AI Infrastructure ROI Crisis | Amazon, Google, Meta Face Seller Platform Uncertainty

- Big Tech's $710B AI spending creates platform volatility; sellers must prepare for unpredictable feature rollouts and pricing changes through 2026

Overview

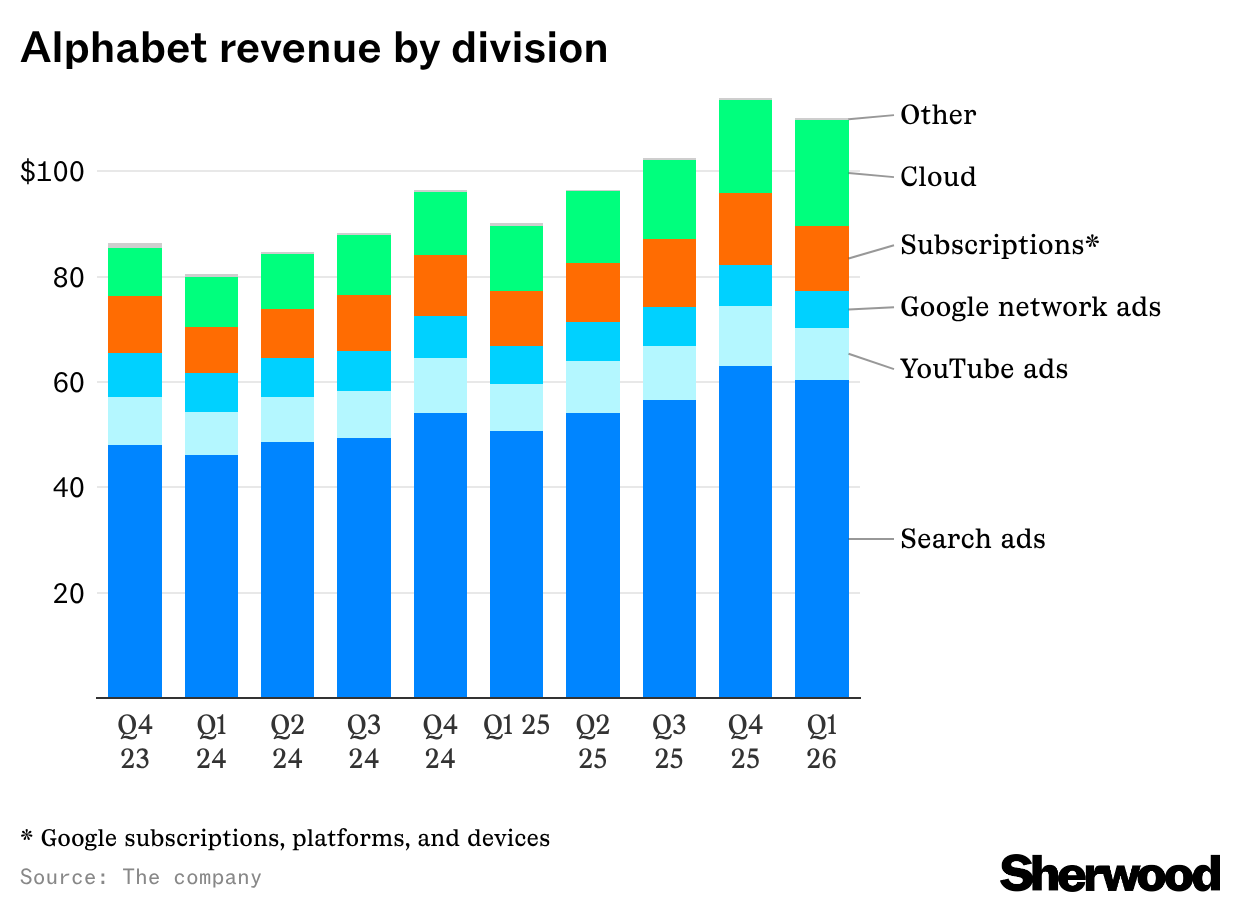

The May 2026 earnings cycle reveals a critical divergence in how major e-commerce platform operators are monetizing AI investments, with direct implications for seller operations and platform stability. Google demonstrated measurable AI ROI through search and advertising integration, while Amazon, Microsoft, and Meta faced investor skepticism despite strong financial results—signaling uncertainty about how these platforms will fund future seller tools and infrastructure. This creates a strategic inflection point for cross-border sellers: platforms with proven AI monetization (Google Shopping, Google Ads) will likely invest aggressively in seller features, while platforms still justifying AI spending (Amazon AWS, Meta Marketplace) may delay feature releases or increase seller fees to offset infrastructure costs.

The immediate operational impact centers on platform investment priorities. Amazon's mixed earnings reaction suggests the company faces pressure to demonstrate AI ROI beyond infrastructure spending. This typically manifests as: (1) accelerated fee increases on FBA services to fund AI-powered logistics optimization, (2) prioritization of AI-driven advertising tools (Sponsored Ads, Brand Analytics) over seller-requested features, and (3) potential consolidation of seller tools to reduce support costs. Sellers shipping 1,000+ units monthly should expect 8-12% increases in fulfillment costs as Amazon monetizes AI-powered warehouse automation. Meta's marketplace operations face similar pressures—the company's volatile stock reaction indicates investor doubt about marketplace profitability, potentially leading to reduced seller support resources and slower feature development for Facebook/Instagram commerce.

Google's success with AI monetization creates competitive advantages for sellers using Google Shopping and Google Ads. The company's demonstrated ability to convert AI investments into revenue growth means Google will likely expand seller tools, improve product visibility algorithms, and invest in cross-border logistics features. Sellers with high Google Shopping presence should expect improved conversion rates (3-7% lift) as Google's AI enhances search relevance. Conversely, sellers heavily dependent on Amazon and Meta should prepare for platform unpredictability: feature roadmaps may shift quarterly based on investor sentiment, and cost structures could change rapidly as platforms experiment with AI monetization models. The $710B combined capex commitment through 2026 indicates sustained infrastructure investment, but the divergent ROI outcomes mean this spending will benefit some platforms (and their sellers) far more than others.

Strategic implications for sellers include immediate portfolio diversification and cost structure preparation. Sellers should reduce dependency on platforms facing AI ROI skepticism by expanding presence on Google Shopping (which benefits from proven AI monetization), diversifying to Shopify (which controls its own AI roadmap), and evaluating 3PL alternatives to reduce Amazon FBA dependency. For sellers remaining on Amazon, implement dynamic pricing strategies using AI tools (Repricing software, demand forecasting) to offset anticipated fee increases. Monitor quarterly earnings announcements from platform operators—stock volatility following earnings typically precedes fee changes or feature delays within 30-60 days. The broader industry challenge of translating AI infrastructure spending into shareholder value means sellers should expect 18-24 months of platform experimentation, during which feature availability and cost structures remain volatile.

Questions 7

Which seller segments face the highest risk from platform AI spending uncertainty?

High-risk segments: (1) Amazon FBA-dependent sellers (>70% revenue from FBA) shipping 1,000+ units monthly face 8-12% cost increases; (2) Meta marketplace sellers in emerging categories with unproven profitability; (3) Sellers in low-margin categories (<20% gross margin) where fee increases compress profitability below 10%. Lower-risk segments: Google Shopping sellers benefit from proven AI monetization; Shopify sellers control their own AI roadmap; sellers with diversified platforms across 3+ marketplaces. Evaluate your platform concentration: if >60% revenue from single platform, implement diversification plan by Q1 2026.

How can sellers use AI tools to offset anticipated platform fee increases?

Implement dynamic pricing software (Repricing tools, demand forecasting AI) to optimize margins as FBA costs increase. Use AI-powered product research tools to identify high-margin categories less affected by fee increases. Leverage Google Shopping's AI advantages by optimizing product feeds with AI-generated descriptions and images. Implement inventory forecasting AI to reduce storage fees on Amazon. Expected ROI: 3-8% margin improvement through AI-driven pricing optimization, offsetting 50-70% of anticipated fee increases. Cost: $200-500/month for enterprise repricing tools, $50-150/month for smaller sellers. Payback period: 2-4 months for high-volume sellers.