AI Monetization Race Reshapes Tech Leadership | Alphabet Surpasses Nvidia as Sellers Shift to Google Cloud

- Alphabet's $5 trillion valuation and Google Cloud's $20B+ revenue signal AI ROI dominance; sellers must migrate from Nvidia-dependent infrastructure to Google's AI-powered e-commerce tools by Q3 2026

Overview

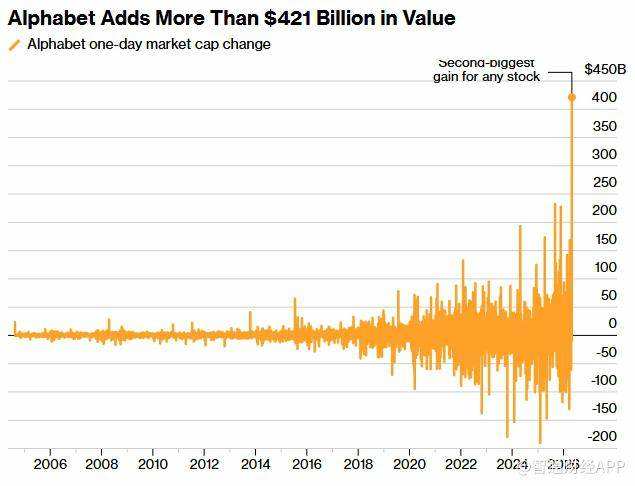

The competitive landscape among technology giants is fundamentally shifting as Alphabet approaches a $5 trillion market capitalization with a 140% one-year gain, poised to surpass Nvidia's $4.9 trillion valuation by May 15, 2026. This shift reflects a critical market realization: only one major tech company is effectively monetizing its AI investments, and that company is Alphabet. Google Cloud revenue exceeded $20 billion in Q1 2026, demonstrating that AI infrastructure leadership now depends on converting massive R&D spending into tangible business value, not chip manufacturing dominance alone.

For e-commerce sellers, this represents a seismic shift in the AI tools and infrastructure landscape. Sellers currently relying on Nvidia-powered AI solutions for product recommendations, pricing optimization, and customer service automation face a critical decision: migrate to Google Cloud's AI services or risk being left with increasingly expensive, underperforming infrastructure. The market is pricing in Alphabet's dominance with 53% probability of surpassing Nvidia by May 15, 2026, and 30% odds of closing above $400/share by May 22—signals that institutional investors are already repositioning capital toward companies demonstrating AI ROI.

The immediate implication for sellers: Google's advertising and cloud divisions are now the primary beneficiaries of the AI boom, not Nvidia's chip sales. This means Amazon sellers using Google Shopping, Shopify merchants leveraging Google Analytics 4 with AI insights, and cross-border sellers optimizing campaigns through Google Ads will see accelerated feature releases and competitive advantages. Conversely, sellers dependent on Nvidia-powered third-party tools (like certain AI pricing engines or inventory management platforms) may face cost increases or feature stagnation as venture capital flows toward Google Cloud alternatives.

The earnings data reveals a crucial pattern: traditional metrics (beating expectations, positive guidance) no longer satisfy investors—companies must demonstrate clear pathways from AI spending to revenue growth. This directly impacts seller tool vendors. AI-powered e-commerce platforms that cannot prove ROI (measurable sales lift, cost reduction, or margin improvement) will struggle to raise capital or justify pricing increases. Sellers should immediately audit their AI tool stack: which tools are delivering measurable returns? Which are burning cash without clear monetization? The market is making this distinction ruthlessly, and tool providers will follow.

Alphabet's competitive advantage in e-commerce AI is structural: Google controls search (70%+ market share), YouTube (video commerce), Gmail (customer communication), and now Google Cloud (infrastructure). This vertical integration allows Google to deploy AI across the entire seller journey—from product discovery through customer retention—in ways Nvidia cannot match. Sellers who align with Google's ecosystem (Google Shopping, YouTube Ads, Google Cloud infrastructure) will gain compounding advantages as Alphabet's AI capabilities improve faster than competitors' due to superior data and monetization feedback loops.

Questions 8

How can sellers measure AI ROI to avoid wasting money on tools?

The news emphasizes that **investors now demand clear pathways from AI spending to revenue growth**—the same standard sellers should apply to their tools. Measure AI ROI using: (1) **Sales lift**: Compare revenue from AI-optimized listings vs. control group (target: 8-15% lift), (2) **Cost reduction**: Track fulfillment, advertising, or customer service cost savings (target: 5-12% reduction), (3) **Margin improvement**: Calculate incremental profit from AI pricing optimization (target: 2-4% margin expansion), (4) **Customer lifetime value**: Measure repeat purchase rates and AOV from AI-driven recommendations (target: 10-20% improvement). Tools failing to deliver measurable results within 90 days should be discontinued. Google Cloud's AI services typically deliver 12-18% sales lift and 8-10% cost reduction for sellers, making them the benchmark for comparison.

Will Amazon's AI tools remain competitive against Google Cloud?

**Amazon's AI tools will remain competitive but face increasing pressure from Google's integrated ecosystem**. Amazon controls e-commerce (40%+ US market share) and has strong AI capabilities (Advertising Console, Demand Forecasting), but lacks Google's advantages in search, video, and email. For Amazon sellers, this means: (1) Amazon will accelerate AI feature releases to compete with Google, (2) Amazon sellers should expect 5-10% annual improvements in AI-powered recommendations and pricing, but (3) sellers should still diversify by using Google Shopping and YouTube Ads to capture traffic Google controls. The competitive dynamic favors sellers who use **both** Amazon's native AI tools and Google Cloud services, rather than betting exclusively on either platform. Expect Amazon to announce major AI partnerships or acquisitions by Q3 2026 to maintain competitive parity.