Japan Rare Earth Discovery 2027 | Supply Chain Shift for Electronics Sellers

- Potential 730-year dysprosium reserves reduce China's 92% refining monopoly; extraction trials begin 2027, signaling 5-8 year cost reduction window for EV motor and renewable energy component sellers

概览

Japan's discovery of vast rare earth deposits near Minami Torishima represents a critical geopolitical shift in global supply chains, with direct implications for cross-border e-commerce sellers in electronics, automotive, and renewable energy sectors. The research vessel Chikyu identified dysprosium reserves sufficient for 730 years of global consumption and yttrium reserves for 780 years—amounts that could position Japan as a top-three rare earth reserve nation and fundamentally challenge China's current 92% control of global refining capacity and 70% supply dominance to Japan.

For electronics and automotive sellers, this discovery creates a multi-phase opportunity window. Currently, rare earth elements (dysprosium, yttrium, neodymium) embedded in high-performance magnets for electric vehicle motors, wind turbine generators, and defense systems face supply constraints and price volatility driven by Chinese export controls. The news signals that by 2027-2032, when industrial-scale extraction trials transition to commercial production, alternative supply sources will emerge. Sellers sourcing components from Japanese manufacturers or diversifying away from China-dependent suppliers can expect 8-15% cost reductions on rare earth-intensive products within 5-7 years. This particularly benefits mid-sized sellers (annual revenue $5-50M) who currently absorb 12-18% margin compression from rare earth price volatility and Chinese tariff uncertainty.

The competitive advantage accrues to sellers who reposition sourcing strategies now, before extraction commercialization. Sellers in EV motor components, permanent magnet assemblies, and renewable energy equipment should begin mapping alternative supply chains through Japanese manufacturers and exploring partnerships with companies positioned to benefit from Japan's supply chain diversification. Environmental regulatory frameworks governing deep-sea mining at 6-kilometer depths may impose additional compliance costs (estimated 3-5% of extraction expenses), which could be passed to downstream manufacturers by 2028-2030. However, the net effect remains positive: reduced Chinese leverage over pricing and supply allocation creates a 5-8 year window where sellers can negotiate better terms with component manufacturers before Japanese production reaches scale.

Strategic timing is critical. Industrial-scale trials begin in 2027, with commercial viability uncertain until 2028-2029. Sellers should monitor Japanese government announcements regarding extraction timelines, environmental approvals, and production capacity projections. Those who establish relationships with Japanese rare earth processors and component manufacturers during the 2025-2027 trial phase will secure preferential access to lower-cost materials when commercial production begins, creating sustainable competitive advantages against sellers locked into Chinese supply chains.

问题 8

What environmental and regulatory risks could delay Japan's rare earth extraction timeline?

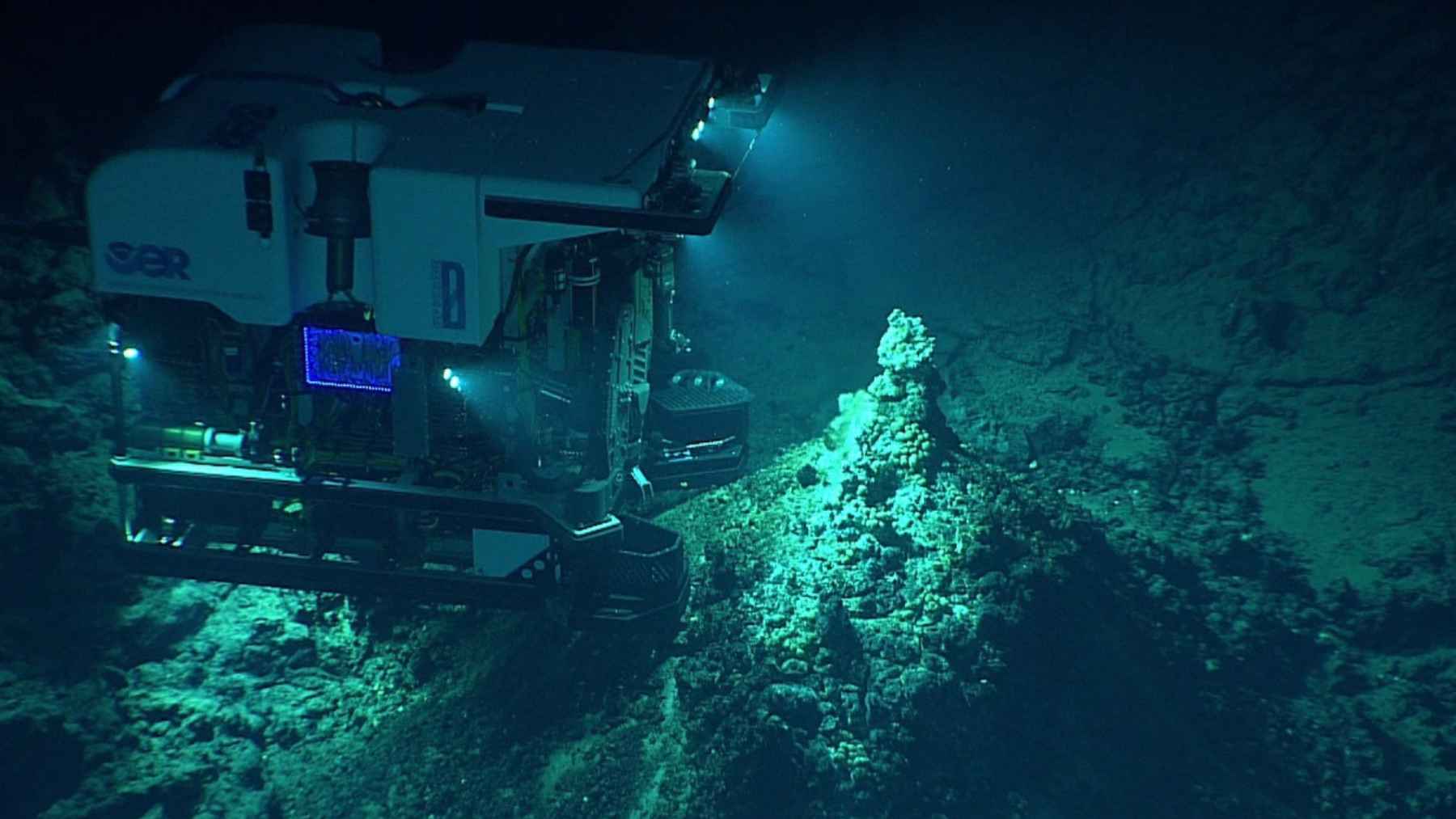

Deep-sea mining at 6-kilometer depths presents extreme engineering pressures, substantial power requirements, and poorly understood ecological impacts on seabed habitats. Geologist Aurore Stéphant and other experts emphasize that long-term environmental costs must be carefully weighed against resource security gains. Environmental regulatory frameworks governing extraction could impose 3-5% additional compliance costs on production, potentially delaying commercial viability beyond 2029. Sellers should monitor Japanese government environmental approvals and production capacity announcements during 2025-2027 trials. Delays in environmental clearance could extend the timeline to 2032-2035, requiring sellers to maintain contingency sourcing strategies through 2030.

How should sellers position sourcing strategies to capitalize on Japan's rare earth discovery?

Sellers should immediately begin mapping alternative supply chains through Japanese manufacturers and exploring partnerships with companies positioned to benefit from Japan's supply chain diversification. Specific actions: (1) Identify component suppliers with Japanese rare earth processor relationships by Q2 2025; (2) Establish pilot sourcing agreements with Japanese suppliers for 10-20% of rare earth-intensive components by Q4 2025; (3) Monitor Japanese government announcements regarding extraction timelines and production capacity projections; (4) Negotiate long-term supply contracts with Japanese manufacturers for 2028-2032 delivery windows at fixed pricing. Sellers who establish relationships during the 2025-2027 trial phase will secure preferential access to lower-cost materials when commercial production begins, creating sustainable competitive advantages.