Iran Conflict Shipping Costs Surge $2-4/Barrel | E-Commerce Logistics Impact 2026

- Freight expenses spike 8-15% for cross-border sellers; 250K barrel/day US production increase expected by August 2026

Overview

The Iran geopolitical crisis is creating a critical bifurcation in global energy markets with direct implications for cross-border e-commerce logistics costs. A Dallas Federal Reserve survey (April 15-20, 2026) of 120 oil and gas firms reveals that 43 respondents expect U.S. crude production to rise by up to 250,000 barrels per day in 2026, yet this supply increase masks significant shipping cost volatility. Most critically, more than one-third of surveyed firms anticipate shipping costs will jump $2-4 per barrel following conflict resolution, translating to 8-15% freight cost increases for e-commerce sellers relying on ocean and air logistics.

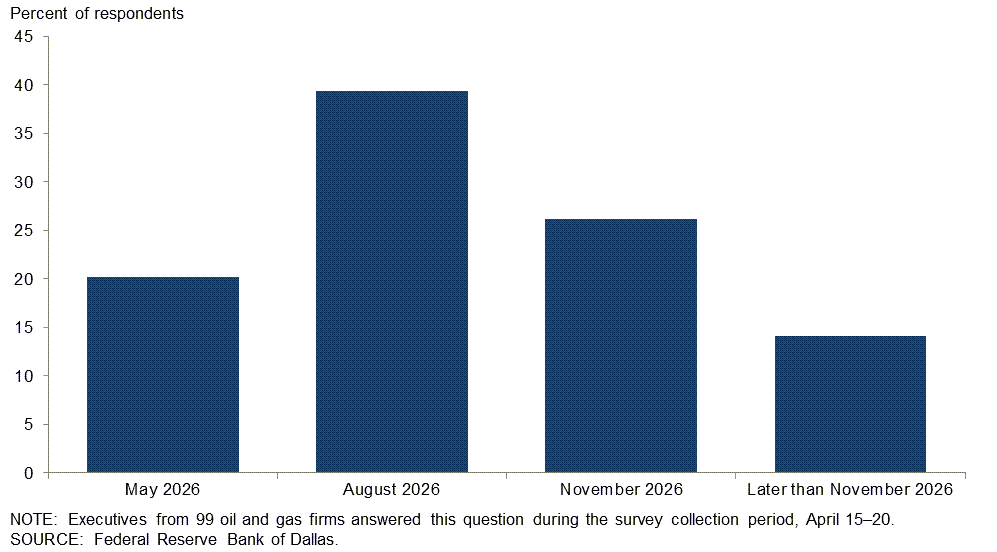

The market presents a paradoxical opportunity window. While shale producers resist output expansion due to Iran war uncertainty (per Financial Times reporting), executives simultaneously expect West Texas Intermediate crude to stabilize at $65/barrel once conflict resolves. This creates a timing arbitrage for sellers: those locking in shipping contracts NOW before the August-November Strait of Hormuz normalization window can avoid the anticipated $2-4/barrel post-conflict surge. The survey data shows 39 executives predict August normalization, with remaining respondents projecting November or later—establishing a 4-6 month window for logistics cost optimization.

For cross-border sellers, this translates to immediate operational decisions. Small to mid-sized sellers (shipping 500-2,000 units monthly) face margin compression of 3-8% if they delay freight procurement. A typical seller shipping 1,000 units monthly via ocean freight (averaging 20 containers) could see costs increase $4,000-8,000 monthly post-conflict. Conversely, sellers in price-sensitive categories (apparel, home goods, electronics accessories) operating on 15-25% margins face the highest risk. The survey indicates that larger independent operators are already "moving up drilling schedules" in response to $75+/barrel pricing, signaling industry recognition that current pricing windows are temporary.

The geopolitical uncertainty creates a strategic sourcing opportunity: sellers currently sourcing from China/Vietnam can negotiate extended payment terms with 3PL providers through August 2026, locking in current freight rates before the anticipated surge. Additionally, the survey's finding that "approximately two-thirds of respondents believe at least 90% of shut-in Gulf production will eventually return to market" suggests the price spike is temporary—making this an ideal period to build inventory ahead of the normalization window when shipping costs stabilize at higher levels.

Questions 8

When will shipping costs peak and stabilize for e-commerce sellers?

The survey data reveals a critical timing window: 39 of 120 surveyed executives predict Strait of Hormuz traffic normalization in August 2026, while remaining respondents project November or later. An oil executive quoted in the survey stated crude will 'fall back to the $65 a barrel level very quickly once this conflict settles down,' indicating the shipping cost surge is temporary and tied to conflict resolution. This creates a 4-6 month window (April-August/November 2026) where sellers should secure long-term freight contracts at current rates before the anticipated $2-4/barrel increase materializes post-normalization.

How much will shipping costs increase for cross-border sellers due to Iran conflict?

According to the Dallas Federal Reserve survey of 120 oil and gas firms (April 2026), more than one-third of respondents anticipate shipping costs will jump $2-4 per barrel following conflict resolution. For a typical cross-border seller shipping 1,000 units monthly via ocean freight (approximately 20 containers), this translates to $4,000-8,000 in additional monthly logistics costs. The survey indicates this surge will occur once the Strait of Hormuz normalizes, with 39 executives predicting August 2026 and others projecting November or later. Sellers should lock in freight contracts immediately to avoid these increases.