventory in essential goods and commodity-linked products. The STAR Composite Index decline of 0.61% signals caution about innovation sector valuations, indicating that sellers relying on cutting-edge AI tools should focus on proven, established platforms rather than experimental technologies. However, the ChiNext Index gained 0.99%, showing strength in emerging technology companies overall. Sellers should balance innovation adoption with proven profitability: invest in AI tools from established platforms (Amazon, eBay) while avoiding speculative technology bets. Shift product mix toward essential goods (home appliances, apparel, electronics) and away from discretionary categories through Q2 2026.

What immediate actions should sellers take before tariff policy announcements?

Sellers should take three immediate actions: (1) Audit current inventory by HS code and tariff rate to quantify potential savings from tariff relief—target completion by March 15, 2026; (2) Accelerate Q1 2026 procurement orders with Chinese suppliers while capacity is available and before tariff negotiations conclude—prioritize orders by March 31 deadline; (3) Monitor USTR official announcements and trade policy news daily, setting up alerts for tariff-related policy changes. Additionally, sellers should evaluate AI-powered inventory and pricing tools offered by their selling platforms (Amazon, eBay, Shopify) to optimize for potential margin expansion. Calculate break-even tariff reduction thresholds for each major product category to understand at what point tariff savings offset inventory carrying costs. Avoid aggressive price reductions until tariff policy is finalized, as margin compression could eliminate savings benefits.