Strait of Hormuz Shipping Crisis | Freight Costs Surge 15-25% for Cross-Border Sellers

- 50-day blockade creates $2-4B supply chain disruption; sellers face elevated shipping costs, inventory delays, and route restructuring through Q2 2026

Overview

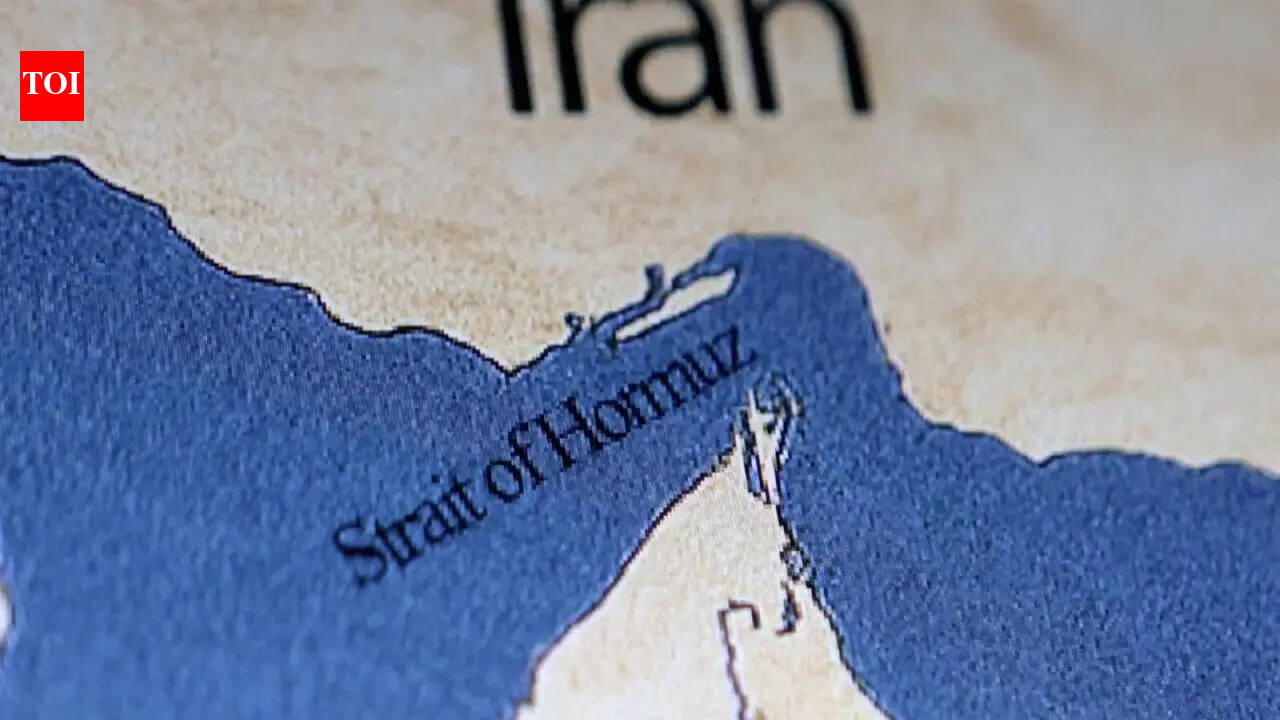

The April 2026 Strait of Hormuz blockade represents a critical supply chain inflection point for cross-border e-commerce sellers. On April 18, 2026, Reuters reported that after a 50-day closure, more than a dozen tankers briefly transited the waterway before Iran reimposed restrictions on Saturday and fired at vessels attempting passage. This chokepoint handles approximately 21% of global petroleum trade and critical LNG supplies—the first LNG cargoes from Qatar's Ras Laffan facility arrived only after February 28 conflict resolution. The International Energy Agency termed this "the worst-ever supply disruption," with hundreds of ships stranded in the Persian Gulf and major producers (Saudi Arabia, UAE, Iraq, Kuwait) sharply reducing output.

For e-commerce sellers, the immediate impact manifests across three critical dimensions: First, freight rate volatility is accelerating. Ocean freight from Asia to North America and Europe typically costs $1,200-1,800 per 20ft container; current disruption-driven rates are climbing 15-25% ($1,800-2,250 per container) as shipping lines reroute around Africa via the Cape of Good Hope—adding 10-14 days transit time and $400-600 per container. Sellers shipping electronics, apparel, and home goods from China, Vietnam, and India face immediate margin compression of 8-12% on products with <30% gross margins. Second, inventory management becomes critical. The 50-day blockade created a backlog of 300+ vessels; even with partial reopening, sellers should expect 3-4 week delays on Asia-to-Middle East shipments and 2-3 week delays on Asia-to-Europe routes through May 2026. Third, energy-dependent product categories face cost pressures: plastics (HS 3901-3916), chemicals (HS 2901-2942), and petroleum products (HS 2701-2715) will see 5-8% cost increases as crude oil prices remain elevated ($85-95/barrel vs. pre-crisis $70-75).

Strategic sourcing shifts are accelerating. Sellers currently sourcing from Middle East suppliers (petrochemicals, fertilizers, minerals) should evaluate Vietnam, India, and Indonesia alternatives to avoid Hormuz dependency. Companies with established 3PL networks in Southeast Asia or India can capture market share from competitors still dependent on Gulf-routed supply chains. The volatile geopolitical situation—with U.S., Iran, and Israel tensions unresolved—suggests this disruption may persist through Q2 2026, making alternative sourcing not a luxury but a competitive necessity for sellers with <$500K annual revenue who lack supply chain redundancy.

Questions 8

What geopolitical risks should I monitor for future Hormuz disruptions?

The April 2026 blockade reflects unresolved U.S.-Iran-Israel tensions. Key risk indicators: (1) escalation in U.S.-Iran sanctions, (2) Israeli military actions in the region, (3) Iranian Revolutionary Guard statements about strait closure, and (4) insurance premium spikes (currently 2-3% above baseline). Subscribe to geopolitical risk alerts from sources like Stratfor and Control Risks. Implement quarterly supply chain stress tests assuming 30-60 day Hormuz closures. Maintain 60-90 day safety stock for critical SKUs. Consider supply chain insurance products covering geopolitical disruptions (cost: 0.5-1.5% of shipment value). Diversify sourcing across at least 3 geographic regions to minimize single-point-of-failure risk.

How can I leverage 3PL networks to mitigate Hormuz disruption risks?

Sellers with established 3PL networks in Southeast Asia, India, or Europe can capture market share from competitors dependent on Gulf-routed supply chains. Evaluate 3PL providers in Vietnam, Thailand, and India who offer: (1) local sourcing capabilities, (2) direct Asia-to-Europe shipping routes avoiding Hormuz, and (3) inventory buffering services. Cost: typically 8-12% of product value for full 3PL services. Benefits: 2-3 week faster delivery, reduced freight volatility exposure, and competitive advantage during supply chain disruptions. Negotiate 6-month contracts with 2-3 providers to build redundancy; avoid single-provider dependency.