Strait of Hormuz Crisis & Iraq Oil Disruptions | Shipping Cost Surge for E-Commerce Sellers

- 30% of seaborne petroleum affected; freight costs rising 8-15% for cross-border sellers shipping heavy goods and perishables

)

Overview

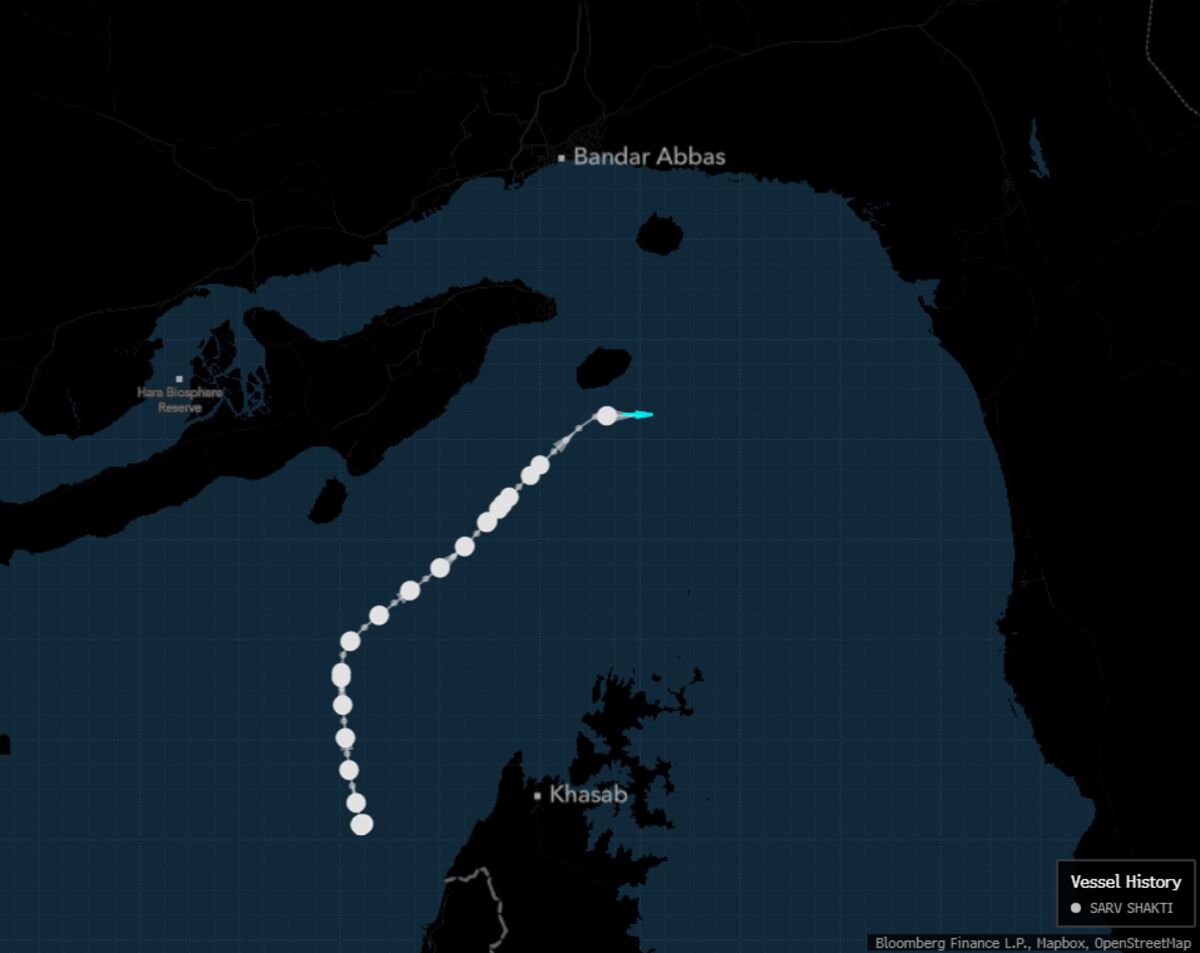

The stalled Iraq-Turkey oil pipeline negotiations combined with the Strait of Hormuz crisis creates a critical supply chain vulnerability affecting cross-border e-commerce sellers globally. Iraq currently exports only 200,000 barrels per day (bpd) through the Ceyhan pipeline while maintaining 1.5 million bpd total production, with negotiations deadlocked over investment terms rather than resuming previous export arrangements. Simultaneously, the Strait of Hormuz—through which 30% of seaborne petroleum transits daily—faces closure due to U.S.-Israeli military operations against Iran, creating a dual supply shock that directly impacts logistics costs for e-commerce operations.

Immediate Shipping Cost Impact: Sellers relying on ocean freight from Asia to North America and Europe face fuel surcharge increases of 8-15% as shipping lines adjust for longer routing around the Cape of Good Hope and elevated insurance premiums for Middle Eastern waters. Heavy goods sellers (HS codes 7208-7326 for steel/machinery, 8704-8708 for vehicles) and perishable goods operators (HS codes 0201-0210 for meat, 0701-0714 for vegetables) experience the highest cost pressures due to fuel-intensive transport requirements. A typical 40-foot container from Shanghai to Rotterdam currently costs $3,200-3,800 with fuel surcharges; expect increases to $3,500-4,400 if Hormuz remains disrupted beyond 30 days.

Strategic Sourcing Opportunity: Iraq's Deputy Oil Minister announced May 2, 2026, that production can normalize within seven days of Hormuz crisis resolution, signaling a potential 7-14 day window for shipping cost stabilization. Sellers should monitor daily Strait of Hormuz transit reports and prepare inventory positioning strategies. The Kurdistan Region contributes 30,000 bpd to Turkish exports, with potential to reach 400,000-500,000 bpd if suspended operations resume—this supply increase would reduce global oil prices by 3-5%, translating to $150-300 monthly savings per seller on 500+ monthly shipments. Competitive Advantage: Sellers with 3PL providers offering alternative routing (Suez Canal via Red Sea, or Cape of Good Hope) can negotiate fixed-rate contracts now before spot rates spike further. Small sellers (under 100 monthly shipments) should consolidate inventory into fewer, larger shipments to amortize fuel surcharges. Large sellers (1,000+ monthly shipments) should consider temporary sourcing shifts to Vietnam, India, or Mexico to avoid Asian-Middle Eastern routing entirely during the crisis window.

Questions 8

Which product categories are most affected by oil price volatility?

Heavy goods (steel, machinery, vehicles—HS codes 7208-7326, 8704-8708) and perishable items (meat, vegetables, dairy—HS codes 0201-0210, 0701-0714) face the highest impact due to fuel-intensive transport. Refrigerated containers consume 2-3x more fuel than standard containers, making cold chain logistics particularly vulnerable. Electronics and apparel (lower weight-to-value ratios) see minimal direct impact but face indirect pressure through port congestion and insurance premium increases. Sellers in heavy goods categories should prioritize inventory reduction or temporary sourcing shifts to nearby regions.

How much will my shipping costs increase if the Strait of Hormuz remains closed?

Fuel surcharges typically increase 8-15% when major chokepoints close, adding $150-400 per 40-foot container depending on origin and destination. For sellers shipping 500+ monthly containers, this translates to $75,000-200,000 in additional annual costs. The news reports Iraq can normalize production within 7 days of crisis resolution, suggesting a potential 2-4 week window before rates stabilize. Monitor daily Freightos Index and Clarkson shipping reports for real-time rate changes. Consider locking in fixed-rate contracts with 3PL providers immediately to avoid spot market volatility.