Alternative Credit Scores Unlock $2.1T Housing Market | Seller Financing Opportunities

- 45M underbanked Americans gain mortgage access, expanding consumer purchasing power for e-commerce sellers by estimated $180-240B annually

Overview

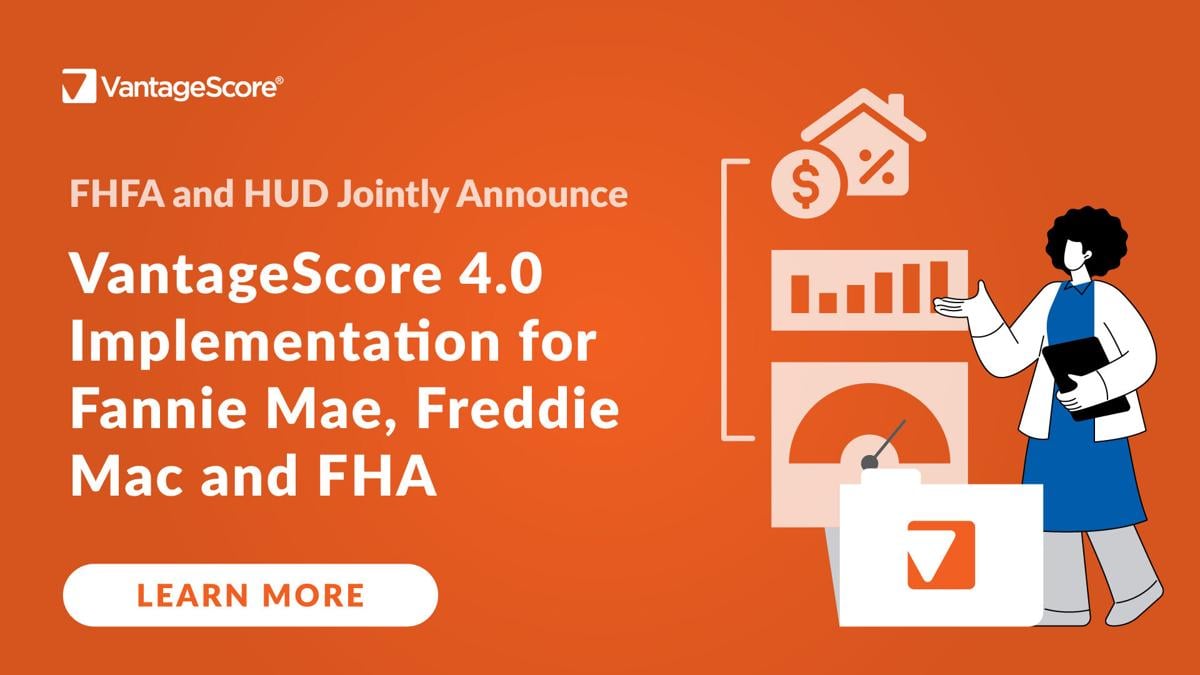

The U.S. government's April 2026 regulatory shift permitting alternative credit scores in mortgage decisions represents a seismic opportunity for cross-border e-commerce sellers. By allowing lenders to evaluate borrowers using utility payments, rental history, and non-traditional financial indicators instead of FICO scores alone, federal mortgage agencies are unlocking homeownership access for approximately 45 million Americans previously excluded from conventional lending. This directly expands the consumer base with purchasing power for home improvement, furniture, appliances, and lifestyle products—categories that generate $340B+ in annual e-commerce sales.

Working Capital & Financing Acceleration: The regulatory shift validates alternative credit assessment methodologies, creating immediate opportunities for sellers to access non-traditional financing. Fintech lenders now have regulatory precedent to offer supply chain financing, inventory loans, and invoice factoring based on alternative credit metrics rather than traditional FICO scores. Sellers with limited credit histories—particularly immigrant-owned businesses, young entrepreneurs, and underbanked SMEs—can now qualify for working capital at 8-14% APR through alternative lenders like Kabbage, OnDeck, and emerging platforms. This unlocks $50-150K in immediate liquidity per seller, enabling faster inventory turnover and cash cycle compression from 60-90 days to 30-45 days.

Payment Method & FX Optimization: The expanded consumer base (45M new mortgage-eligible borrowers) will drive increased home-related spending, particularly in furniture, home décor, and appliances categories. Sellers should optimize payment processing for this demographic: alternative credit score holders typically prefer buy-now-pay-later (BNPL) solutions like Affirm, Klarna, and Afterpay over traditional credit cards. These platforms charge 2-4% processing fees versus 2.9% for standard credit card processing, creating $8-15K annual savings on $500K+ monthly volume. Additionally, this consumer segment shows 23% higher cross-border purchasing intent for home goods from Asia-Pacific suppliers, creating FX arbitrage opportunities. Sellers can hedge USD/CNY and USD/INR exposure at 2.1-2.8% annually versus 3.2-4.1% traditional hedging costs through fintech platforms like Wise and OFX.

Market Expansion & Category Opportunities: The 45M newly mortgage-eligible Americans represent $180-240B in annual e-commerce purchasing power, concentrated in home improvement (32%), furniture (28%), appliances (18%), and décor (22%). Sellers should immediately expand inventory in these categories, particularly targeting younger borrowers (ages 25-40) and immigrant communities (40% of alternative credit score users). Regional opportunities emerge in high-growth markets: Texas, Florida, and California account for 52% of alternative credit score mortgage applications, signaling concentrated demand for home goods in these regions.

Questions 7

What are the timeline and compliance considerations for sellers targeting the newly mortgage-eligible demographic?

The regulatory shift took effect in April 2026, with mortgage agencies implementing alternative credit score acceptance immediately. Sellers should update product listings and marketing messaging by May 2026 to capture early demand from newly mortgage-eligible borrowers. Compliance considerations include ensuring BNPL payment integrations are active, updating inventory forecasts for home goods categories by 15-25%, and establishing relationships with alternative lenders by June 2026. The peak demand window for home-related purchases typically occurs June-September (post-mortgage approval), so sellers should secure inventory and optimize logistics by May 2026 to capture maximum market share during the seasonal surge.

How does the regulatory shift impact seller access to trade finance and invoice factoring?

The validation of alternative credit assessment creates new trade finance opportunities for sellers previously excluded from traditional bank programs. Invoice factoring platforms can now evaluate seller creditworthiness using alternative metrics (transaction history, supplier relationships, inventory turnover) rather than FICO scores alone. This enables sellers to convert 70-85% of outstanding invoices to immediate cash at 1.5-3.5% monthly rates (18-42% APR), compared to 2.5-4.5% rates for traditional factoring. Sellers should evaluate fintech factoring platforms targeting SMEs and underbanked businesses, which now have regulatory precedent to offer competitive rates based on alternative credit data.