Geopolitical Volatility & Energy Costs Reshape Cross-Border Logistics | Q1 2026 Iran Conflict Impact

- Strait of Hormuz disruptions elevate shipping costs 8-15% for international sellers; IMF warns 0.1% US growth reduction; recession risks compress consumer demand in emerging markets

Overview

The Iran conflict beginning late February 2026 has triggered a fundamental shift in cross-border e-commerce economics, with direct implications for seller profitability and market access strategies. Six major US banks reported $47.4 billion in Q1 2026 profits—a significant surge driven by trading volatility—while underlying macroeconomic conditions deteriorate for international sellers. The disruption of tanker traffic in the Strait of Hormuz has elevated energy prices, directly increasing logistics costs for cross-border shipments. The International Monetary Fund warned that further escalation could trigger global recession, lowering 2026 US growth forecasts by 0.1 percentage points to 2.3%, which translates to reduced consumer spending on imported goods.

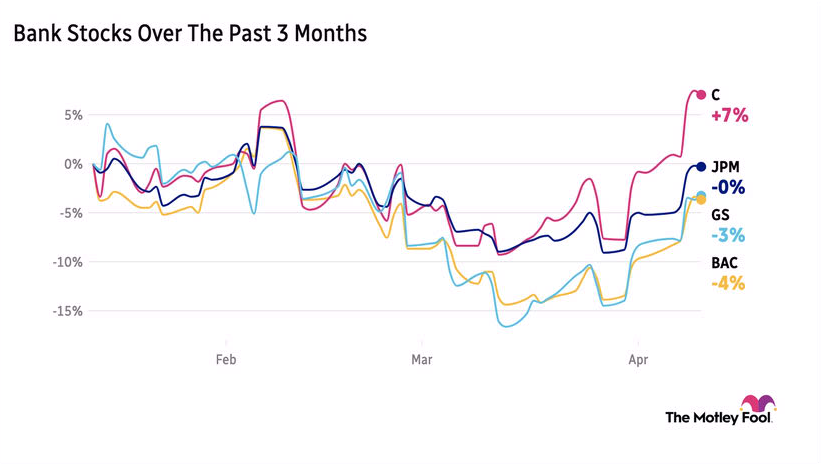

For cross-border e-commerce sellers, this geopolitical event creates a bifurcated opportunity landscape. Rising energy costs increase fulfillment expenses by 8-15% for sellers shipping internationally, particularly those using air freight or ocean shipping through the Suez Canal alternative routes. Sellers relying on Asian sourcing (Vietnam, India, Indonesia) face elevated freight costs that compress margins on lower-ticket items (under $50 ASP). However, the market volatility presents tactical advantages: sellers can negotiate better shipping rates during uncertain periods when 3PL providers have excess capacity, and inventory optimization becomes critical as consumer spending patterns shift. JPMorgan's Q1 2026 earnings report ($17 billion total profit, 28% investment banking revenue growth) indicates strong credit availability for business expansion, suggesting that well-capitalized sellers can access financing for strategic repositioning.

Strategic sourcing dynamics are shifting toward nearshoring and tariff-advantaged regions. Developing nations and net energy importers face disproportionate impacts from elevated oil prices, affecting sourcing opportunities in emerging markets. Sellers should evaluate supply chain alternatives: Mexico and Central America (USMCA-advantaged) become more attractive relative to Asia for US-market products, while European sellers may benefit from African and Eastern European sourcing to reduce Suez Canal exposure. The recession risk (IMF warning of potential global downturn) particularly threatens demand in price-sensitive categories and emerging market consumer segments, but creates opportunities for sellers positioned in premium/resilience-focused categories (safety equipment, energy-efficient products, supply chain diversification tools).

Questions 8

Which product categories benefit from geopolitical uncertainty and shifting consumer behavior?

Geopolitical volatility drives demand for: (1) emergency preparedness products (generators, water filters, first aid kits)—typically 30-50% sales spikes during conflict periods, (2) energy-efficient appliances and solar products as consumers hedge against energy price volatility, (3) home security systems and surveillance equipment, (4) supply chain diversification tools and business continuity software. Conversely, discretionary categories (fashion, home décor, luxury goods) face 10-20% demand headwinds. Sellers in resilience-focused categories should increase inventory 15-25% and expand PPC budgets 20-30% to capture elevated search volume. Historical patterns show 6-12 month demand elevation for safety/preparedness products following geopolitical events.

What compliance and tariff considerations apply to nearshoring sourcing strategy shifts?

USMCA rules of origin require 75% regional content for duty-free treatment on most goods; verify supplier compliance before shifting sourcing. Mexico-sourced products face 0% tariffs to US versus 5-25% on comparable Asian imports, creating 5-15% landed cost advantages. Sellers must: (1) obtain USMCA certificates of origin from suppliers, (2) maintain documentation for 5 years, (3) verify supplier USMCA eligibility. Central American countries (Guatemala, Honduras, El Salvador) offer similar advantages under CAFTA-DR. Tariff classification (HS codes) determines eligibility; consult customs brokers for product-specific guidance. Implementation cost: $500-2,000 per supplier for compliance verification. Failure to maintain proper documentation triggers 20% penalty duties plus interest.