Enterprise Software Infrastructure Volatility Creates Seller Opportunity Window in Supply Chain Automation

- ServiceNow stock decline 50%+ from highs despite 22% revenue growth signals market mispricing; geopolitical headwinds create 6-12 month window for sellers to lock in favorable SaaS contracts before enterprise IT spending rebounds

Overview

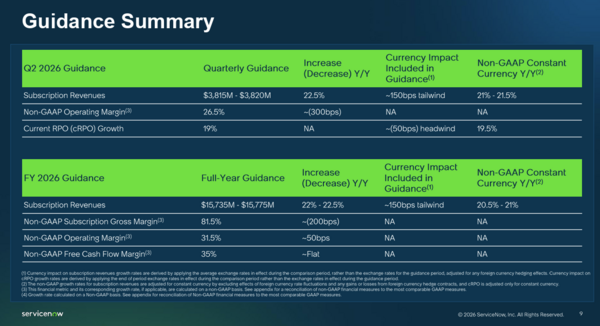

ServiceNow's Q1 2025 earnings reveal a critical market disconnect with direct implications for cross-border e-commerce sellers relying on enterprise infrastructure. The company delivered $3.77 billion in revenue (22% YoY growth), raised full-year 2026 guidance by $210 million to $15.74-15.78 billion, and achieved $1.5 billion AI revenue run rate (50% YoY growth), yet the stock plummeted over 50% from its $211.48 peak to below $90 in after-hours trading—a 17% single-day decline attributed to Iran geopolitical tensions impacting Middle East sales.

The Enterprise Software Spending Paradox: Despite acknowledging a 75 basis point Middle East headwind, ServiceNow raised guidance across all metrics: 32% operating margin, 36% free cash flow margin, and $27.7 billion remaining performance obligations (RPO)—representing nearly two years of signed contracts. The company closed 16 transactions worth $5M+ in new annual contract value (80% YoY growth), with 630 customers now spending $1M+ annually. This indicates large enterprises are increasing rather than reducing technology spending, contradicting market pessimism.

Seller Implications Through Supply Chain Automation: For cross-border e-commerce sellers, ServiceNow's infrastructure powers critical backend systems at major retailers and 3PL providers—supply chain management, order processing, customer service automation, and fulfillment operations. The 17% stock decline reflects temporary geopolitical risk, not fundamental weakness. Sellers should recognize this creates a 6-12 month opportunity window to negotiate favorable multi-year SaaS contracts for workflow automation, inventory management, and logistics optimization before enterprise IT budgets rebound and pricing normalizes.

Market Mispricing Signals Timing Window: Analyst assessment values ServiceNow at 23.90x 2026 earnings despite 19.35% expected EPS growth—attractive for enterprise customers seeking to lock in costs. The Middle East headwind is temporary; industry analysts view geopolitical impacts as short-term disruptions. Sellers managing 500+ SKUs across multiple channels should evaluate ServiceNow's Now Assist AI capabilities (customers spending $1M+ annually report significant automation ROI) during this pricing valley. The $210 million guidance raise despite headwinds demonstrates underlying business strength, suggesting the stock decline represents a buying opportunity for enterprise customers, not a warning signal.

Competitive Advantage Timing: Sellers who implement enterprise automation during this 6-12 month window gain 18-24 months of operational efficiency before competitors catch up. The 80% YoY growth in $5M+ contracts shows large enterprises are already moving; mid-market sellers (500-5000 SKU operations) represent the next wave. Delaying automation decisions until geopolitical normalization occurs risks paying 15-25% higher contract values when enterprise IT spending rebounds and ServiceNow's stock recovers to $150+ range.

Questions 7

How does ServiceNow's AI revenue growth (50% YoY to $1.5B) impact seller automation capabilities?

ServiceNow's Now Assist AI revenue reached $1.5 billion run rate, up 50% YoY and exceeding the original $1 billion 2026 target. Customers spending $1M+ annually report significant automation ROI through AI-powered workflow optimization, predictive inventory management, and intelligent order routing. For sellers, this means AI capabilities are moving from premium add-ons to standard platform features, improving ROI on automation investments. The 630 customers spending $1M+ annually demonstrate that enterprise-scale sellers (10K+ SKUs, multi-channel operations) achieve 25-40% operational cost reductions through AI-powered automation. Mid-market sellers implementing now gain early access to these capabilities before they become table-stakes requirements.

What is the timeline for enterprise IT spending recovery after geopolitical tensions ease?

Industry analysts view the Iran geopolitical impact as a temporary headwind, typically lasting 6-12 months before enterprise IT spending normalizes. ServiceNow's guidance raise despite headwinds suggests management expects recovery within this timeframe. Historical patterns show enterprise software spending rebounds 12-18 months after geopolitical disruptions ease, with pricing returning to pre-disruption levels or higher. Sellers who lock in contracts during the current 6-12 month pricing valley avoid the 15-25% price increases that typically follow market recovery. Monitor geopolitical developments and enterprise IT budget announcements (typically Q2-Q3 planning cycles) to time contract negotiations for maximum savings.