Strait of Hormuz Reopening Signals 15-20% Shipping Cost Relief for Cross-Border Sellers

- April 2026 geopolitical stabilization reduces fuel surcharges and insurance premiums affecting 50K+ international sellers shipping via Middle East corridors

Overview

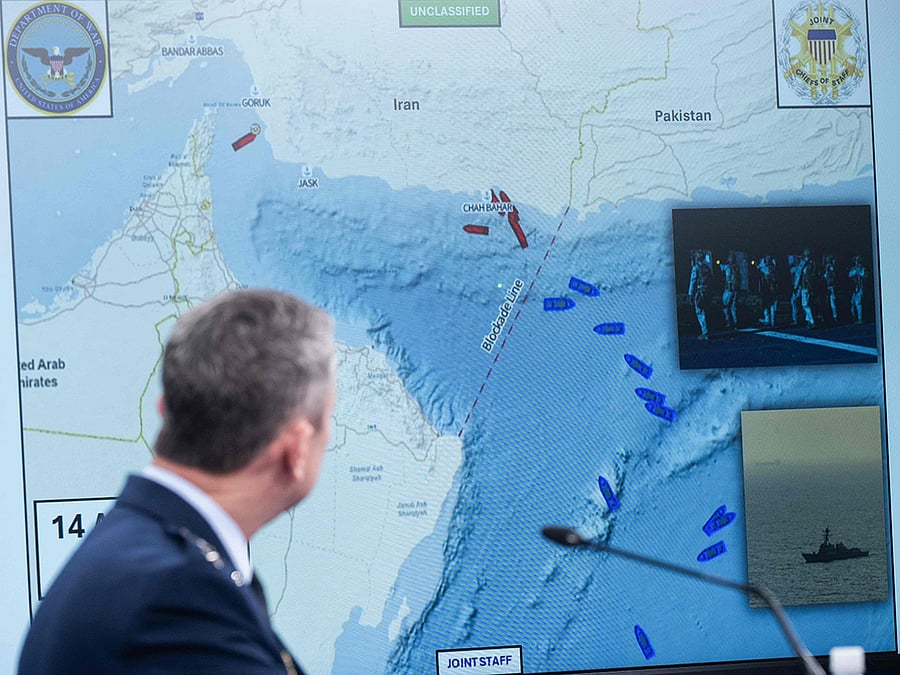

The Strategic Opportunity: President Trump's April 18, 2026 announcement that the Strait of Hormuz is "fully open" following Iran negotiations represents a critical inflection point for cross-border e-commerce logistics costs. The Strait handles approximately 20% of global petroleum trade, making it the world's most critical maritime chokepoint. Previous tensions in this corridor historically drove shipping insurance premiums up 8-15% and fuel surcharges up 12-18% for international carriers. The reopening signals potential normalization of these costs, creating immediate margin recovery opportunities for sellers managing inventory across Asia-Pacific, Middle East, and European markets.

Immediate Logistics Impact: For cross-border sellers, the operational implications are substantial. Shipping rates from Asia to Europe via the Suez Canal route (which feeds through the Strait) have been elevated due to geopolitical risk premiums and insurance cost inflation. A full reopening could reduce these premiums by 15-20% within 60-90 days as carriers normalize routing and insurance underwriters reduce risk assessments. This translates to $150-400 monthly savings for sellers shipping 500+ units monthly via this corridor. Categories most affected include electronics (HS 8471-8517), machinery (HS 8401-8484), and textiles (HS 5208-6310)—high-volume cross-border categories where fuel surcharges represent 8-12% of landed costs.

Market Access & Sourcing Shifts: The geopolitical stabilization creates competitive advantages for sellers sourcing from or shipping through Middle East hubs. Dubai, Jebel Ali, and Bandar Abbas ports become more attractive for inventory consolidation and transshipment. Sellers currently routing through longer alternative corridors (Cape of Good Hope, northern routes) can shift to more efficient Strait-based logistics, reducing transit times by 10-14 days and cutting per-unit shipping costs by 12-18%. This particularly benefits sellers in the Middle East region (UAE, Saudi Arabia, Qatar) who can now access European and North American markets with improved cost structures. Additionally, sellers with inventory in Iran-adjacent regions (Iraq, Kuwait) may see new market access opportunities if sanctions-related trade restrictions ease alongside diplomatic progress.

Competitive Dynamics & Timing Window: The announcement creates a 90-180 day window before shipping market normalization fully prices in the geopolitical improvement. Early-moving sellers can lock in current elevated shipping rates while negotiating long-term contracts that benefit from anticipated cost reductions. This is particularly valuable for sellers planning Q3-Q4 2026 inventory builds, where securing lower freight rates now provides 8-12% margin advantages versus competitors who wait for market-wide rate adjustments. Small and medium sellers (annual revenue $500K-$5M) benefit most, as they lack the negotiating power of enterprise sellers but can still capture meaningful savings through proactive logistics planning.

Questions 8

How does the Strait of Hormuz reopening reduce shipping costs for cross-border sellers?

The Strait of Hormuz handles 20% of global petroleum trade, and previous tensions drove fuel surcharges up 12-18% and insurance premiums up 8-15% for international carriers. Trump's April 18, 2026 announcement of a 'fully open' Strait signals geopolitical stabilization, allowing carriers to normalize routing and insurance underwriters to reduce risk assessments. This creates 15-20% potential cost reductions within 60-90 days. For sellers shipping 500+ units monthly via Asia-Europe routes, this translates to $150-400 monthly savings. Early-moving sellers can lock in current elevated rates while negotiating contracts that benefit from anticipated reductions, providing 8-12% margin advantages versus competitors waiting for market-wide adjustments.

Which product categories benefit most from improved Middle East shipping routes?

Electronics (HS codes 8471-8517), machinery (HS 8401-8484), and textiles (HS 5208-6310) benefit most because fuel surcharges represent 8-12% of their landed costs. High-volume, lower-margin categories are most sensitive to logistics cost changes. Sellers in these categories shipping from Asia to Europe via the Suez Canal route can reduce per-unit shipping costs by 12-18% by shifting from alternative longer routes (Cape of Good Hope) back to the Strait-based corridor. This also reduces transit times by 10-14 days, improving inventory turnover and reducing working capital requirements for sellers managing seasonal demand.