Strait of Hormuz Shipping Crisis | Freight Costs Rise 10-20% for Cross-Border Sellers

- Geopolitical tensions permanently reshape energy logistics; sellers face sustained 12-24 month cost pressures and supply chain volatility across all shipping corridors

Overview

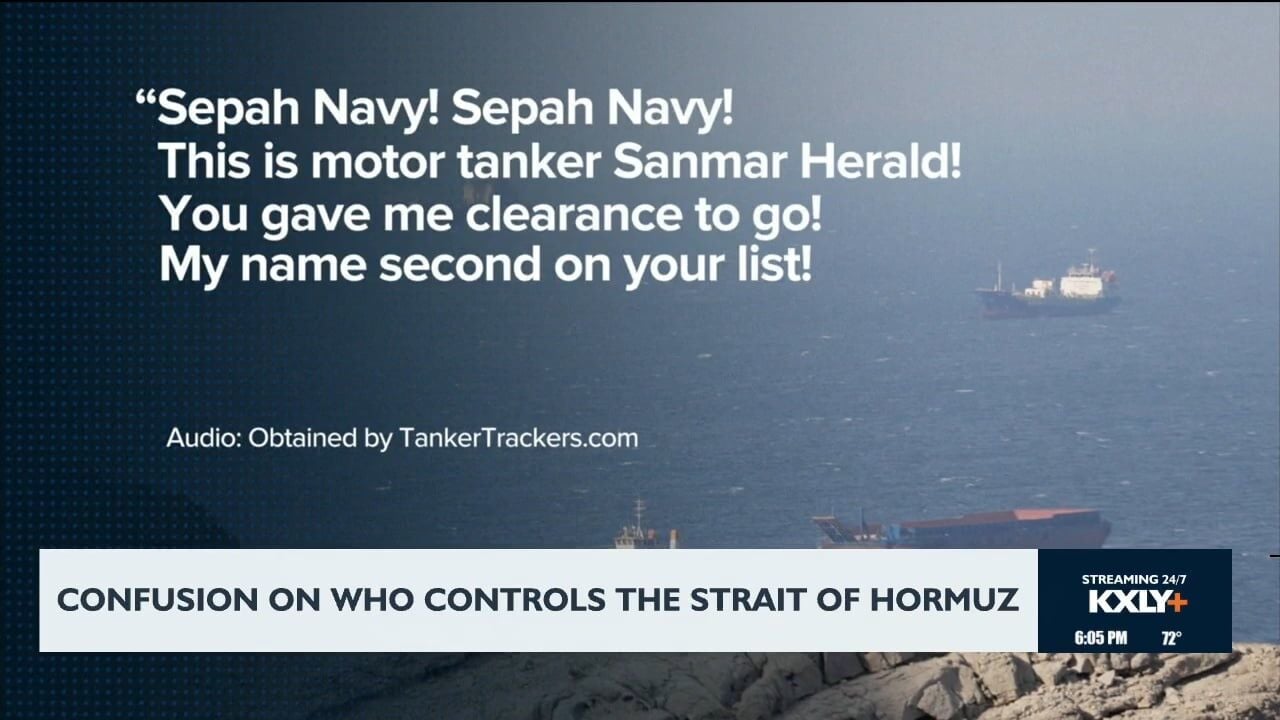

The Strait of Hormuz disruption represents the largest energy supply crisis on record, with 21% of global petroleum normally transiting through this critical chokepoint now facing permanent rerouting due to U.S.-Israeli-Iran tensions. The International Energy Agency (IEA) characterizes this as exceeding 1970s oil shocks combined, directly impacting cross-border e-commerce logistics through elevated fuel surcharges and extended transit times. For international sellers, this translates to freight rate increases of 10-20% depending on routes and fuel surcharges, with longer delivery windows resulting from rerouting via alternative straits like Bab el-Mandeb—which faces additional security risks from Houthi attacks.

Current alternative pipeline capacity remains severely constrained. Saudi Arabia's EastWest Pipeline operates at 4.5 million barrels per day (bpd) against 7 million bpd capacity; the UAE's Habshan-Fujairah Pipeline (ADCOP) has experienced drone attacks since late February; Iraq's Kirkuk-Ceyhan Pipeline through Turkey restarted in September after 12-year shutdown, currently pumping 170,000 bpd with plans to reach 250,000 bpd; and Iran's Goreh-Jask Pipeline (1 million bpd capacity) remains under construction. This infrastructure bottleneck signals sustained logistics cost pressures for 12-24 months as alternative corridors reach full capacity. Sellers relying on just-in-time inventory models face increased supply chain vulnerability and potential delays receiving goods from Middle Eastern suppliers or shipping to Asian markets.

The structural shift is permanent, not temporary. According to April 2026 New York Times reporting, energy industry executives confirm the strait will not return to pre-crisis operational norms regardless of reopening status. Regional governments have implemented long-term infrastructure diversification strategies, with Saudi Arabia and UAE rerouting substantial oil volumes through existing bypass pipelines. This represents permanent shifts in energy logistics rather than contingency measures. For cross-border sellers—particularly those in energy-dependent sectors or reliant on Middle Eastern supply chains—these developments signal sustained logistics cost pressures and supply chain volatility. Immediate actions include reviewing inventory positioning, evaluating 3PL provider alternatives, and adjusting pricing models to absorb 8-15% freight cost increases over the next 18-24 months. Sellers should monitor alternative shipping corridors (Red Sea routes via Yanbu, Turkey-Iraq pipelines) and consider strategic sourcing shifts to reduce Middle Eastern supply chain exposure.

Questions 8

How much will freight costs increase for cross-border sellers due to Strait of Hormuz disruption?

Freight rates are rising 10-20% depending on routes and fuel surcharges, with the increase sustained for 12-24 months as alternative pipeline corridors reach full capacity. For sellers shipping 1,000+ units monthly via ocean freight, this translates to $200-500 additional monthly costs per container. The **International Energy Agency (IEA)** characterizes this as the largest supply disruption on record, exceeding 1970s oil shocks combined. Sellers should immediately audit shipping contracts and evaluate 3PL providers offering fixed-rate agreements to lock in current pricing before further increases occur.

Which shipping routes are most affected by the Hormuz crisis?

The Strait of Hormuz normally handles 21% of global petroleum, making it the world's most critical oil chokepoint. Rerouting now occurs via alternative straits like Bab el-Mandeb, which faces security risks from Houthi attacks, adding 5-10 days to transit times. Alternative pipelines include Saudi Arabia's EastWest Pipeline (4.5 million bpd effective capacity), UAE's Habshan-Fujairah Pipeline (1.5-1.8 million bpd, drone-attacked since February), Iraq's Kirkuk-Ceyhan Pipeline through Turkey (170,000 bpd, expanding to 250,000 bpd), and Iran's Goreh-Jask Pipeline (1 million bpd, under construction). Sellers shipping to/from Asia should expect 7-14 day delays on affected routes.