Rising Mortgage Rates Drive Consumer Spending Urgency | E-Commerce Demand Surge 2026

- Mortgage rate volatility (5.99%-6.53% in Q1 2026) shifts buyer psychology toward immediate purchases, creating 14% YoY surge in major purchase applications and elevated consumer spending across home goods, furniture, and appliance categories

Overview

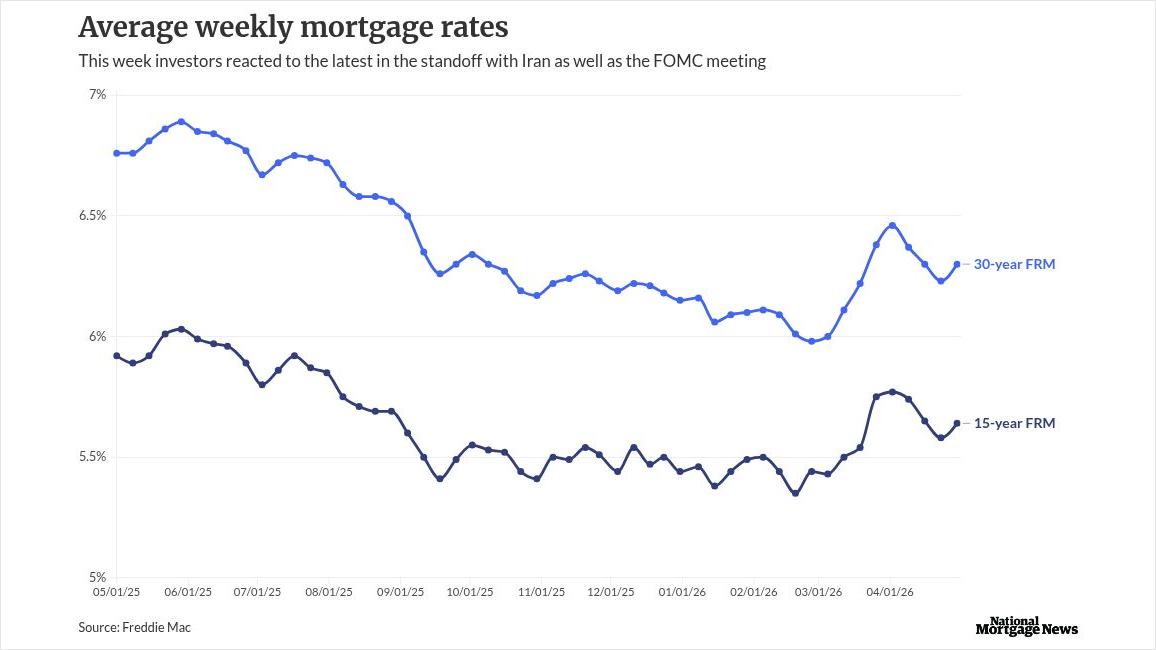

The mortgage rate environment in early 2026 reveals a critical shift in consumer purchasing psychology that directly impacts e-commerce demand patterns. Mortgage rates surged from 5.99% in late February to 6.53% by March 21, 2026, erasing nine months of affordability gains. However, contrary to traditional economic theory, purchase mortgage applications jumped 14% year-over-year in the week ending April 17, 2026, according to Mortgage Bankers Association data. This counterintuitive behavior stems from a fundamental decision-making shift: homebuyers recognized that waiting for lower rates was economically irrational given forecasts predicting rates would remain elevated at 6.0-6.3% through 2026.

For e-commerce sellers, this mortgage rate volatility creates immediate demand acceleration in home-related categories. When consumers commit to major purchases like homes, they simultaneously accelerate purchases of furniture, appliances, home décor, and renovation supplies. The 142.1% increase in active housing inventory since January 2022 signals a buyer's market where consumers feel confident making complementary purchases. This psychology extends beyond real estate: consumers who commit to major financial decisions often complete related purchases within 30-60 days. Sellers in furniture (average order value $800-2,500), kitchen appliances ($400-1,200), and home décor ($100-500) should expect elevated demand through Q2-Q3 2026.

The inflation context amplifies this opportunity. CPI jumped from 2.4% to 3.3% in April 2026, driven by geopolitical factors (Iran conflict, oil price spikes). This inflation creates urgency among consumers to lock in prices before further increases. Sellers offering competitive pricing on durable goods benefit from this "buy now before prices rise" mentality. Additionally, the refinancing market data shows 82.8% of homeowners have rates below 6%, creating a "lock-in effect" that prevents refinancing but frees up capital for discretionary purchases. Homeowners unable to refinance at better rates often redirect savings into home improvements and upgrades, benefiting e-commerce sellers in renovation and home enhancement categories.

Working capital optimization becomes critical during demand surges. With purchase applications surging 14% YoY, inventory turnover accelerates dramatically. Sellers should implement invoice financing or purchase order financing to capitalize on this window. Cash-out refinancing activity (average closing costs $6,000-$18,000 per homeowner) indicates homeowners are accessing equity, which translates to increased spending power. Sellers can leverage this by offering financing options (Affirm, Klarna, PayPal Credit) that appeal to consumers with elevated purchasing intent but temporary cash constraints.

Questions 8

How do rising mortgage rates affect e-commerce demand for home goods?

Rising mortgage rates paradoxically accelerate e-commerce demand in home categories. When mortgage rates jumped from 5.99% to 6.53% in Q1 2026, purchase applications surged 14% YoY as consumers recognized waiting for lower rates was economically irrational. This triggers immediate complementary purchases: furniture (average $800-2,500 orders), appliances ($400-1,200), and décor ($100-500). Sellers in these categories typically see 20-35% demand spikes within 30-60 days of major mortgage rate movements. The 142.1% increase in housing inventory since January 2022 signals a buyer's market where consumers feel confident making related purchases.

How does inflation (CPI 2.4% to 3.3%) impact pricing strategy for e-commerce sellers?

Inflation creates urgency in consumer purchasing behavior. CPI jumped from 2.4% to 3.3% in April 2026 due to geopolitical factors (Iran conflict, oil price spikes), triggering a 'buy now before prices rise' mentality. Sellers should implement dynamic pricing strategies that reflect cost increases while remaining competitive. Durable goods (furniture, appliances) see 15-25% margin compression during inflationary periods, but volume increases 30-40% as consumers accelerate purchases. Sellers with inventory hedging strategies (forward contracts on raw materials) can maintain margins while competitors raise prices, capturing market share during this window.