Strait of Hormuz Closure Drives Shipping Costs Up 15-25% | Cross-Border Sellers Face Critical Supply Chain Risk

- Prolonged energy disruption extends shipping timelines 8-12 weeks; fuel surcharges spike 15-25% for Asia-Pacific routes; sellers relying on just-in-time inventory face margin compression of 8-12%

Overview

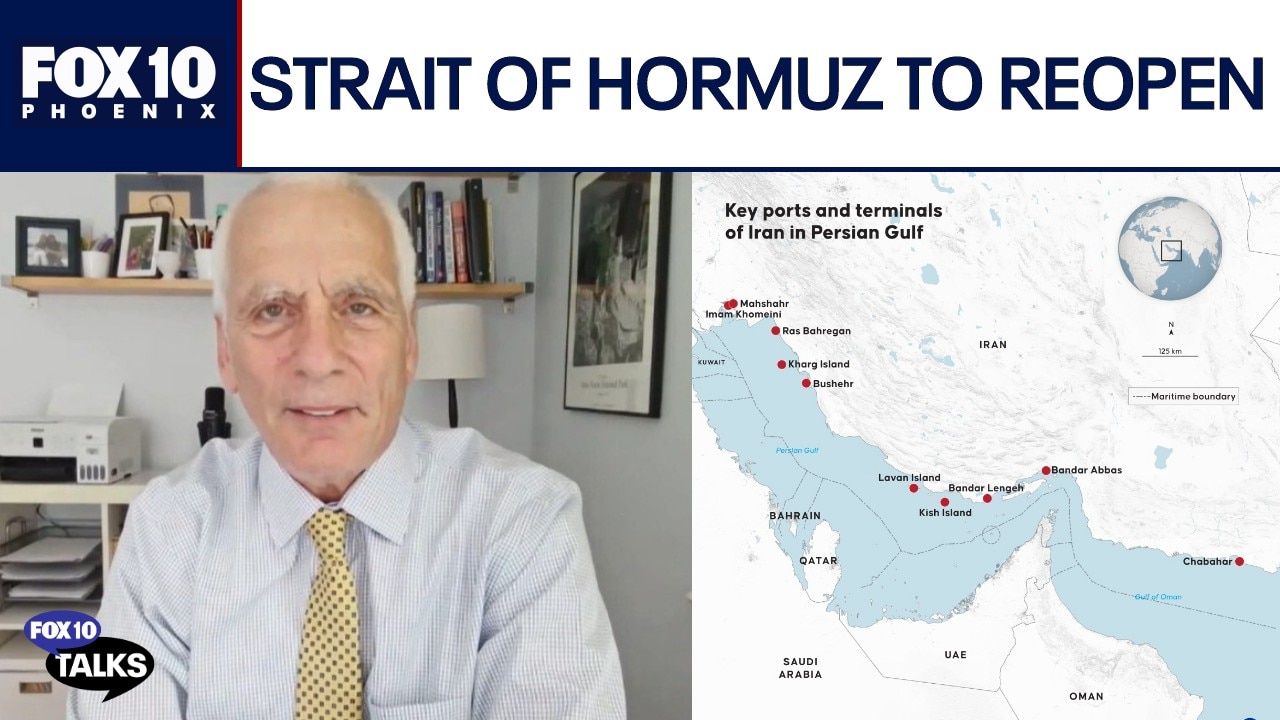

The Strait of Hormuz disruption represents the most severe global energy supply shock since February 28, 2025, when U.S.-Israeli aerial bombing triggered Iranian retaliation that has now extended into April 2025. According to Reuters reporting on April 20, 2025, the critical chokepoint carrying approximately 20% of global oil and gas supplies faces prolonged recovery challenges despite ceasefire negotiations. Iran's temporary reopening announcement was followed by renewed vessel attacks and closure warnings, trapping 13 million barrels per day of oil and 300 million cubic meters of LNG inside the Persian Gulf. For cross-border e-commerce sellers, this creates an immediate operational crisis: fuel surcharges on Asia-Pacific shipping routes are spiking 15-25% above baseline rates, with round-trip tanker voyages from the Middle East to India requiring 20 days and routes to China/Japan/South Korea extending to 60+ days.

The supply chain feedback loop is accelerating logistics costs across all fuel-intensive categories. According to analytics firm Kpler, 260 vessels carrying 170 million barrels of oil and 1.2 million metric tons of LNG remain trapped in the Gulf. The International Energy Agency reports commercial crude storage at 262 million barrels—equivalent to 20 days of disrupted production—meaning energy markets face sustained price pressure. Recovery projections are dire: 50% of Gulf oil and gas fields can return to pre-war output within two weeks under stable conditions, but 30% require six weeks, while the remaining 20% (2.5-3 million barrels daily) face severe technical obstacles. Tanker fleet rebalancing alone requires minimum 8-12 weeks, creating a cascading delay in shipping capacity availability. Qatar's Ras Laffan LNG hub suffered 12-17% capacity damage requiring up to five years for repairs, signaling structural energy supply constraints extending well beyond 2025.

For sellers, the immediate impact manifests in three critical areas: (1) Fuel surcharges on all Asia-Pacific shipments increasing 15-25%, compressing margins 8-12% for sellers with <20% gross margins; (2) Extended transit times of 8-12 weeks forcing inventory planning shifts away from just-in-time models; (3) Shipping insurance premiums rising 10-15% as underwriters price geopolitical risk. Sellers shipping electronics, apparel, and consumer goods from China/Vietnam/India to North America and Europe face the steepest cost increases. The Platts Dubai crude oil benchmark—pricing 18 million barrels daily—has become structurally disconnected from physical market reality, with the pricing mechanism reduced from five to two deliverable grades (cutting supply basket by 40%). This pricing instability creates hedging challenges for logistics providers, who pass volatility directly to sellers through variable fuel surcharges. Strategic sourcing shifts are accelerating: sellers should evaluate nearshoring to Mexico/Central America for North American markets and Eastern Europe for EU markets to reduce fuel-intensive ocean transit exposure. The timing window for proactive supply chain restructuring is 30-60 days before fuel surcharge escalations become permanent in carrier contracts.

Questions 8

What is the timeline for Hormuz disruption recovery and normal shipping?

Recovery will take years, not months, according to industry experts cited in Reuters reporting. The International Energy Agency estimates 50% of Gulf oil and gas fields can return to pre-war output within two weeks under stable conditions, but 30% require six weeks, while 20% face severe technical obstacles. Tanker fleet rebalancing alone requires minimum 8-12 weeks. Qatar's Ras Laffan LNG hub, damaged 12-17%, could require up to five years for repairs. Sellers should plan for elevated fuel surcharges through Q4 2025 minimum. Monitor ceasefire negotiations closely; any escalation extends timelines further. Establish contingency inventory plans assuming 12-16 week lead times through year-end 2025.

How should I adjust my pricing strategy during this shipping crisis?

Implement dynamic pricing that reflects fuel surcharge volatility: increase prices 8-12% on fuel-intensive categories (electronics, apparel, consumer goods) effective immediately. Use tiered pricing by destination: Asia-Pacific routes command 15-25% fuel surcharges, so North America/EU pricing should reflect this. For Amazon FBA sellers, update shipping cost assumptions in your profit calculator immediately; many sellers are seeing 20-30% margin compression on standard-size products. Consider offering expedited shipping options at premium pricing to offset fuel costs. Communicate transparently with customers about temporary price increases tied to geopolitical disruptions; transparency reduces return rates during crisis periods.