Hormuz Blockade Triggers 2-3 Month Supply Delays | Cross-Border Sellers Face 15-25% Shipping Cost Surge

- Iran's $2M per-vessel toll and geopolitical tensions create immediate logistics crisis for Asian-sourced inventory; electronics, fertilizer, and semiconductor sellers most vulnerable through 2025

Overview

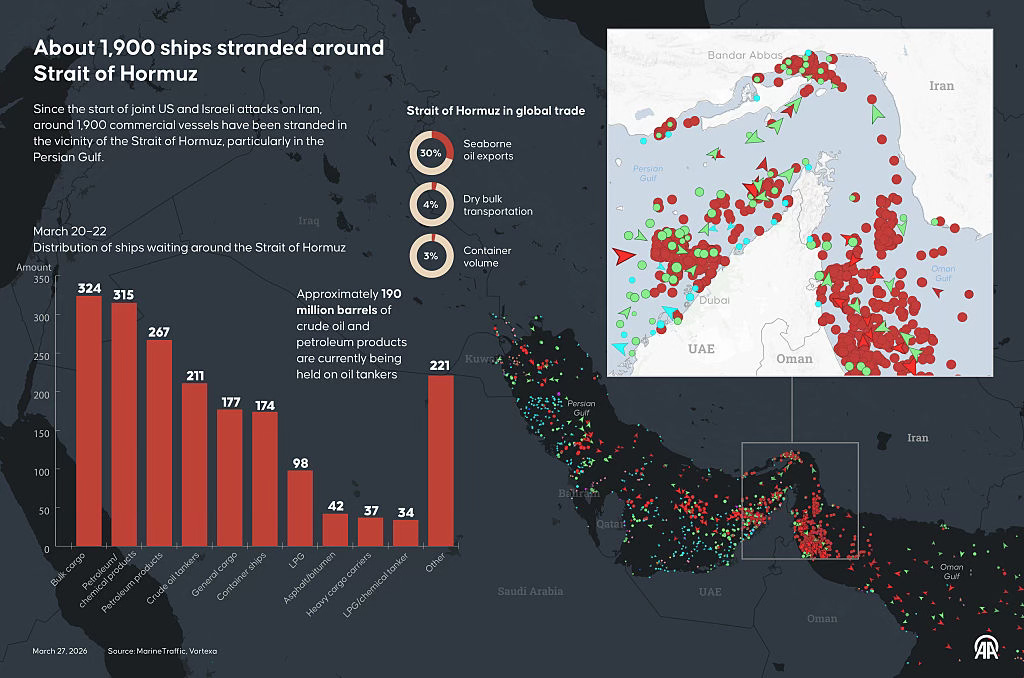

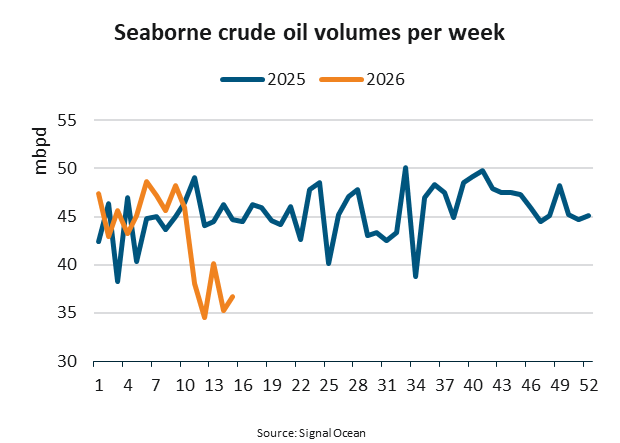

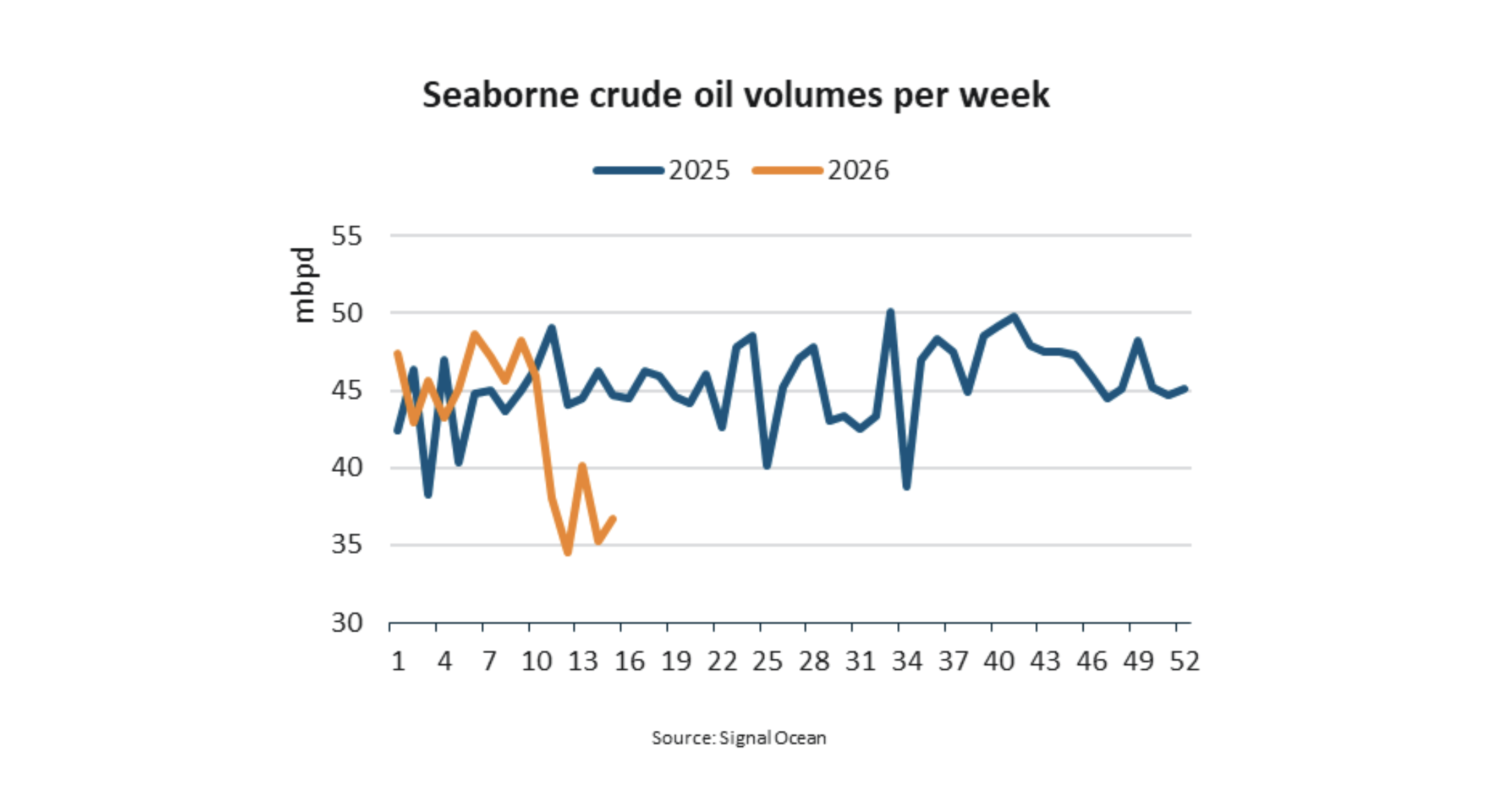

The Strait of Hormuz blockade represents the most significant supply chain disruption for cross-border e-commerce sellers since 2022, with immediate operational and financial consequences. According to CNBC's Power Insider analysis, the U.S. naval blockade of Iranian ports combined with Iran's emerging $2 million per-vessel toll system threatens 21% of global petroleum trade flowing through this critical chokepoint. For e-commerce sellers, this translates to 2-3 month inventory replenishment delays even if military hostilities cease immediately, plus 15-25% increases in fuel surcharges on ocean freight and 30-40% increases on air freight routes.

The financial impact cascades across multiple seller segments. Electronics sellers face semiconductor supply constraints due to helium shortages (critical for chip manufacturing), while agricultural product sellers confront fertilizer scarcity as Saudi Arabia and UAE redirect their 8.5 million barrels-per-day pipeline capacity away from traditional Hormuz routes. Heavy goods and perishable sellers using refrigerated transport experience disproportionate cost exposure, with fuel surcharges potentially adding $200-400 monthly per shipment. The Reuters Breakingviews analysis (April 15, 2025) reveals Iran's rational toll ceiling sits at approximately $55 billion over 25 years—the cost threshold at which Gulf states would justify alternative pipeline infrastructure. This suggests sustained toll pressure for 7+ years during pipeline construction, creating a structural cost floor for all Hormuz-dependent shipping.

Immediate market opportunities emerge for sellers willing to shift sourcing geography. Vietnam, India, and Indonesia—countries with lower energy-dependent manufacturing costs and alternative shipping routes avoiding Hormuz—become strategically attractive for categories like electronics, textiles, and consumer goods. Sellers currently sourcing 60-80% from China face margin compression unless they diversify sourcing by Q2 2025. The 50% reduction in Hormuz-dependent oil (via Saudi/UAE pipeline alternatives) provides some stability, yet alternative routing adds 7-14 days to transit times and increases logistics complexity. Compliance opportunity: Sellers can legally leverage MarineTraffic.com's live ship mapping to monitor vessel routing and negotiate better rates with 3PL providers using non-Hormuz corridors, potentially recovering 5-8% of fuel surcharge increases through route optimization.

Questions 8

How much will Hormuz shipping disruptions increase my Amazon FBA costs in 2025?

Ocean freight surcharges will increase 15-25% due to fuel costs and alternative routing, while air freight faces 30-40% increases. For sellers shipping 1,000+ units monthly via FBA, expect $200-400 additional monthly costs per shipment. Amazon typically passes fuel surcharges to sellers within 30-45 days through adjusted shipping rates in Seller Central. Sellers relying on Asian manufacturing should immediately audit their 3PL contracts for fuel surcharge caps and negotiate fixed-rate agreements through Q4 2025 before rates stabilize.

Should I shift my sourcing from China to Vietnam or India due to Hormuz risks?

Yes, for 20-30% of your inventory, particularly electronics and consumer goods. Vietnam and India offer 5-8% lower manufacturing costs due to reduced energy dependency and access to non-Hormuz shipping routes (via Singapore and Port Klang). However, transition costs include supplier qualification (4-8 weeks), MOQ adjustments, and quality audits. The ROI breakeven occurs at 6-9 months for sellers shipping 500+ units monthly. Start with non-critical SKUs and expand to core products by Q3 2025 before alternative pipeline construction begins (7-year timeline).