Wholesale Inflation Surge & Energy Shock | Cross-Border Seller Cost Crisis

- PPI hits 3-year high at 4.0% annually; jet fuel +30.7%, diesel +42% impact logistics costs for 50K+ sellers

Overview

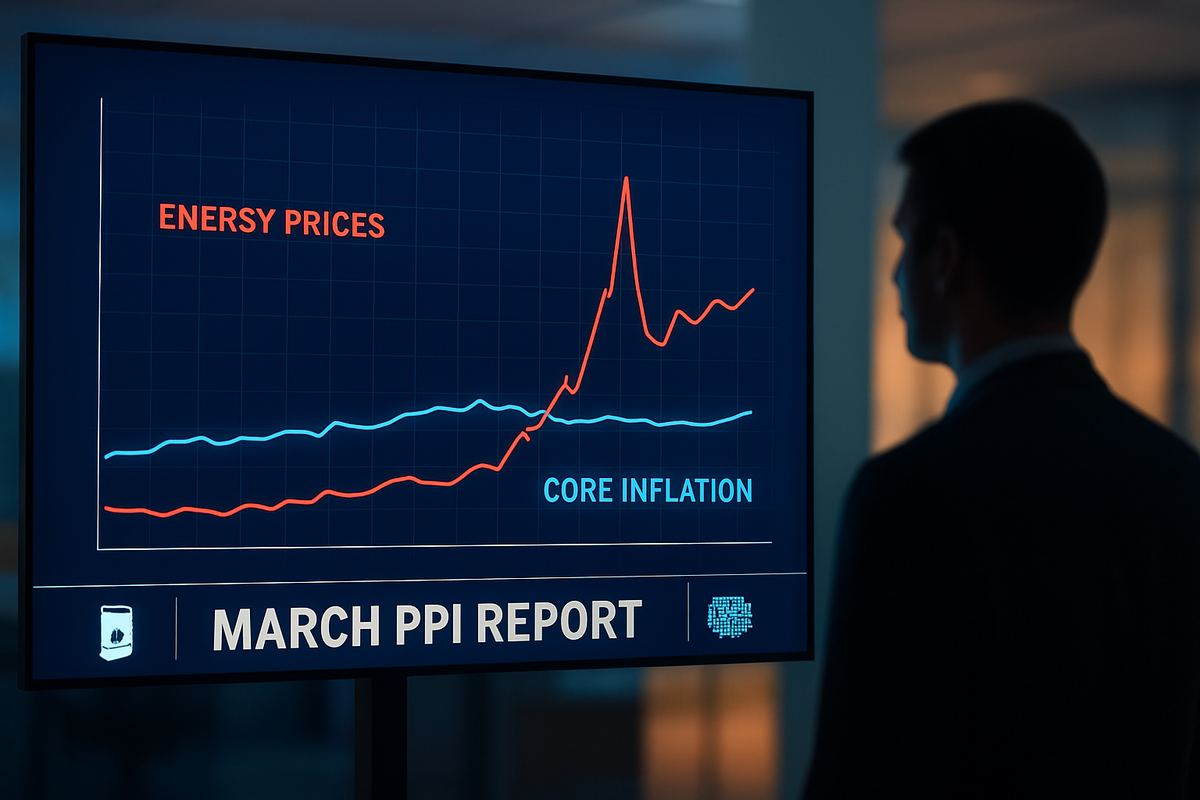

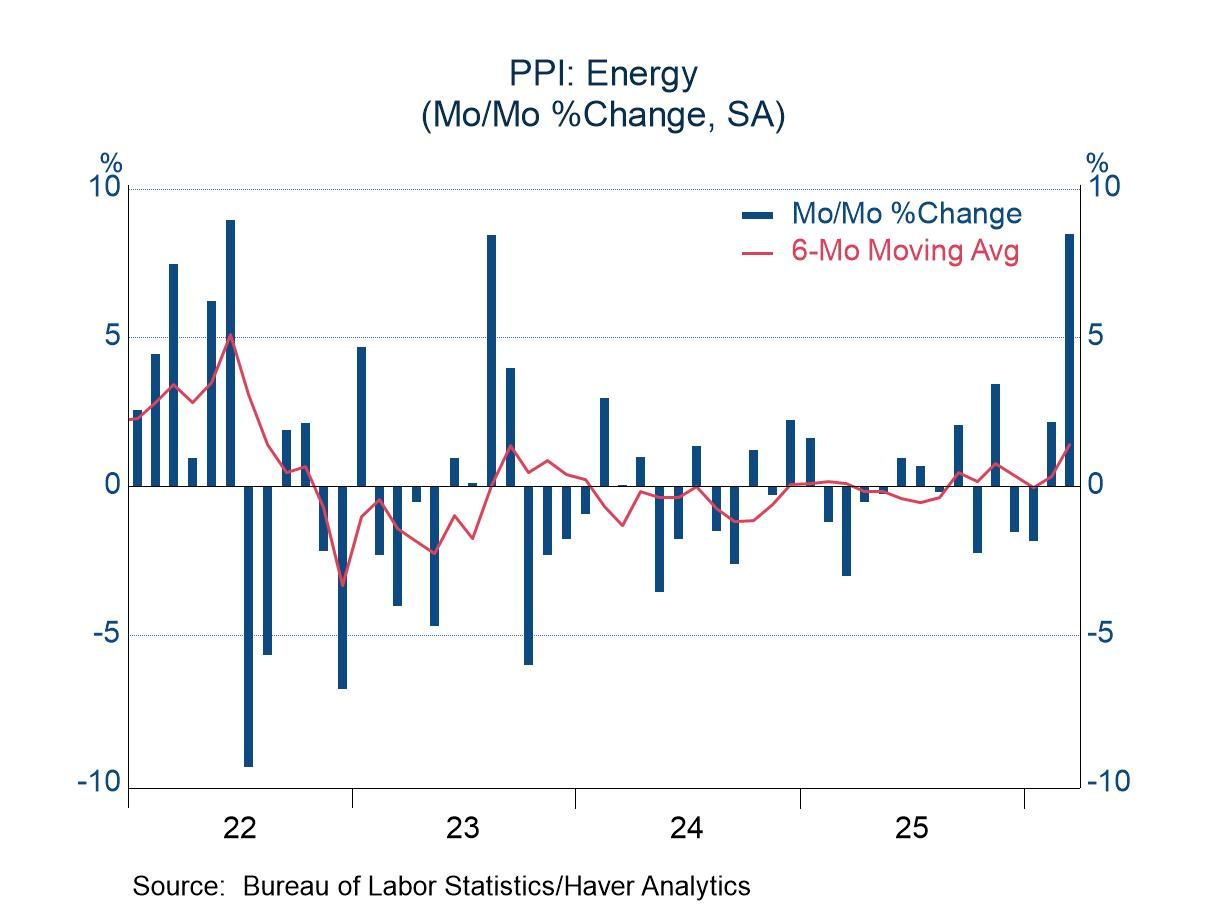

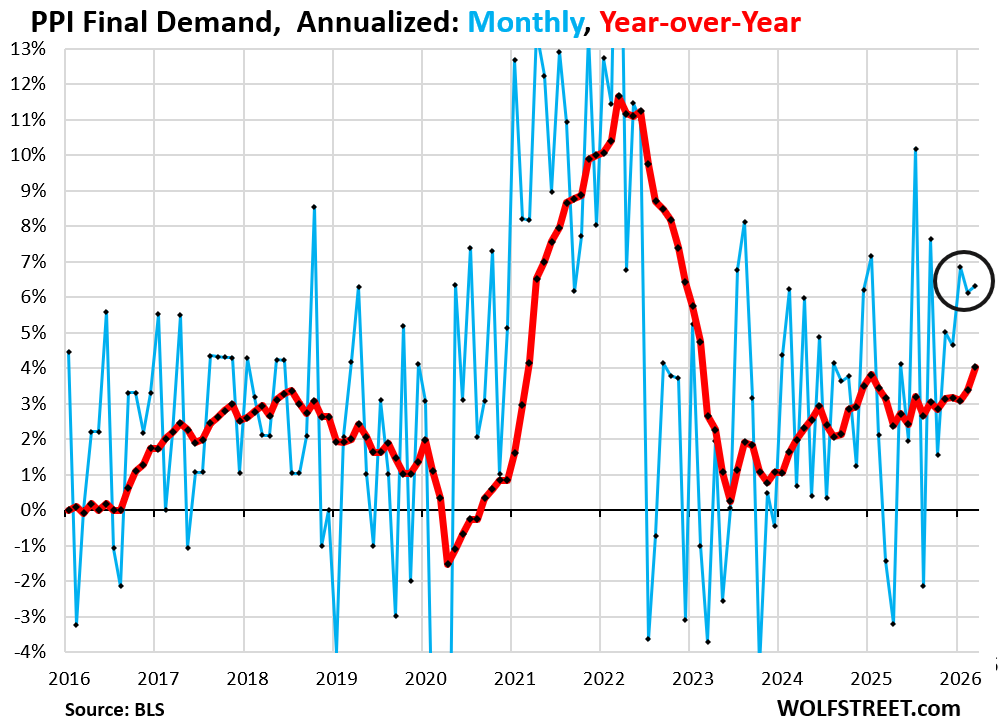

CRITICAL ALERT: US wholesale inflation reached a three-year high in March 2025, with the Producer Price Index (PPI) climbing to 4.0% annually—significantly outpacing the 3.8% core rate and signaling margin compression across cross-border e-commerce supply chains. The Bureau of Labor Statistics report (April 14, 2025) revealed a 0.5% monthly increase driven almost entirely by energy costs, with gasoline surging 15.7%, jet fuel soaring 30.7%, and diesel exploding 42%. While headline numbers beat economist forecasts (expected 1.1% monthly vs. actual 0.5%), the energy shock from the Iran-U.S. conflict has created a two-tier inflation environment: moderating tariff pressures offset by volatile logistics costs.

For cross-border sellers, this inflation trajectory creates immediate operational challenges and margin pressure. Air freight-dependent sellers face the steepest impact—jet fuel's 30.7% surge directly translates to 4.1% airfare increases, compressing margins on time-sensitive shipments by $150-400 per 1,000-unit shipment. Sellers sourcing petroleum-based products (plastics, chemicals, textiles) experience rising wholesale costs, while those relying on ocean freight benefit from moderating trade services (down 0.3% monthly), though elevated diesel costs offset gains. The Federal Reserve's likely decision to maintain interest rates through 2025 (25% probability of cuts) stabilizes financing costs but signals persistent inflation expectations, pressuring consumer discretionary spending.

The dual inflation signal creates strategic divergence by seller segment. Large sellers (10K+ monthly units) with diversified logistics networks can absorb energy volatility through 3PL optimization and mode-shifting to ocean freight. Mid-market sellers (1K-10K units) face critical decisions: accept 3-5% margin compression, raise prices 2-4% risking conversion loss, or shift inventory to lower-cost regions. Small sellers (<1K units) relying on air freight or express shipping face existential margin pressure—a $10 product with 40% COGS now faces $1.50-2.00 additional logistics costs, reducing net margin from $4 to $2.50-3.50. Food/beverage sellers benefit from falling food prices (moderating input costs), while electronics and apparel sellers absorb petroleum-based material inflation. The timing matters critically: March 10 data collection captured early-stage Iran conflict impacts; subsequent ceasefire announcements have eased energy prices ~15% from peaks, but crude remains up 70% year-to-date, suggesting volatility will persist through Q2-Q3 2025.

Consumer purchasing power erosion compounds seller challenges. RSM US economist projections show PCE inflation accelerating to 3.5% annually (0.7% monthly), up from February's 2.8%, directly reducing discretionary e-commerce demand. Sellers in non-essential categories (home décor, fashion, electronics) should expect 5-12% demand softening as consumers redirect spending to necessities. This creates a margin-demand squeeze: rising input costs force price increases precisely when consumer elasticity tightens, reducing conversion rates 2-8% depending on category and price point.

Questions 7

How much will my shipping costs increase from the 30.7% jet fuel surge?

Jet fuel's 30.7% spike translates to approximately 4.1% airfare increases for express/air freight shipments. For sellers shipping 1,000 units monthly via air freight at $2.50/unit baseline cost, expect an additional $100-150 monthly expense ($1.50-2.00 per unit increase). Ocean freight sellers benefit from moderating trade services (down 0.3%), though diesel costs (up 42%) offset gains by approximately 1-2%. The impact varies by origin region: Asia-to-US air freight sees steeper increases than intra-North America routes. Monitor freight indices weekly through your 3PL provider's dashboard to lock in rates before further escalation.

Will the Federal Reserve cut interest rates to help with financing inventory?

Current market expectations show only 25% probability of Fed rate cuts through December 2025, with the central bank likely maintaining current rates amid persistent inflation. The PPI report's 4.0% annual headline rate and 3.5% PCE inflation projections signal the Fed views inflation as sticky, not transitory. This means inventory financing costs will remain elevated—expect 7-9% APR on business lines of credit and 8-11% on inventory loans through 2025. Sellers should prioritize cash flow optimization and just-in-time inventory strategies rather than betting on rate relief. Consider locking in fixed-rate financing now before potential mid-year rate hikes if inflation accelerates further.