Asian Tech Supply Chain Stabilization | Cross-Border Sellers Face Shipping Cost Volatility & Sourcing Opportunities

- Geopolitical tensions ease, unlocking Korean semiconductor sourcing; oil price volatility ($86-95/barrel) creates 8-15% shipping cost fluctuations for electronics sellers through Q2 2026

Overview

Geopolitical De-escalation Opens Korean Tech Supply Chain Opportunities for Cross-Border Sellers

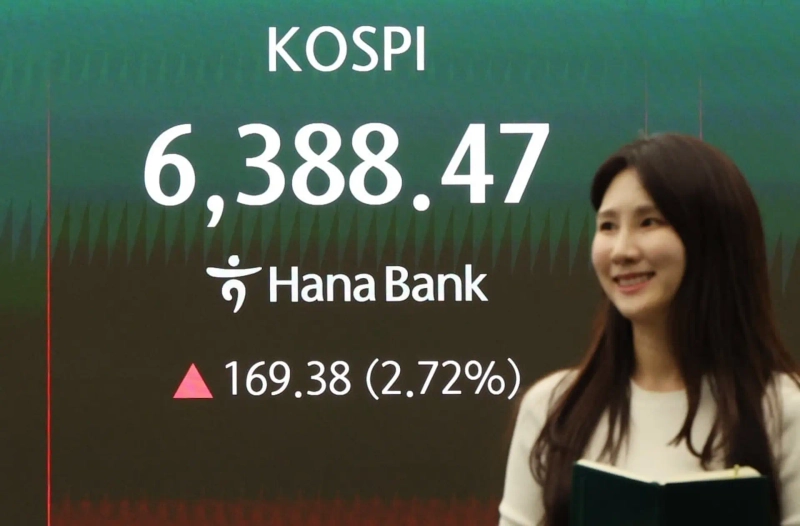

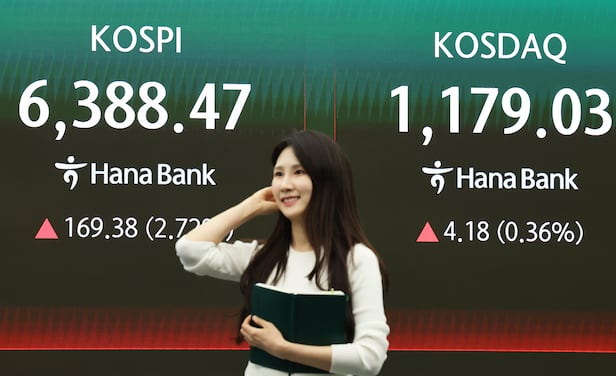

The April 2026 U.S.-Iran ceasefire negotiations represent a critical inflection point for cross-border e-commerce sellers sourcing from Asia. South Korea's KOSPI index surged to a record 6,388.47 points (up from 6,307.27 on February 26), driven by renewed investor confidence in semiconductor manufacturers SK Hynix and Samsung Electronics. This 1.3% recovery follows a devastating 19% market decline in March when Iran's closure of the Strait of Hormuz paralyzed shipping routes and spiked oil prices above $100/barrel. The immediate impact: Brent crude stabilized at $94.92-$95.10/barrel (down from $100+ peak), reducing logistics costs for sellers shipping electronics, smart devices, and tech accessories from Korean suppliers.

Supply Chain Cost Dynamics & Sourcing Arbitrage Opportunities

For cross-border sellers, the Korean tech sector's recovery creates two distinct opportunities. First, memory chip shortages extending through 2027 (per industry projections) signal sustained pricing power for Korean chipmakers, meaning sellers sourcing AI-related hardware, high-bandwidth memory (HBM) components, and DRAM-dependent devices face 5-12% cost increases if they delay procurement. Samsung Electronics reported record Q1 2026 operating profits exceeding 50 trillion won, driven by AI chip demand—indicating production capacity constraints and potential lead time extensions. Second, the geopolitical stabilization reduces supply chain disruption premiums. Foreign investors who net-sold 35 trillion won ($23.8 billion) of Korean stocks in March have returned to the market, signaling confidence in logistics normalization. Sellers should front-load Korean semiconductor and component orders by May 2026 before supply tightens further.

Currency Volatility & Pricing Strategy Adjustments

The U.S. dollar strengthened to 158.98 Japanese yen (from 158.82), while the euro weakened to 1.1782—creating favorable conditions for USD-based sellers sourcing from Korea but challenging for EUR-based competitors. For sellers using Amazon FBA, eBay, or Shopify to distribute electronics globally, the 0.16 yen appreciation translates to approximately 0.1% cost reduction on Korean imports, modest but meaningful at scale (100+ units monthly). However, oil price volatility remains the primary cost driver: each $5/barrel swing in Brent crude affects shipping costs by 2-3% for air freight and 1-2% for ocean freight. Sellers should lock in shipping rates through Q2 2026 and consider hedging strategies if sourcing >$50K monthly from Korean suppliers. The fragile ceasefire (with unclear prospects for renewed negotiations per the April 21 reports) means risk premiums could resurface if talks collapse, potentially spiking oil to $100+/barrel again.

Competitive Positioning: Korean Tech Brands vs. Third-Party Sellers

South Korea's position as a critical supplier in global e-commerce supply chains strengthens as KOSPI-listed firms expand capacity. Samsung Electronics and SK Hynix are filing for U.S. listings to fund AI chip expansion, indicating capital availability for production scaling. This benefits third-party sellers competing in electronics categories (HS codes 8471-8517 covering computers, semiconductors, telecommunications equipment) by improving component availability, but also increases competition from Korean brand sellers entering Amazon and eBay directly. Goldman Sachs raised its 12-month KOSPI target from 7,000 to 8,000 points, and JPMorgan Chase designated South Korea as a top preferred regional market with an 8,500-point bull case—signaling sustained investor confidence and likely continued Korean export growth. Sellers should monitor Korean brand entry into their categories and consider differentiation through bundling, value-added services, or niche positioning rather than competing on price alone.

Questions 7

Which product categories benefit most from Korean supply chain stabilization?

AI-related hardware, high-bandwidth memory (HBM) components, DRAM-dependent devices, smartphones, and smart home electronics benefit most from Korean supply stabilization. Samsung Electronics' record Q1 2026 profits (driven by AI chip demand) indicate sustained production capacity for these categories. Sellers in laptops, gaming devices, and data center equipment should prioritize Korean sourcing. Conversely, non-AI consumer electronics (basic smartphones, standard storage devices) face 5-12% cost increases due to supply constraints. Consider shifting product mix toward AI-enabled devices or bundling standard electronics with AI-powered accessories to capture margin improvements.

What are the compliance and logistics considerations for shipping electronics from Korea via Amazon FBA?

**Amazon FBA** requires proper HS code classification for electronics (8471-8517 range), battery certifications (UL, CE, FCC), and country-of-origin labeling. Korean suppliers typically handle these, but verify before ordering. Shipping from Korea to Amazon FBA warehouses typically takes 3-4 weeks via ocean freight (cost: $2-5/unit for standard electronics) or 5-7 days via air freight (cost: $8-15/unit). Given current oil prices at $94.92/barrel, lock in ocean freight rates to avoid potential spikes if geopolitical tensions resurface. For **eBay** sellers, ensure Korean suppliers provide proper documentation for international shipping and customs clearance.