P&G Q3 2026 Earnings Beat | $1B Oil Cost Hit Reshapes CPG Supply Chain & Seller Pricing Strategy

- Oil prices surge $60→$100/barrel, triggering $1B annual profit hit; 172 companies issue cost warnings; beauty/baby care volume growth 3-5% signals premium pricing opportunity for cross-border sellers

Overview

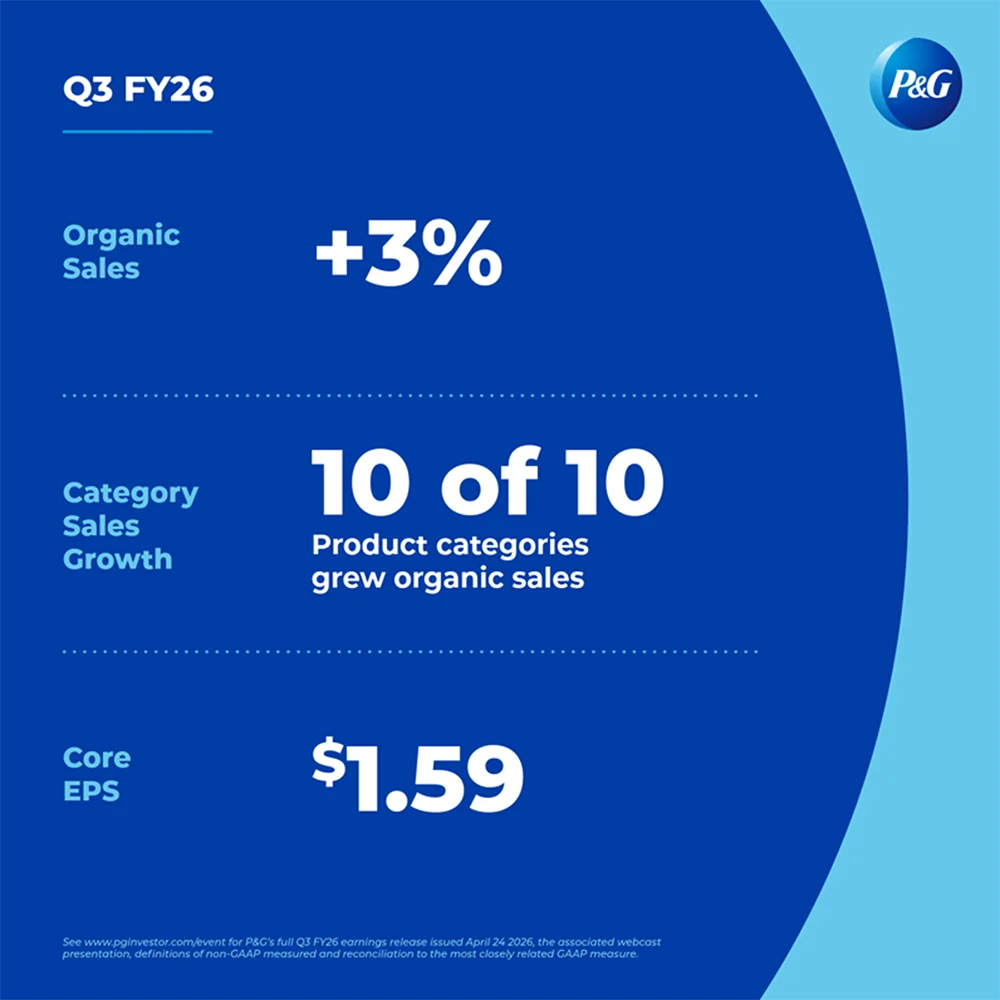

P&G's Q3 2026 earnings beat masks a critical supply chain crisis reshaping consumer packaged goods pricing and cross-border commerce dynamics. The company reported $21.24B revenue (+7% YoY) and beat EPS estimates ($1.59 vs $1.56 expected), but disclosed a devastating $1B post-tax profit hit for fiscal 2027 driven by oil prices surging from $60 to ~$100/barrel. This represents one of the largest cost impacts outside the airline industry, directly affecting packaging materials (plastics/paper), transportation, and logistics—the exact supply chain nodes that cross-border sellers depend on.

The financial pressure is immediate and quantifiable. P&G projects a $150M cost headwind in Q4 2026 alone from elevated fuel and transportation expenses. The company's total cost of goods sold reached $40.85B in 2025, demonstrating massive operational exposure. Critically, P&G's currency-neutral gross margin declined 100 basis points for the sixth consecutive quarter, pressured by tariffs and product innovation investments. Rather than broad price increases, P&G is pursuing selective premium product pricing to exploit the K-shaped economy—where affluent consumers maintain spending while budget-conscious shoppers face pressure. This bifurcated strategy has immediate implications for cross-border sellers sourcing P&G products or competing in beauty, baby care, and fabric care categories.

The broader market context amplifies seller opportunities and risks. Reuters analysis shows 172 companies have issued statements since the Iran conflict began: 24 withdrawing/cutting outlooks, 35 signaling price hikes, and 35 warning of financial impacts. Competitors including Nestlé and Beiersdorf have similarly flagged cost pressures. However, P&G's Q3 results reveal a critical insight: volume growth returned (+2% for first time in a year), with beauty division leading at +5% volume growth (personal care, skin care, hair care), baby/feminine/family care at +3% (diapers, paper products), and fabric/home care at +2% (Tide detergent). This volume recovery despite cost pressures indicates strong consumer demand for premium products—a direct opportunity for sellers to reposition inventory toward higher-margin, premium-positioned SKUs.

For cross-border sellers, this creates three distinct financial optimization opportunities: (1) Payment Cost Arbitrage: Sellers sourcing CPG products from Asia-Pacific suppliers can lock in lower procurement costs before Q4 2026 price increases propagate. Using regional payment corridors (Singapore/Hong Kong banking entities) for supplier payments can reduce FX conversion costs by 40-80 basis points versus direct USD transfers. (2) FX Hedging Window: With oil prices at $100/barrel and tariff uncertainty ($400M P&G headwind, $150M potentially recoverable), sellers should hedge USD/CNY and USD/INR exposure through 6-month forward contracts now, before Q2 2027 when tariff refunds may trigger currency volatility. (3) Working Capital Unlock: Sellers holding beauty/baby care inventory can accelerate cash conversion by 15-25 days through invoice financing or supply chain financing products targeting CPG categories, capitalizing on the demonstrated volume growth and premium pricing environment.

Questions 8

What are the tariff refund opportunities for sellers under IEEPA invalidation?

P&G expects $150M of its $400M tariff hit to be recoverable through refunds from invalidated tariffs under the International Emergency Economic Powers Act. Sellers importing CPG products should audit tariff classifications for potential IEEPA refund eligibility. Tariffs on beauty products (HS 3304-3307) and baby care (HS 3401-3402) may qualify if imposed under IEEPA authority. File refund claims with US Customs by Q2 2027 to capture 2-3% tariff cost recovery. This creates 60-90 day working capital improvement as refunds process. Consult customs brokers to identify eligible tariff lines and file claims proactively.

How should sellers adjust inventory strategy given 172 companies issuing cost warnings?

Reuters analysis shows 172 companies issued statements since Iran conflict: 24 cutting outlooks, 35 signaling price hikes, 35 warning of impacts. This signals industry-wide price increases starting Q2 2027. Sellers should front-load inventory purchases by Q1 2027 before price increases propagate. Beauty and baby care categories show strongest volume growth (+3-5%), justifying higher inventory allocation. Expect 3-8% wholesale price increases for CPG products by Q2 2027. Build 60-90 day inventory buffer in Q1 2027 to lock in current pricing, then reduce inventory velocity in Q2-Q3 2027 as prices increase. Monitor competitor pricing weekly to optimize repricing strategy.