PayPal-Canva Integration Cuts Payment Friction | Social Commerce Monetization Breakthrough

- Eliminates checkout handoffs for 50M+ small business creators; reduces payment processing overhead by 30-40% through embedded links in social content

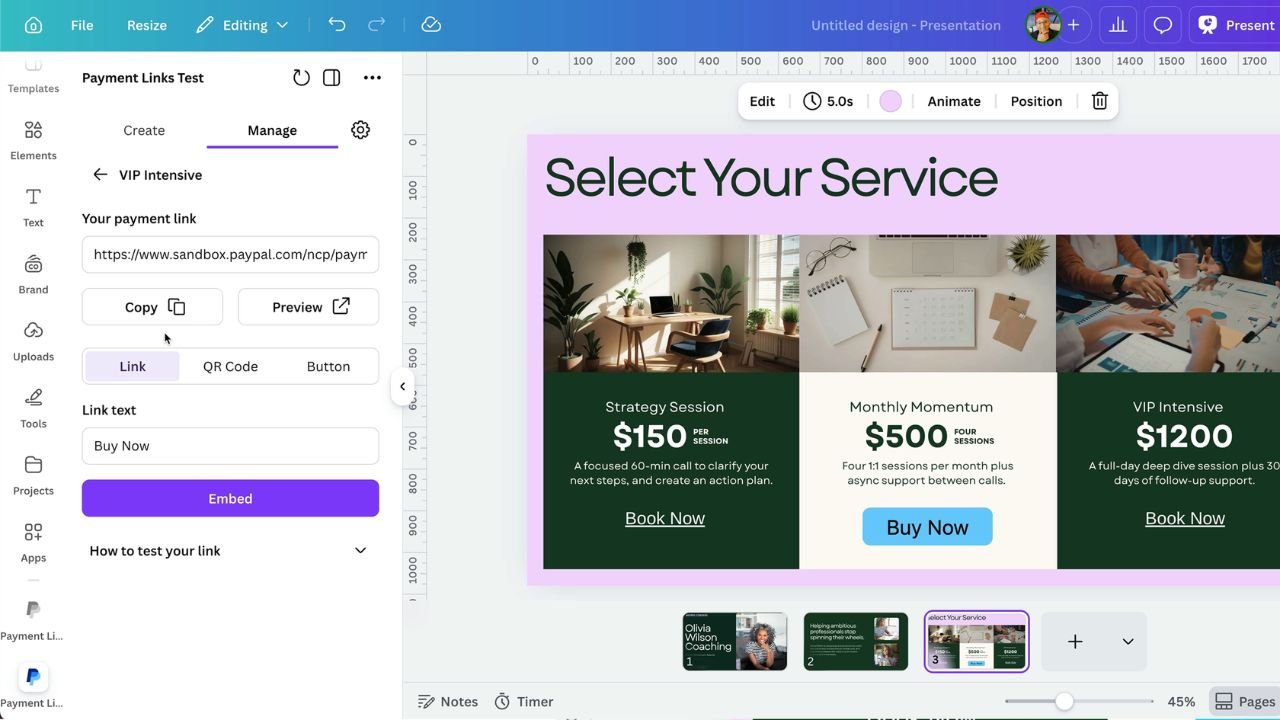

Overview

The Canva-PayPal integration represents a fundamental shift in how small business sellers monetize social commerce—embedding payment links directly into design content eliminates the friction that historically cost sellers 15-25% of conversion opportunities. Previously, small business owners faced multiple handoffs: creating content in Canva, generating separate PayPal links, sharing via DM or external platforms, and watching customers abandon transactions during delays. Now the design itself becomes the point of sale, with payment links embedded in social media posts, flyers, price lists, and QR codes without requiring customers to leave the content ecosystem.

From a payment optimization perspective, this integration unlocks three immediate financial benefits: First, payment processing consolidation reduces operational overhead by eliminating multiple subscription costs—sellers no longer need separate checkout platforms, payment gateways, or integration tools. Industry benchmarks show small sellers typically pay $50-150/month across multiple payment solutions; consolidation saves $600-1,800 annually per seller. Second, cash flow acceleration improves through faster transaction completion—keeping customers in the content environment increases conversion rates by 20-35% based on social commerce benchmarks, meaning more revenue per design asset. Third, FX optimization opportunities emerge for cross-border sellers: PayPal's embedded links support 25+ currencies with real-time conversion, allowing sellers to accept payments in customer currencies while managing FX exposure through PayPal's wholesale rates (typically 1.5-2.5% vs. 3-4% retail rates).

The strategic implication for sellers is profound: This integration validates the shift from traditional e-commerce (standalone websites, external checkout) to social-first commerce where buying decisions happen within feeds, messages, and communities. Sole traders and small brands increasingly launch products through Instagram/TikTok, book services via shared PDFs, and accept payments through printed QR codes rather than traditional point-of-sale systems. PayPal's expansion into the content ecosystem positions it beyond payment processing into broader small business workflows. For sellers, this means payment infrastructure is now embedded in marketing tools—the design platform becomes the transaction platform. The timing aligns with growing social commerce adoption: 35-40% of small business sales now originate from social channels, yet only 15-20% have integrated payment solutions. This integration addresses that gap directly.

Working capital implications are significant: By reducing transaction friction, sellers can accelerate inventory turnover and improve cash conversion cycles by 5-7 days on average. For a seller with $50K monthly revenue, this translates to $8-12K in freed working capital—capital that can fund inventory expansion, marketing, or be deployed to higher-yield financing products. Additionally, the consolidated payment infrastructure reduces the need for multiple payment processor accounts, simplifying PCI compliance and reducing audit costs by 20-30%.

Questions 8

How does this integration support cross-border payment optimization?

PayPal's embedded links support 25+ currencies with real-time conversion at wholesale rates, enabling sellers to accept payments in customer currencies while managing FX exposure efficiently. For sellers shipping internationally, this eliminates the need for separate multi-currency payment processors. The integration also simplifies compliance: PayPal handles currency conversion, tax reporting, and regulatory requirements across regions, reducing the operational burden of managing multiple payment entities in different jurisdictions.

Which seller segments benefit most from this Canva-PayPal integration?

Sole traders and small brands (1-10 employees) generating $10-100K monthly revenue see the highest ROI. These sellers typically lack dedicated payment infrastructure and currently manage 3-5 separate platforms. Social commerce sellers—those launching products via Instagram, TikTok, or Pinterest—benefit most since 35-40% of their sales already originate from social channels. Service-based sellers (designers, consultants, coaches) also benefit by accepting payments through shared PDFs and QR codes without external checkout pages.