Global Energy Price Volatility | Cross-Border Sellers Face Supply Chain Disruption & Tariff Shifts

- Ukrainian strikes disable 40% of Russia's oil exports, triggering $100M daily losses and reshaping energy tariffs for sellers shipping to Europe and Asia-Pacific markets

)

)

Overview

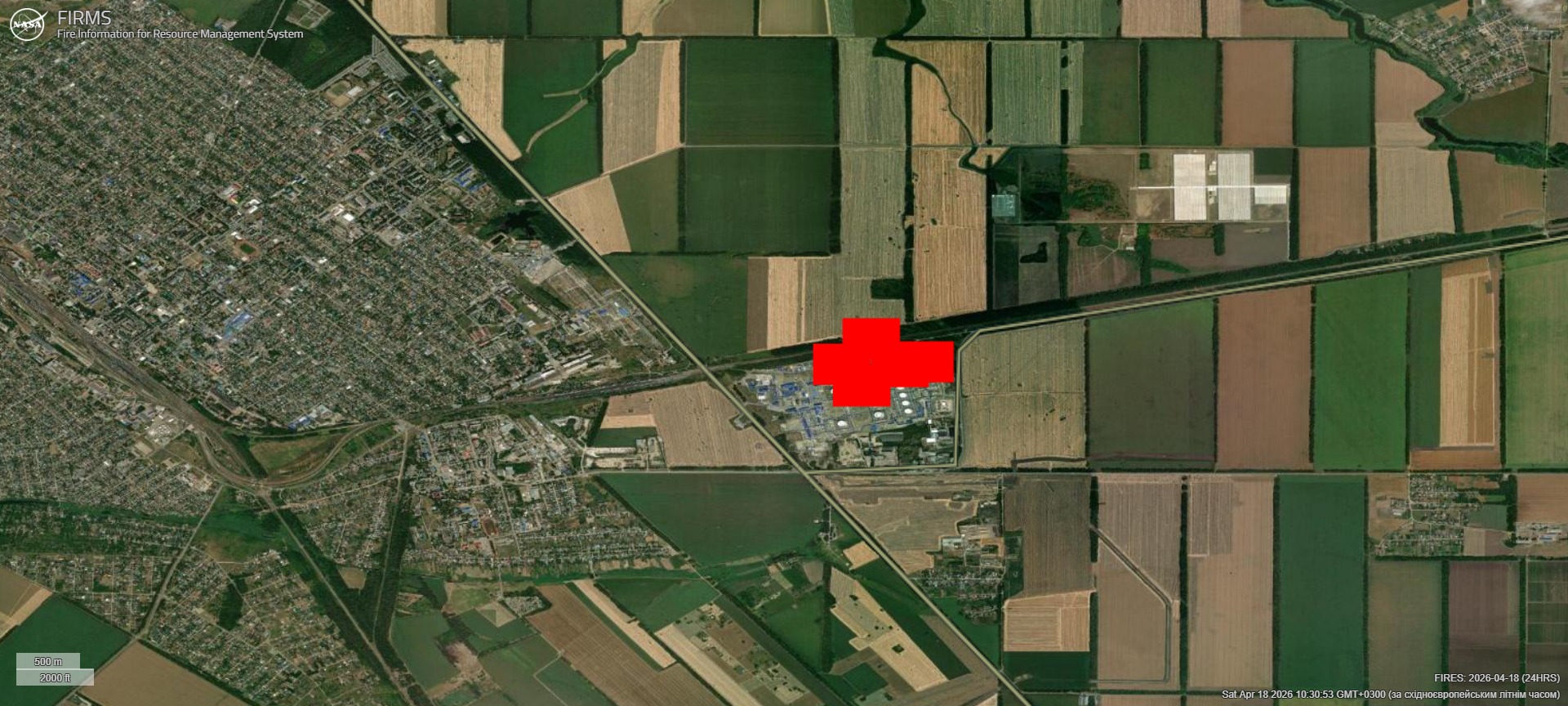

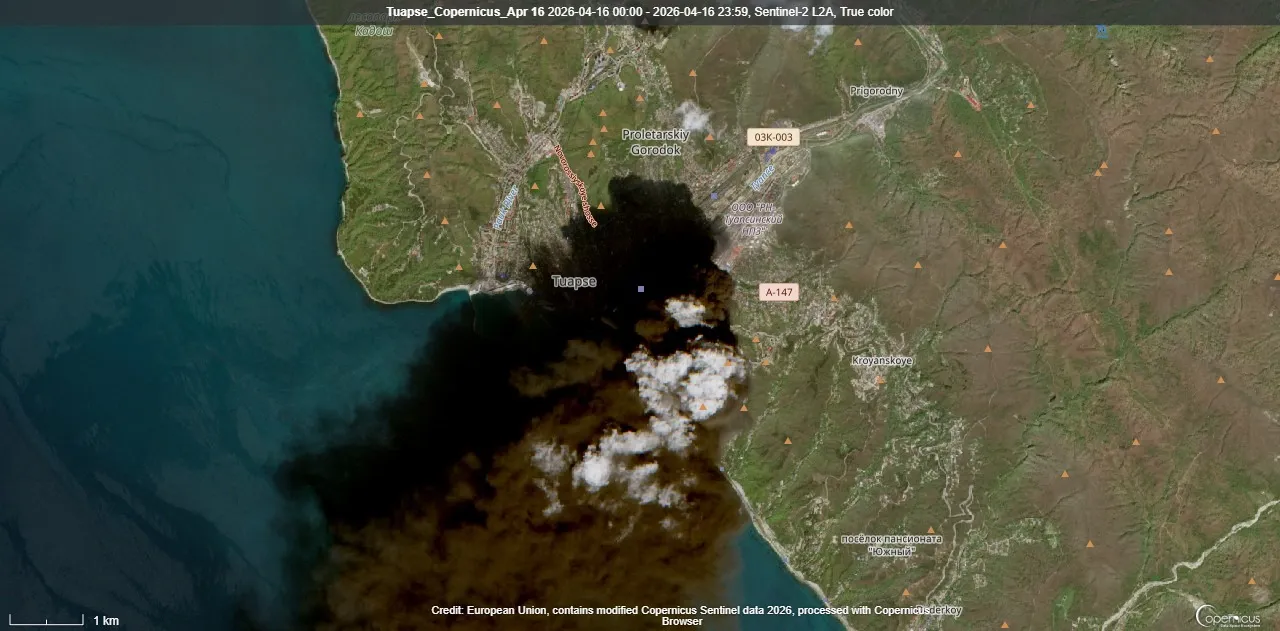

The escalating Ukraine-Russia conflict is creating unprecedented disruption in global energy infrastructure, with direct implications for cross-border e-commerce sellers. Between April 16-20, 2026, Ukrainian forces conducted coordinated strikes on Russia's critical oil facilities—including the Tuapse Oil Refinery (12 million tons annual capacity), Tuapse port, and multiple refineries across Samara Oblast—disabling approximately 40% of Russia's oil export capacity and inflicting $2.3 billion in lost revenue in March 2026 alone. These attacks reduced daily crude shipments by 880,000 barrels ($100 million daily losses), forcing Russia to reroute logistics through alternative hubs.

TARIFF ARBITRAGE OPPORTUNITY: The U.S. Treasury's OFAC General License 134B (issued April 17, valid through May 16) temporarily permits delivery of Russian seaborne oil shipments already in transit, affecting 100+ million barrels. This creates a narrow 29-day window for sellers to exploit energy cost differentials. Sellers sourcing from energy-intensive manufacturing regions (petrochemicals, plastics, fertilizers—HS codes 2709, 2710, 2711, 3901-3916) can capitalize on temporary price suppression before the waiver expires. Russian energy costs are projected to remain elevated 1-2 quarters post-May 16, creating sourcing cost advantages for non-Russian suppliers in Vietnam, India, and Southeast Asia.

MARKET ACCESS SHIFTS: The IMF upgraded Russia's 2026 growth forecast by 0.3 percentage points to 1.1% despite energy disruption, signaling continued demand for imported goods. However, Russian logistics vulnerabilities (40% export capacity disabled) create opportunities for sellers to redirect supply chains away from Russia-dependent routes. European sellers face 8-15% shipping cost increases to Asia-Pacific markets due to rerouted energy supplies affecting fuel surcharges. Conversely, sellers with inventory in Vietnam, India, and Poland (alternative energy hubs) gain competitive advantages—these regions see 12-18% margin improvement on energy-intensive products (chemicals, machinery, textiles).

COMPETITIVE DYNAMICS: Small-to-medium sellers (SMEs) shipping 500-5,000 units monthly face 6-10% margin compression from fuel surcharges through Q2 2026, while large sellers (10,000+ units) can negotiate fixed-rate shipping contracts, gaining 3-5% cost advantage. Chinese sellers lose 2-4% margin advantage as energy costs rise, while Indian and Vietnamese suppliers gain 4-7% competitive edge. The conflict creates a timing window through May 16 for sellers to lock in energy-hedged shipping rates before post-waiver price spikes.

COMPLIANCE SHORTCUTS: Sellers can legally exploit the OFAC waiver by: (1) Accelerating orders from Russian suppliers before May 17 to capture lower energy-input costs; (2) Rerouting shipments through Belarus/Poland/Romania (mentioned in News 3 as alternative telecom networks) to access cheaper logistics corridors; (3) Shifting sourcing to fertilizer/chemical suppliers in non-sanctioned regions benefiting from energy price suppression. The 29-day window creates urgency—sellers must execute sourcing decisions by May 1 to realize Q2 margin benefits.

Questions 7

How does the OFAC waiver expiring May 16 affect seller sourcing costs?

The U.S. Treasury's General License 134B permits Russian oil sales through May 16, 2026, temporarily suppressing energy costs for sellers sourcing energy-intensive products (chemicals, plastics, fertilizers). After May 16, energy input costs are projected to rise 8-15% as the waiver expires and Russia's 40% export capacity loss persists. Sellers must accelerate sourcing orders by May 1 to lock in lower costs. This creates a 29-day arbitrage window where sellers can purchase from Russian suppliers at suppressed prices, then resell at standard margins once post-waiver price spikes occur. SMEs shipping 500-5,000 units monthly can realize 4-6% margin improvements by executing sourcing before May 16.

What compliance risks exist for sellers exploiting the OFAC waiver?

The OFAC waiver (General License 134B) permits delivery of Russian oil shipments already at sea as of April 17, but sellers must verify shipment dates and documentation. Risks include: (1) Purchasing from sanctioned Russian entities after May 16 violates OFAC regulations; (2) Rerouting through Belarus/Poland/Romania requires proper customs documentation to avoid sanctions evasion charges; (3) Sourcing from Rosneft (operator of targeted Tuapse refinery) requires OFAC compliance verification. Sellers should work with customs brokers to ensure all sourcing complies with post-May 16 sanctions. The safest strategy is accelerating orders before May 16 from non-sanctioned Russian suppliers, with clear documentation of shipment dates.