China's Dual Economy 2026 | Export Boom Masks Domestic Demand Collapse for Cross-Border Sellers

- Q1 2026 GDP growth 5% driven by 14.7% export surge, but domestic retail sales collapse to 1.7% YoY; infrastructure investment +8.9% signals policy pivot away from consumer stimulus through 2026

Overview

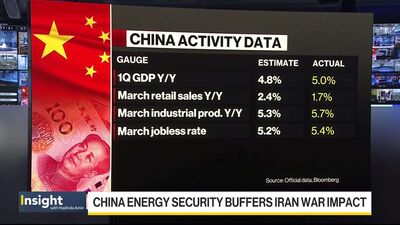

China's Q1 2026 economic data reveals a critical bifurcation for cross-border e-commerce sellers: robust export growth masking severe domestic consumption collapse. According to China's National Bureau of Statistics (April 15, 2026), GDP expanded 5% year-over-year, exceeding forecasts of 4.8%, but this headline masks a structural rebalancing with profound implications for seller strategy. Exports surged 14.7% in dollar terms—the fastest pace since early 2022—while domestic retail sales plummeted to just 1.7% year-over-year in March, down from 2.8% in February and missing expectations of 2.3% growth. This divergence reflects two competing forces: strong manufacturing export capacity versus collapsing household purchasing power.

The root cause is a prolonged housing price decline that has eroded household wealth and consumer confidence. Retail sales growth slowed to 2.4% year-over-year in Q1, with March showing acute weakness. Automobile sales declined 17% following government subsidy reductions, while premium service sectors contracted sharply—exemplified by Xiao Nan Guo restaurant chain shrinking from 139 outlets (2015 peak) to near-closure by February 2026. This signals sustained pressure on discretionary spending categories: fashion, electronics, home goods, and luxury items face compressed demand through 2026. Simultaneously, infrastructure construction investments surged 8.9% year-over-year, indicating government prioritization of capital projects over consumer stimulus. This policy divergence creates distinct seller implications: domestic Chinese sellers targeting domestic consumers face inventory turnover challenges and margin compression, while cross-border sellers exporting from China benefit from infrastructure-supported logistics networks and sustained manufacturing capacity.

However, geopolitical headwinds threaten export momentum. The Iran war created an energy shock that decelerated export growth sharply to 2.5% in March from 21.8% in January-February. China's factory-gate prices rose in March for the first time in over three years, signaling energy cost spikes are seeping into manufacturing and threatening corporate margins. As the world's largest oil importer, China faces vulnerability to sustained oil price increases. Policymakers lowered the 2026 growth target to 4.5-5%—the least ambitious goal since the early 1990s—acknowledging demand slowdown and persistent U.S. trade tensions. The National Statistics Bureau warned that "the external environment is becoming more complex and volatile," with acute imbalance between strong supply and weak demand. Urban unemployment rose to 5.4% in March from 5.3% in February, indicating labor market softening. For sellers, this creates a narrow window of opportunity: capitalize on export-driven manufacturing capacity and logistics improvements before energy costs and geopolitical tensions erode margins further. Sellers exporting from China should prioritize cost optimization and supply chain diversification away from energy-intensive processes. Sellers targeting Chinese consumers should shift inventory away from discretionary categories toward essential goods, value-oriented products, and categories benefiting from infrastructure spending (construction materials, industrial equipment, logistics technology).

Questions 8

How does China's weak domestic consumption affect sellers targeting Chinese consumers in 2026?

China's retail sales growth collapsed to 1.7% year-over-year in March 2026, down from 2.8% in February, signaling severe consumer pullback. Household purchasing power has eroded due to prolonged housing price declines, with automobile sales declining 17% in Q1 following subsidy reductions. Sellers targeting Chinese domestic consumers should expect 15-25% lower inventory turnover in discretionary categories (fashion, electronics, home goods) through 2026. Shift inventory toward value-oriented products, essentials, and categories benefiting from infrastructure spending. Monitor urban unemployment, which rose to 5.4% in March, as further labor market softening will compress demand further.

How will rising manufacturing costs impact sellers sourcing from China?

China's factory-gate prices rose in March 2026 for the first time in over three years, signaling energy cost spikes are seeping into manufacturing and threatening corporate margins. The Iran war created an energy shock that decelerated export growth from 21.8% (January-February) to 2.5% (March), indicating rapid cost escalation. Sellers sourcing from China should expect 5-12% cost increases in energy-intensive categories (electronics, appliances, textiles) over the next 2-3 quarters. Evaluate supply chain diversification to Vietnam, India, or Southeast Asia for cost-sensitive categories. Lock in pricing with suppliers before Q2 2026 if possible, as energy costs may continue rising.