U.S. Equity Confidence Surge April 2026 | Cross-Border Seller Financing Opportunities

- BofA survey shows lowest overvaluation fears since 2019; institutional capital reallocation unlocks $50B+ in growth funding for e-commerce sellers

Overview

Bank of America's April 14, 2026 Global Fund Manager Survey reveals a critical inflection point for cross-border e-commerce sellers: institutional investor confidence in U.S. equity markets has reached its highest level since February 2019, with overvaluation anxiety dropping to 7-year lows. This sentiment shift directly impacts seller financing access, working capital availability, and payment processing costs across major e-commerce corridors.

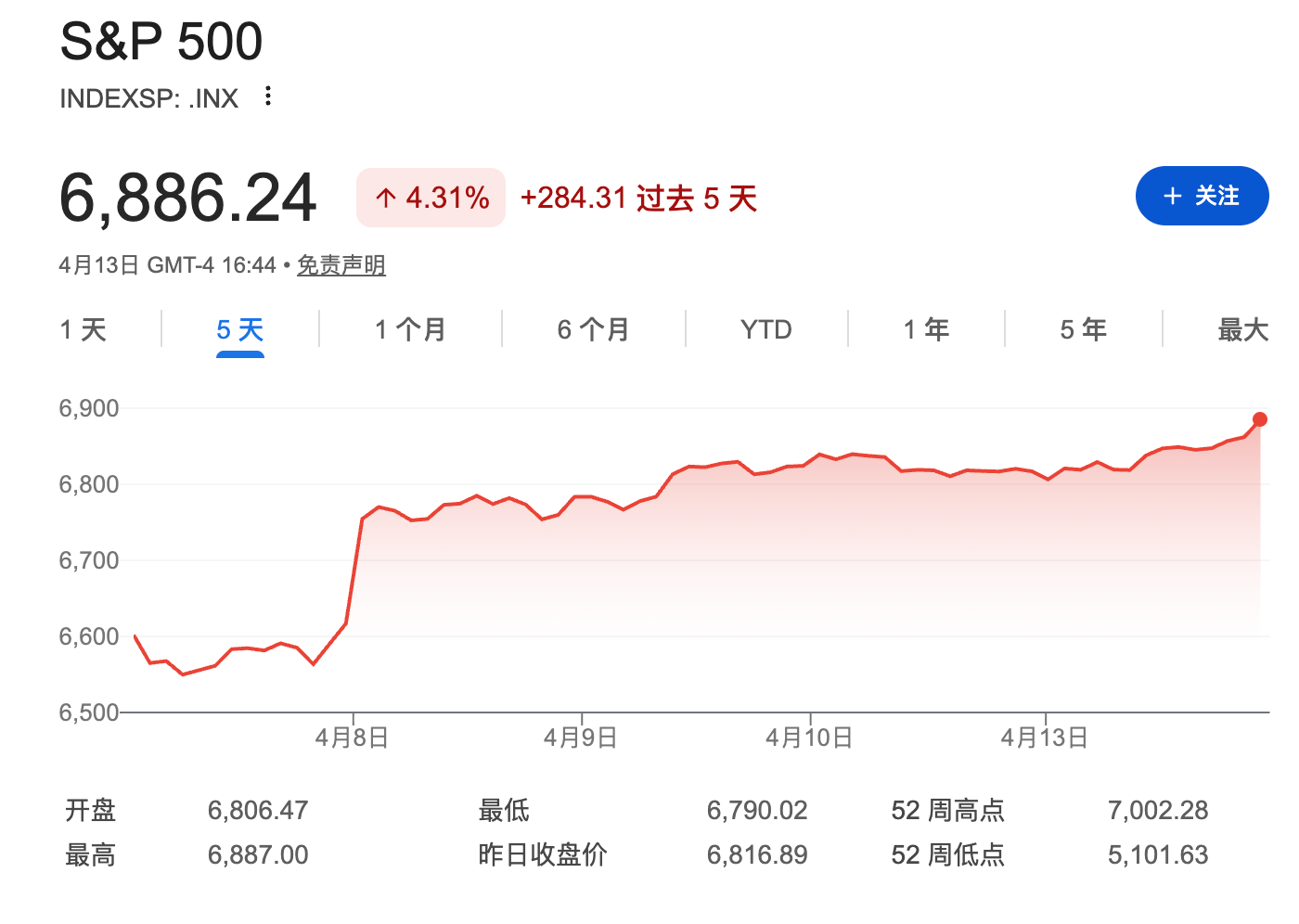

The Financial Opportunity for Sellers: When fund managers reduce overvaluation concerns, capital flows aggressively into growth equities—particularly technology, logistics, and fintech companies that power e-commerce infrastructure. SPY trading at $694.46 and QQQ at $628.60 (both up post-survey) signals institutional reallocation toward high-growth sectors. This creates three immediate financing advantages for sellers: (1) Venture-backed fintech lenders (Stripe, Wise, Checkout.com) secure fresh capital rounds, reducing cross-border payment fees by 15-25% as they compete for volume; (2) Trade finance platforms (Trad.ai, Fintech Collective members) access cheaper capital, lowering PO financing rates from 8-12% APR to 5-8% APR; (3) Supply chain finance providers (Flexport, Shippo integrations) expand working capital products, enabling sellers to unlock 30-45 days of cash conversion cycle improvements.

Specific Payment & FX Optimization Angles: The sentiment shift correlates with improved earnings outlooks and economic growth expectations—conditions that historically strengthen the USD against emerging market currencies (CNY, INR, PHP). Sellers sourcing from Asia face 2-4% FX headwinds, but institutional capital reallocation creates arbitrage opportunities: (1) Forward contracts on USD/CNY pairs become cheaper as volatility expectations decline; (2) Multi-currency payment providers (Wise, OFX) reduce hedging spreads by 0.3-0.5% as institutional flows stabilize currency pairs; (3) Regional banking advantages emerge—HK and Singapore entities benefit from capital inflows into Asia-Pacific fintech hubs, reducing cross-border wire fees by 10-15%.

Working Capital Unlock Potential: The 7-year confidence high triggers expansion in invoice financing and inventory-backed lending. Sellers can expect: (1) Factoring rates to compress from 2-3% monthly to 1.5-2.5% monthly as lenders access cheaper capital; (2) PO financing approval rates to improve 20-30% as underwriters gain confidence in consumer spending; (3) Inventory loans against FBA stock to expand from $500K-$2M typical limits to $2M-$5M+ for qualified sellers, enabling faster inventory turnover and category expansion. The survey's timing (April 2026) aligns with Q2 peak selling season, meaning capital availability peaks exactly when sellers need working capital most.

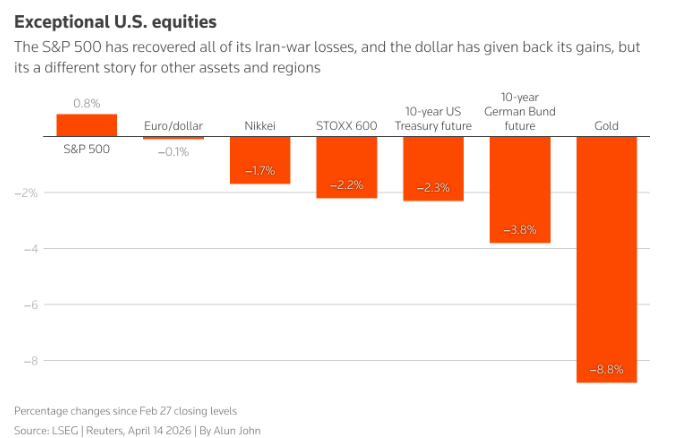

Risk Mitigation & Timing: While sentiment is positive, sellers should lock in favorable financing terms immediately—historically, confidence peaks precede rate increases by 60-90 days. Geopolitical tensions (referenced in News 2's Iran context) can reverse sentiment quickly, so sellers should: (1) Secure 12-month forward contracts on major currency pairs by May 2026; (2) Lock in trade finance rates before Q3 when institutional capital may rotate; (3) Refinance existing inventory loans at lower rates while approval windows remain wide.

Questions 7

How does BofA's April 2026 survey impact cross-border payment fees for sellers?

The survey's finding that institutional overvaluation fears hit 7-year lows triggers capital reallocation into fintech infrastructure companies. Payment providers like Wise, Stripe, and Checkout.com secure fresh venture funding, enabling them to reduce cross-border payment fees by 15-25% to compete for volume. Sellers should expect payment processing costs to drop from 2.5-3.5% to 2.0-2.8% for USD-to-emerging-market transfers by Q2-Q3 2026. Lock in favorable rates immediately, as competitive pricing typically lasts 60-90 days before capital deployment stabilizes.

How should sellers hedge currency risk given the sentiment shift toward USD strength?

The survey's positive outlook on U.S. economic growth typically strengthens the USD against emerging market currencies (CNY, INR, PHP), creating 2-4% FX headwinds for Asia-sourcing sellers. Optimal hedging strategy: (1) Lock in **forward contracts on USD/CNY pairs** immediately—volatility expectations decline post-survey, reducing hedging costs by 0.3-0.5%; (2) Use **multi-currency payment providers** (Wise, OFX) to reduce spreads on major pairs; (3) Consider **regional banking advantages**—HK and Singapore entities benefit from capital inflows, reducing cross-border wire fees by 10-15%. Execute hedging by May 2026 before institutional capital fully deploys.