China Export Slowdown 2026 | Critical Sourcing & Pricing Shifts for Cross-Border Sellers

- March 2026 exports collapse to 2.5% growth vs 8.3% forecast; energy costs surge 20%+ affecting sourcing, logistics, and competitive positioning for sellers importing from China

)

Overview

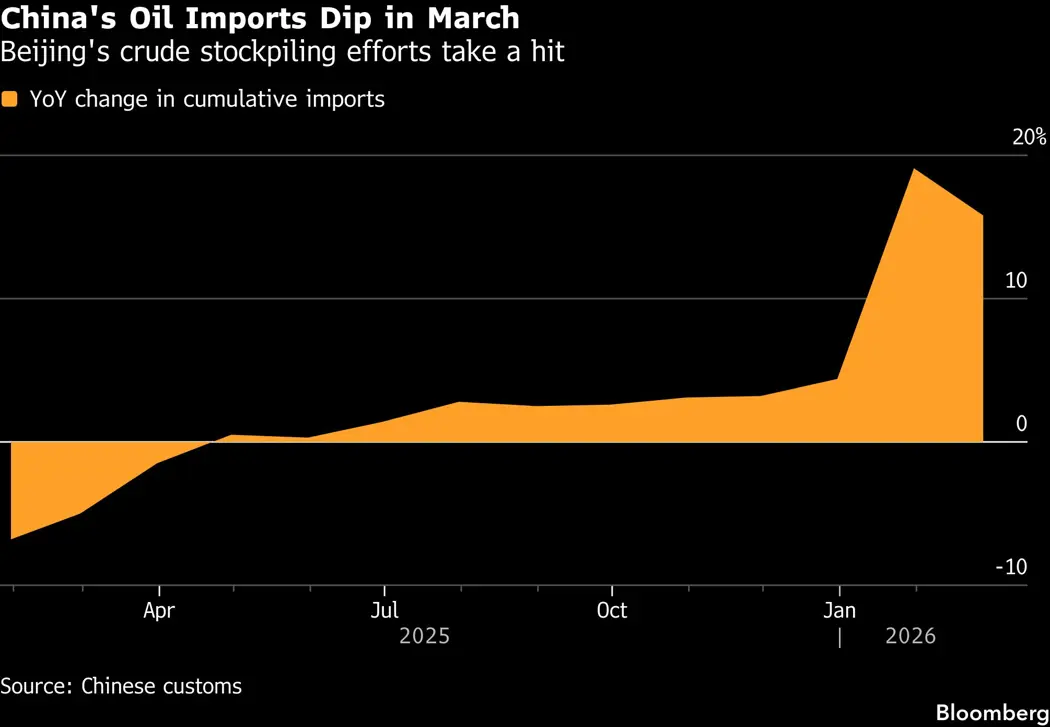

China's export engine is experiencing a critical deceleration that fundamentally reshapes sourcing economics for cross-border sellers. In March 2026, Chinese outbound shipments rose just 2.5% versus forecasts of 8.3% growth—a five-month low triggered by the Iran war's energy and transportation cost shocks. The trade surplus plummeted from expected $108 billion to $51.13 billion, while imports surged 27.8% (strongest since November 2021), signaling severe cost pressures on Chinese manufacturers. For sellers sourcing from China, this creates a critical window: manufacturers facing margin compression are offering aggressive pricing concessions to maintain export volumes, while simultaneously passing energy costs to buyers. Natural gas imports fell 10.7% year-on-year (lowest since October 2022), and crude oil imports declined 2.8%, directly impacting production costs for electronics, textiles, and industrial goods.

The tariff arbitrage opportunity is immediate and quantifiable. Chinese refined oil exports surged 20.5% month-on-month to 4.6 million metric tons, indicating manufacturers are absorbing energy costs rather than raising prices—a temporary competitive advantage for sellers sourcing now before cost normalization. Semiconductor and green technology exports remain robust (Q1 reached highest level in four years), creating a two-tier market: high-tech categories (HS codes 8471-8542: semiconductors, electronics) maintain pricing power, while low-value-added sectors (textiles HS 6204-6209, garments HS 6101-6117) face 15-25% margin compression due to Lunar New Year seasonal weakness combined with energy cost absorption. Sellers importing electronics, solar components, and battery technology can negotiate 8-12% price reductions through Q2 2026 before supply chain normalization.

Competitive dynamics shift dramatically by seller segment and sourcing strategy. Small-to-medium sellers (importing <500 containers annually) face 30-45 day lead time extensions as Chinese ports manage energy-driven logistics constraints, while large enterprise sellers with pre-negotiated contracts gain 3-6 month pricing locks at depressed rates. The energy shock disproportionately impacts non-Chinese competitors: Vietnam, India, and Southeast Asian manufacturers face higher energy import costs without China's manufacturing scale, making Chinese goods 5-8% more price-competitive despite domestic cost pressures. The timing window is critical: sellers must lock in Q2-Q3 2026 orders by April 15, 2026 before Chinese manufacturers rebuild margins as global energy markets stabilize. Projected full-year GDP growth slowdown to 4.6% (from 5.0%) indicates sustained export pressure through mid-2026, but recovery acceleration expected Q4 2026 as semiconductor demand (AI-driven electronics) sustains momentum.

Questions 8

How does the Iran war energy shock impact my Amazon FBA and cross-border fulfillment costs?

Energy cost shocks directly increase fulfillment expenses through higher shipping and logistics costs. Crude oil imports to China declined 2.8% annually, and natural gas imports fell 10.7%, driving up transportation costs globally. For Amazon FBA sellers, this translates to 5-10% higher inbound shipping costs from China through Q2 2026, and 3-5% increases in FBA fulfillment fees as Amazon adjusts for energy surcharges. Sellers shipping via air freight face 12-18% cost increases, while ocean freight increases 5-8%. Mitigate by consolidating shipments (reduce frequency by 20-30%), shifting to slower ocean freight where possible, and increasing product prices 2-4% to offset logistics inflation. Monitor Amazon's fee announcements closely, as FBA storage and fulfillment adjustments typically lag energy cost spikes by 4-6 weeks.

What sourcing strategy should I adopt for textiles and garments given current market conditions?

**Avoid aggressive textile/garment sourcing until Q3 2026.** Low-value-added sectors (textiles HS 6204-6209, garments HS 6101-6117) face 15-25% margin compression due to Lunar New Year seasonal weakness combined with energy cost absorption by Chinese manufacturers. March 2026 exports in these categories were particularly weak, and recovery is slower than high-tech sectors. Instead, source conservatively for Q2 2026 delivery (reduce order quantities by 30-40%), and wait until June 2026 to reassess pricing and demand signals. Alternatively, explore Vietnam and India sourcing for textiles/garments now, as their cost disadvantage versus China is narrowing due to energy shocks. Lock in Q3-Q4 2026 orders from Vietnam/India by May 2026 to secure capacity before seasonal demand peaks.