Vietnam Social Commerce Boom 2026 | TikTok Shop & Shopee Dominate Video-First Market

- Market projected to reach $20.98B in 2026 (11.5% annual growth); livestream commerce and creator partnerships reshape seller strategies across Southeast Asia

Overview

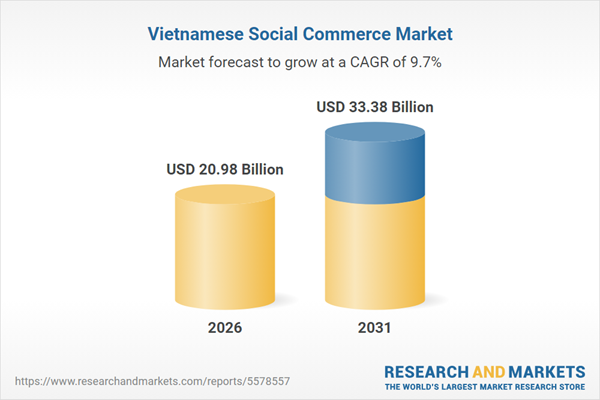

Vietnam's social commerce market is experiencing transformative growth, with the sector projected to reach USD 20.98 billion in 2026 and expand to USD 33.38 billion by 2031 at a 9.7% CAGR. This represents a critical inflection point for cross-border sellers targeting Southeast Asia's fastest-growing e-commerce market. The market demonstrated a 12.7% CAGR from 2022-2025, signaling sustained momentum driven by fundamental shifts in how Vietnamese consumers engage with digital commerce.

The structural transformation centers on four critical platform dynamics that directly impact seller strategy. First, livestream and short-video formats have become primary sales channels, with Shopee Live and TikTok Shop integrating video-driven commerce as core functionality. TikTok is notably expanding local teams in Ho Chi Minh City to scale livestream operations, recognizing that Vietnamese consumers require product demonstrations and interactive reassurance before purchase—a behavioral shift that demands sellers invest in video content capabilities rather than static product listings. Second, creator commerce is evolving from awareness-building to managed sales channels, exemplified by Shopee's Meta partnership and VECOM's KLIC chapter establishment in Ho Chi Minh City. This signals that influencer partnerships are no longer optional marketing tactics but essential fulfillment channels. Third, platforms are tightly integrating content operations with seller supply chains, as demonstrated by TikTok's "Semi-fulfillment Project," which aligns inventory management with content strategy to address stock availability and after-sales service challenges. This integration creates operational complexity but also competitive moats for sellers who master platform-specific fulfillment models.

The competitive landscape is consolidating around two dominant platforms with distinct strategic positioning. Shopee maintains market leadership through integrated marketplace and content infrastructure, while TikTok Shop gains significant traction via creator-led strategies. Lazada focuses on authenticity positioning, while Tiki's influence is declining. Critically, new entrants like Temu and Shein face regulatory obstacles, indicating that Vietnam's regulatory environment is tightening. The market is advancing toward formalized regulation with new laws covering network responsibilities, seller verification, and market surveillance, elevating operational standards for verified sellers and brands. This regulatory shift creates barriers to entry for unvetted sellers but legitimizes the market for compliant cross-border operators.

For cross-border e-commerce sellers, this represents both significant opportunity and operational complexity. The shift toward video-led selling requires content creation capabilities and creator partnerships—sellers cannot rely on traditional PPC and SEO strategies. Sellers must adapt to platform-specific fulfillment models and comply with increasingly stringent verification and traceability requirements. The market's consolidation around Shopee and TikTok Shop suggests sellers should prioritize presence on these platforms while developing creator collaboration strategies to drive conversions in this video-first environment. Sellers with existing Southeast Asia operations should accelerate Vietnam expansion, while new entrants should budget 3-6 months for creator partnership development and platform compliance before achieving meaningful sales velocity.

Questions 8

Which product categories show highest potential in Vietnam's livestream commerce?

Product categories requiring demonstration and interactive reassurance show highest potential in Vietnam's livestream commerce environment. Fashion, beauty, electronics, and home goods perform well because livestream formats allow sellers to showcase fit, color accuracy, functionality, and lifestyle integration. Categories like cosmetics benefit from real-time application demonstrations, while electronics gain from detailed feature walkthroughs. The market's emphasis on 'interactive reassurance before purchase' suggests categories with high return rates or consumer uncertainty perform best on livestream. Sellers should prioritize categories where video demonstration directly addresses purchase hesitation—this is why Shopee Live and TikTok Shop focus on these verticals rather than commodities.

What is the competitive advantage of Shopee's Meta partnership for sellers?

Shopee's Meta partnership enables seamless content-to-commerce workflows, allowing sellers to leverage Facebook and Instagram content directly within Shopee's marketplace. This integration reduces friction between creator awareness campaigns and sales conversion, enabling creators to drive traffic directly to seller storefronts. VECOM's KLIC chapter establishment in Ho Chi Minh City formalizes creator commerce as a managed sales channel rather than organic marketing. For sellers, this means creator partnerships are now structured, measurable, and integrated into platform fulfillment—creators can manage inventory, handle customer service, and track performance within Shopee's ecosystem. This transforms influencer marketing from awareness-building to direct sales responsibility.