Data Center Power Surge & Clean Energy Shift | Critical Cost Implications for E-Commerce Sellers 2025-2026

- Data centers drove 50% of U.S. electricity growth in 2025; clean energy now meets demand growth while fossil fuels flatten, creating divergent cost pressures for sellers across cloud infrastructure, manufacturing, and logistics operations

Overview

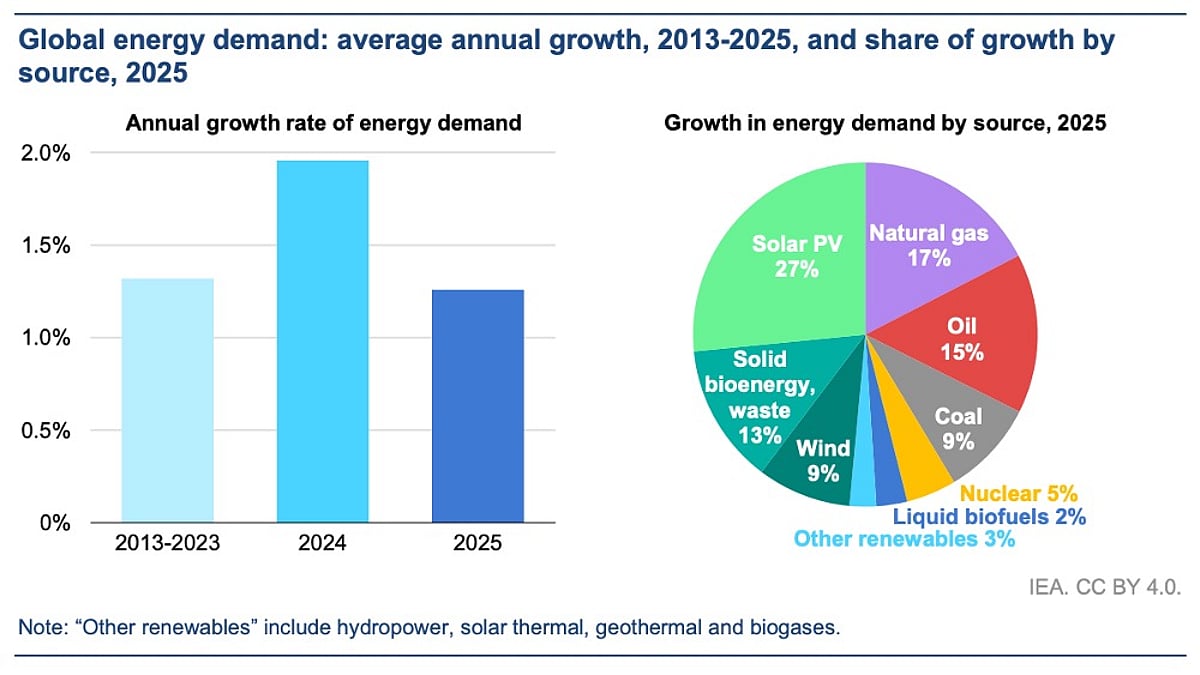

The global energy landscape experienced a structural inflection point in 2025, with two simultaneous but contradictory trends reshaping operational costs for cross-border e-commerce sellers. According to the International Energy Agency's April 2025 Global Energy Review, data centers drove approximately 50% of U.S. electricity demand growth in 2025, with global electricity demand surging 3%—nearly triple the overall energy consumption growth rate of 1.3%. Simultaneously, research from Ember revealed that clean energy generation exceeded global electricity demand growth for the first time, with solar power rising nearly one-third and renewable energy reaching 34% of global generation, surpassing coal's 33% share.

These parallel developments create a complex cost environment for sellers. The data center surge directly impacts Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform infrastructure costs that sellers depend on for inventory management, order processing, and customer analytics. The IEA warns that increased hosting costs and potential service capacity constraints during peak seasons (Q4 2024-Q1 2025) will compress margins for technology-dependent operations. U.S. electricity demand grew 2% in 2025 (down from 2.8% in 2024), but remained above the 2014-2024 average, signaling sustained infrastructure pressure through 2026.

However, the clean energy transition offers long-term cost relief. China and India—critical sourcing regions for 60% of cross-border sellers—are leading renewable adoption, with China producing over 50% of global solar growth and India reducing fossil fuel generation by 52 terawatt hours. Sellers sourcing from or operating manufacturing facilities in these regions benefit from declining renewable energy costs (battery storage costs dropped sharply, with 14% of solar generation now stored for off-peak use). Yet infrastructure modernization requirements may temporarily increase operational costs in some regions through 2026.

The divergence creates a bifurcated risk profile: short-term cloud infrastructure cost increases (2025-2026) offset by medium-term manufacturing cost reductions (2026+) in renewable-heavy regions. Sellers must balance immediate AWS/Azure budget increases against strategic sourcing advantages in China and India. The global energy demand slowdown (1.3% growth vs. 1.4% historical average) reflects reduced cooling demand in Asia and slower economic growth, potentially easing some pressure by late 2025. More than 50 countries meeting in Colombia to discuss fossil fuel transition signals accelerating policy momentum that will reshape energy costs across all seller operating regions through 2026 and beyond.

Questions 8

Which e-commerce categories are most vulnerable to energy cost increases?

Energy-intensive categories face the highest margin pressure: (1) **Electronics/Computing** (high cloud infrastructure dependency for inventory management and analytics), (2) **Appliances/HVAC** (manufacturing energy costs), (3) **Perishables/Cold Chain** (fulfillment center cooling costs), (4) **Heavy/Bulky items** (logistics energy for transportation). Conversely, **low-energy categories** (apparel, accessories, digital products) see minimal impact. Sellers in electronics should prioritize cloud cost optimization and consider shifting to 3PL providers with renewable energy facilities. Perishable sellers should evaluate cold chain logistics partners investing in renewable energy. Digital product sellers face minimal energy cost increases and gain competitive advantage as traditional sellers' margins compress.

How can I calculate the total impact of energy costs on my seller margins for 2025-2026?

Break energy costs into three categories: (1) **Cloud infrastructure**: Calculate current AWS/Azure monthly bills and apply 8-15% increase estimate for 2025-2026. Example: $5,000/month bill × 12% = $600/month increase ($7,200 annually). (2) **Fulfillment costs**: If using FBA, energy represents 8-12% of fulfillment fees; expect 2-3% increases. Example: $10,000/month FBA fees × 10% energy component × 2.5% increase = $25/month impact. (3) **Manufacturing**: If sourcing from China/India, expect 3-5% cost reductions by 2026 from renewable energy adoption. Model scenarios with 10%, 15%, and 20% cloud cost increases to understand margin compression. Most sellers see 1-3% overall margin compression in 2025-2026, offset by manufacturing savings in 2026+.