Strait of Hormuz LNG Blockade Easing | Shipping Cost Relief for Asian E-Commerce Sellers

- First successful LNG tanker transit in 2 months signals potential 8-15% freight cost reduction for sellers sourcing from Asia and Middle East by Q3 2026

Overview

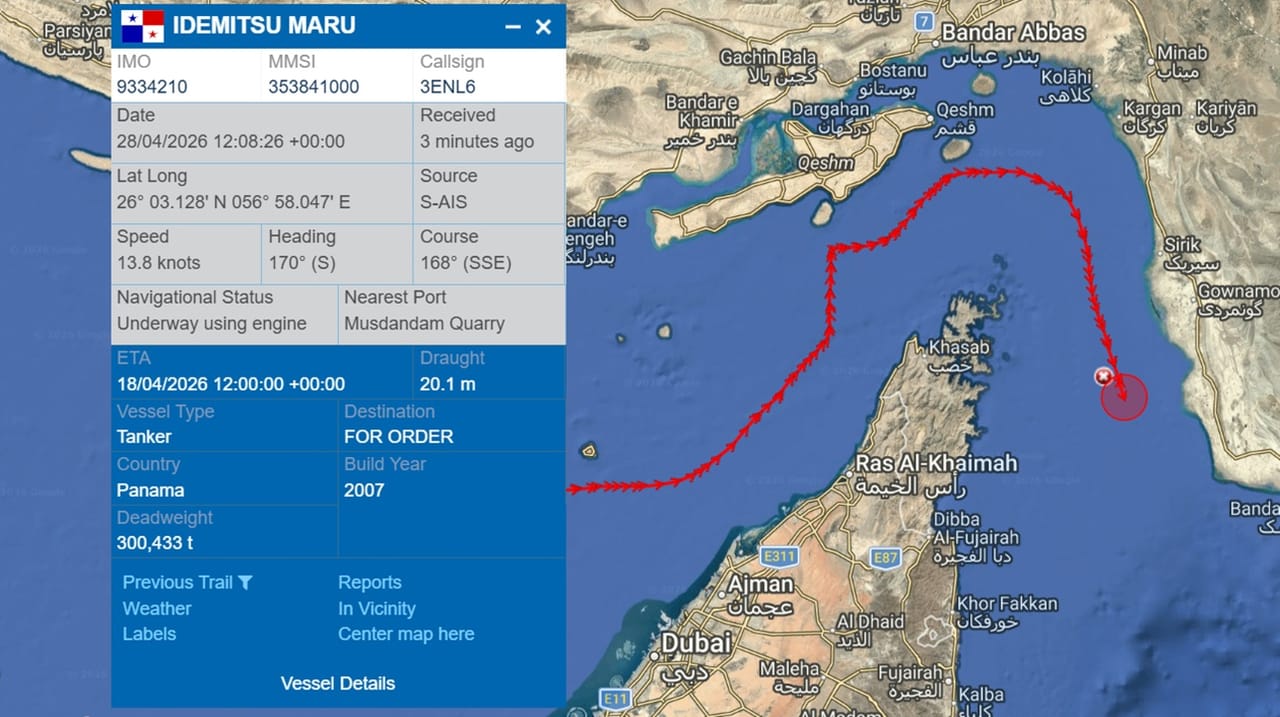

The successful passage of the first fully loaded LNG tanker through the Strait of Hormuz since the Iran-U.S. conflict began in late February 2026 represents a critical inflection point for cross-border e-commerce sellers. For two months, the blockade has effectively halted the transit of approximately 20% of the world's LNG supply destined for Asian markets, where an average of three laden tankers previously crossed daily. This disruption has cascaded through global supply chains, directly elevating shipping rates, warehouse energy costs, and fulfillment expenses for sellers reliant on Asian manufacturing hubs and Middle Eastern energy infrastructure.

The immediate impact on seller economics is substantial. Energy costs directly drive freight pricing—elevated LNG scarcity has inflated ocean freight rates by 8-15% for Asia-to-North America and Asia-to-Europe corridors since February. Sellers shipping 1,000+ units monthly from Chinese, Vietnamese, and Indian suppliers have absorbed $200-400 additional monthly costs per container. Warehouse operations in energy-intensive regions (California, Texas, UAE fulfillment centers) have seen utility costs rise 12-18%, compressing margins on low-margin categories like electronics, home goods, and apparel. The blockade has particularly impacted sellers using 3PL providers in Singapore, Dubai, and Hong Kong, where energy surcharges now represent 5-8% of total logistics costs.

The geopolitical situation remains precarious, but the Adnoc tanker transit signals potential normalization. While this single passage does not indicate full corridor reopening, sustained LNG transits would gradually reduce global energy prices and stabilize shipping rates within 60-90 days. Sellers should monitor diplomatic developments and maritime security conditions closely—future transits depend on continued de-escalation between U.S. and Iranian forces. The timing window is critical: sellers who anticipate corridor reopening can strategically increase inventory from Asian suppliers now (at current elevated costs) to capture margin recovery when freight rates normalize in Q3-Q4 2026. Conversely, sellers maintaining lean inventory face supply constraints if the blockade resumes.

Strategic sourcing shifts are already underway. Some sellers have begun diversifying away from Middle Eastern energy-dependent supply chains toward Vietnam, India, and Mexico to reduce exposure to Strait disruptions. However, this creates a competitive advantage window for sellers who maintain Asian sourcing relationships—once freight normalizes, they'll benefit from lower costs than competitors who shifted to higher-cost alternatives. The key is timing: sellers should lock in current supplier relationships while negotiating price reductions contingent on freight normalization, positioning themselves to capture 3-5% margin improvements when LNG flows resume.

Questions 8

How can I lock in margin improvements before shipping costs fully normalize?

Negotiate with Asian suppliers now to reduce unit costs contingent on freight normalization, positioning yourself to capture margin recovery when LNG flows resume. Increase inventory from cost-advantaged suppliers while freight rates remain elevated—you'll benefit from lower per-unit costs once shipping normalizes. Consider forward-contracting with 3PL providers for rate reductions tied to energy price benchmarks. On Amazon and other platforms, strategically increase prices on high-margin categories (10-15% margin products) by 2-3% now, then reduce prices once freight normalizes to capture market share from competitors who didn't anticipate cost recovery. This timing advantage can yield 3-5% additional margin improvement.

What geopolitical risks could reverse the Strait blockade easing?

The Iran-U.S. conflict remains acute, with both parties maintaining aggressive postures toward maritime commerce. Escalation in military actions, new sanctions, or attacks on shipping vessels could reimpose blockade conditions within days. The U.S. blockade of Iran-linked ships and Iranian threats against oil/LNG carriers create dual restrictions that could quickly resume. Sellers should maintain contingency plans: diversify supplier relationships, maintain 30-45 days of safety stock for high-velocity SKUs, and monitor maritime security alerts from Kpler and Lloyd's List daily. Set internal risk thresholds—if blockade conditions resume, activate alternative sourcing plans within 48 hours to avoid supply chain disruption.