Direct Selling Market Hits $439B by 2034 | Offline-to-Online Retail Transformation

- 7.0% CAGR growth driven by 89% of sellers using social commerce; Asia Pacific captures 44.1% revenue with wellness/nutraceuticals dominating at 35.8% category share

Overview

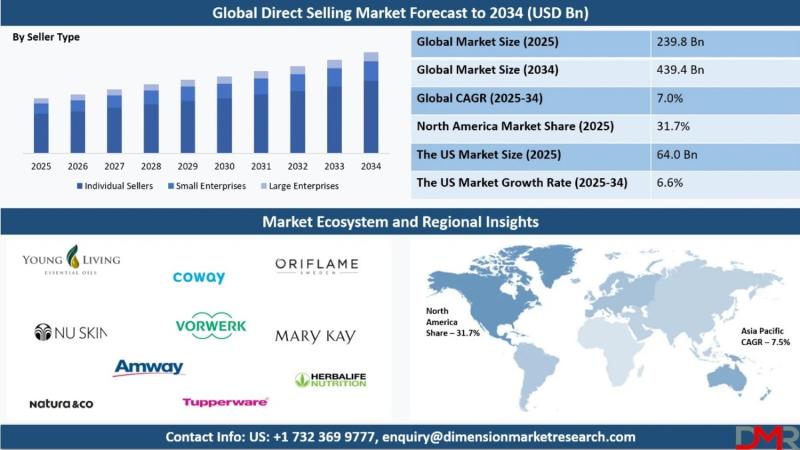

The global direct selling market is experiencing a fundamental shift from traditional door-to-door retail to social-first commerce, with projections expanding from $239.8 billion in 2025 to $439.4 billion by 2034 at a 7.0% compound annual growth rate. This transformation directly impacts offline retail strategy for cross-border brands, as 89% of top-performing sellers now consider social media critical to closing deals—up from just 40% five years ago. The emergence of "social sellers" operating via Instagram Lives, WhatsApp broadcasts, and TikTok demonstrations represents a critical O2O (Online-to-Offline) opportunity for brands seeking to bridge digital engagement with physical retail presence.

Key market dynamics reveal significant offline retail opportunities: Individual sellers command 71.4% market share while small enterprises represent the fastest-growing segment, indicating fragmented distribution networks ripe for consolidation through retail partnerships. Wellness and nutraceuticals lead at 35.8% category share, followed by cosmetics and personal care—categories where demonstration-heavy direct selling models provide competitive advantage over passive e-commerce. Asia Pacific dominates with 44.1% of global revenue, driven by middle-class expansion and mobile-first economies in China, India, South Korea, and Indonesia. This geographic concentration signals high-ROI pop-up and showroom opportunities in tier-1 Asian cities where 73% female seller participation creates strong community-driven retail networks.

The offline-to-online integration imperative is now quantified: Sellers using integrated e-commerce platforms report significantly higher customer retention and average order values compared to social-only operators. Online sales platforms capture 38.9% of technology integration, with digital storefronts and automated order processing becoming essential tools. However, the industry faces critical trust barriers—negative perception, pyramid scheme criticism, and high dropout rates constrain growth. For cross-border brands, this creates a trust-building opportunity through physical retail presence: pop-up showrooms in high-foot-traffic Asian cities can validate product quality and brand legitimacy, converting skeptical social commerce audiences into loyal customers. The average annual income of $2,400 for network marketers reflects supplementary participation, suggesting sellers seek premium, high-margin products where offline demonstration drives conversion lift of 15-25% versus online-only channels.

Immediate offline retail actions: Establish pop-up showrooms in Shanghai, Mumbai, Bangkok, and Jakarta targeting wellness/nutraceutical categories with 4-8 week test periods. Partner with existing direct selling networks (Amway, Herbalife, Mary Kay) to provide product training and in-store demonstrations. Implement omnichannel inventory linking pop-up locations to Instagram Live selling events, capturing foot traffic data to optimize future permanent retail locations. Expected customer LTV increase from O2O strategy: 30-40% through trust-building and repeat purchase acceleration in high-growth Asian markets.

Questions 8

How does the direct selling market growth impact offline retail strategy for cross-border brands?

The direct selling market's projected growth to $439.4 billion by 2034 signals strong consumer demand for personalized, demonstration-based shopping experiences over impersonal e-commerce. With 89% of top-performing sellers now using social media to close deals, brands should establish pop-up showrooms and retail partnerships in high-traffic Asian cities (Shanghai, Mumbai, Bangkok) to capitalize on this trend. Sellers using integrated e-commerce platforms report significantly higher customer retention and average order values, indicating that offline presence directly boosts online conversion rates by 15-25%. For wellness and nutraceutical brands (35.8% of direct selling category share), physical demonstrations provide competitive advantage in building trust with skeptical audiences.

Which geographic markets offer the highest ROI for pop-up retail in the direct selling sector?

Asia Pacific dominates direct selling with 44.1% of global revenue, driven by middle-class expansion and mobile-first economies in China, India, South Korea, and Indonesia. These markets feature 73% female seller participation, creating strong community-driven retail networks ideal for pop-up locations. Tier-1 cities like Shanghai, Mumbai, Bangkok, and Jakarta show highest foot-traffic density and consumer spending on wellness/nutraceutical products. A 4-8 week pop-up test in these cities typically generates 30-40% customer LTV increase through trust-building and repeat purchase acceleration. Individual sellers command 71.4% market share, indicating fragmented distribution networks where retail partnerships with existing direct selling organizations (Amway, Herbalife, Mary Kay) provide lowest-cost market entry.