Geopolitical Oil Shock Reshapes US Consumer Spending | Sellers Must Pivot to Value Categories

- 24.1% gasoline price surge redirects $857+ annual household spending away from discretionary retail; core sales growth drops to 0.7% as consumer strain signals Q2 deceleration

Overview

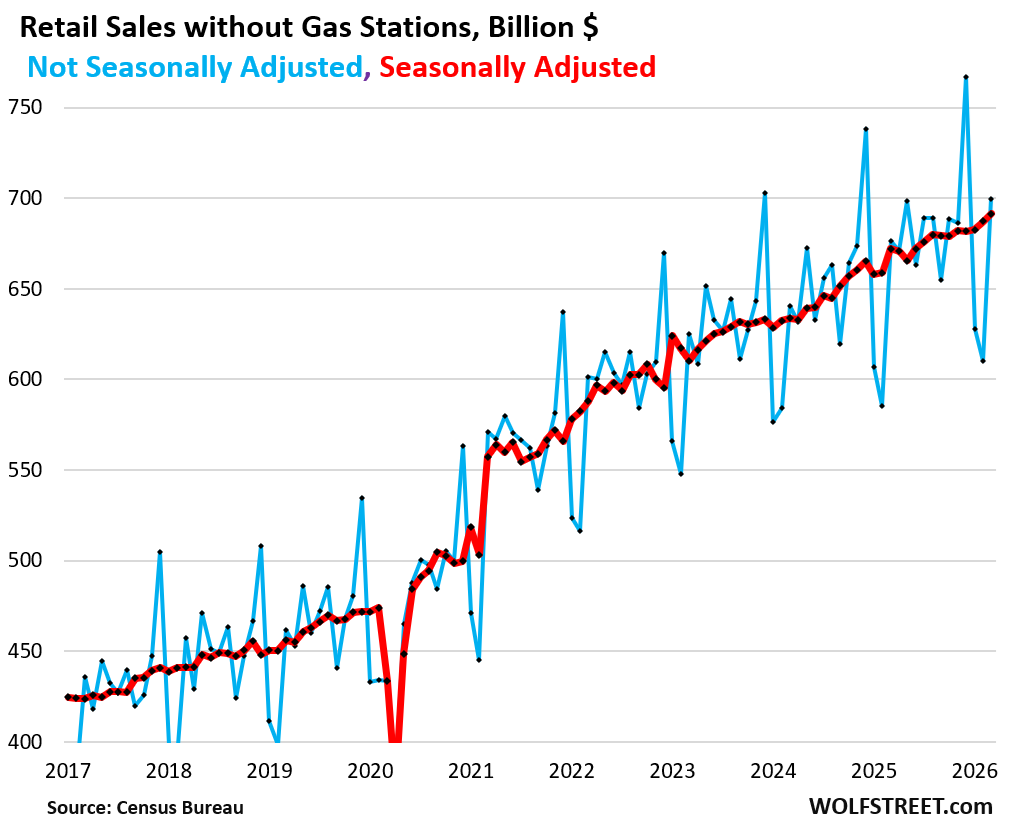

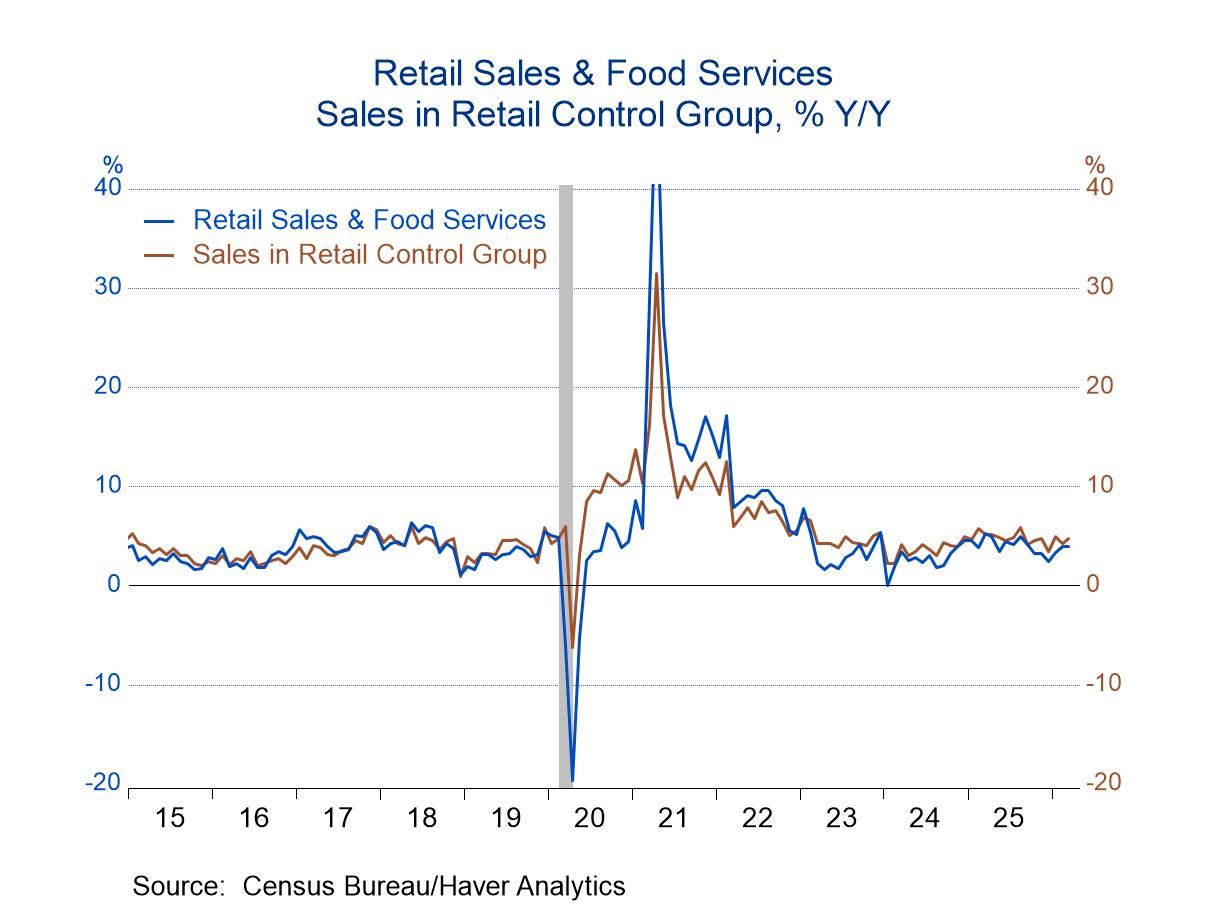

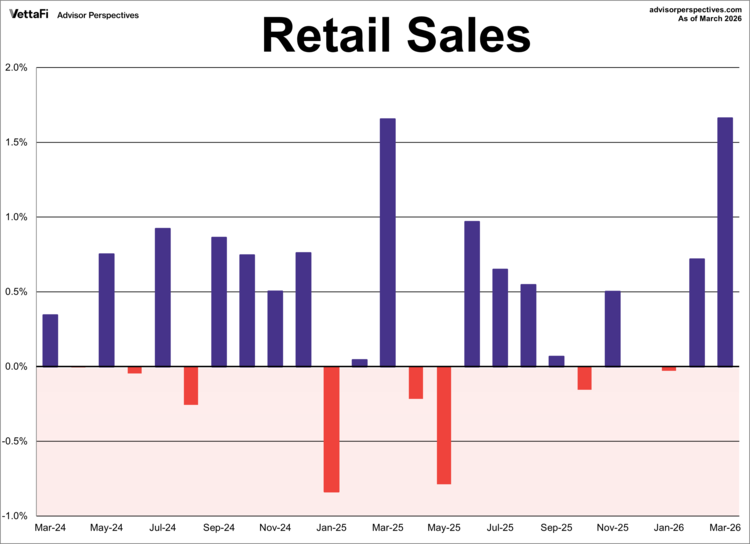

The March 2026 retail data reveals a critical bifurcation in US consumer spending driven by geopolitical oil shocks: while headline retail sales surged 1.7% (beating economist expectations of 1.4%), this masks severe underlying weakness in discretionary categories that directly impacts e-commerce sellers. Gasoline station receipts jumped 15.5%—the highest gain since 1992—as Middle East tensions sent global oil prices soaring 30%+, with US retail gasoline prices climbing 24.1% in March alone. This energy cost shock is functioning as a consumption tax, redirecting household budgets away from apparel, sporting goods, and food service (which grew only 0.1% in March, down from 0.5% in February).

For cross-border e-commerce sellers, the operational implications are severe. Core retail sales (excluding automobiles, gasoline, building materials, and food services) increased only 0.7%—signaling that underlying consumer momentum remains fragile despite tax refund support averaging $351 higher than 2023. Federal Reserve Beige Book reports document "signs of consumer financial strain, increased price sensitivity" across districts, with consumer sentiment plunging to record lows. Households are increasingly tapping savings to maintain spending while wage growth has slowed, indicating they're becoming "increasingly selective" with discretionary purchases. The Stanford Institute estimates war-driven price spikes increased Americans' average annual gasoline costs by $857 for 2024—a burden that crowds out spending on Amazon apparel, eBay sporting goods, and Shopify-powered fashion retailers.

The offline-to-online (O2O) opportunity emerges in value-driven categories and geographic targeting. Sellers should immediately pivot inventory toward budget-conscious segments: private label essentials, value-pack offerings, and price-competitive categories where consumers are still spending (food, household basics, health/wellness). High-traffic urban centers with elevated fuel costs (California, Texas, Northeast corridor) will see the most pronounced shift toward online shopping as consumers avoid discretionary trips. Pop-up showrooms in suburban areas with lower gas prices can capture price-sensitive shoppers seeking tangible product verification before purchase. Retail partnerships with discount chains (Dollar General, Walmart, Target) offer lower-cost offline touchpoints than premium venues. The 0.7% core retail growth rate suggests Q2-Q3 deceleration ahead as tax refund benefits fade, making immediate inventory repositioning and margin optimization critical for sellers dependent on discretionary categories.

Questions 8

What supply chain and logistics adjustments should sellers prioritize given geopolitical oil price volatility?

The 30%+ global oil price increase driven by Middle East tensions creates immediate supply chain risks for sellers relying on air freight and long-haul trucking. Sellers should immediately shift 40-60% of inventory from air freight to ocean freight (despite longer lead times) to reduce logistics costs by 25-35%. Amazon FBA sellers should consolidate shipments to reduce per-unit fulfillment costs by 10-15%. Shopify sellers should negotiate fixed-rate shipping contracts with 3PL providers through Q4 2026 to hedge against further oil price volatility. The Energy Information Administration confirmed dramatic price spikes, suggesting sustained elevated fuel costs through 2026. Sellers should increase inventory safety stock by 15-20% to accommodate longer ocean freight lead times while reducing air freight exposure. Regional distribution centers in lower-cost logistics hubs (Texas, Georgia) offer 20-30% cost savings compared to coastal facilities.

How do apparel and sporting goods sellers adjust pricing strategy during this consumer strain period?

Apparel and sporting goods sales grew only 0.1% in March (down from 0.5% in February), signaling severe price sensitivity among consumers. Sellers should implement tiered pricing strategies: maintain premium positioning for 10-15% of SKUs targeting affluent segments, shift 60-70% of inventory to value-competitive pricing (10-20% below historical margins), and introduce budget sub-brands for 15-25% of portfolio. Amazon sellers should increase reliance on Subscribe & Save programs (which show 25-35% higher retention during economic strain) and bundle offerings that emphasize value. Shopify sellers should implement dynamic pricing that adjusts based on competitor pricing and inventory levels. The $857 annual gasoline cost increase per household directly compresses discretionary budgets, requiring sellers to emphasize value messaging and price transparency to maintain conversion rates.