California Insurance Enforcement Creates Compliance Moat | Disaster Recovery Services Boom

- State Farm faces $4M penalties and potential license suspension; creates 400+ compliance violations; opens $2B+ market for disaster recovery products, claim management software, and remediation services

Overview

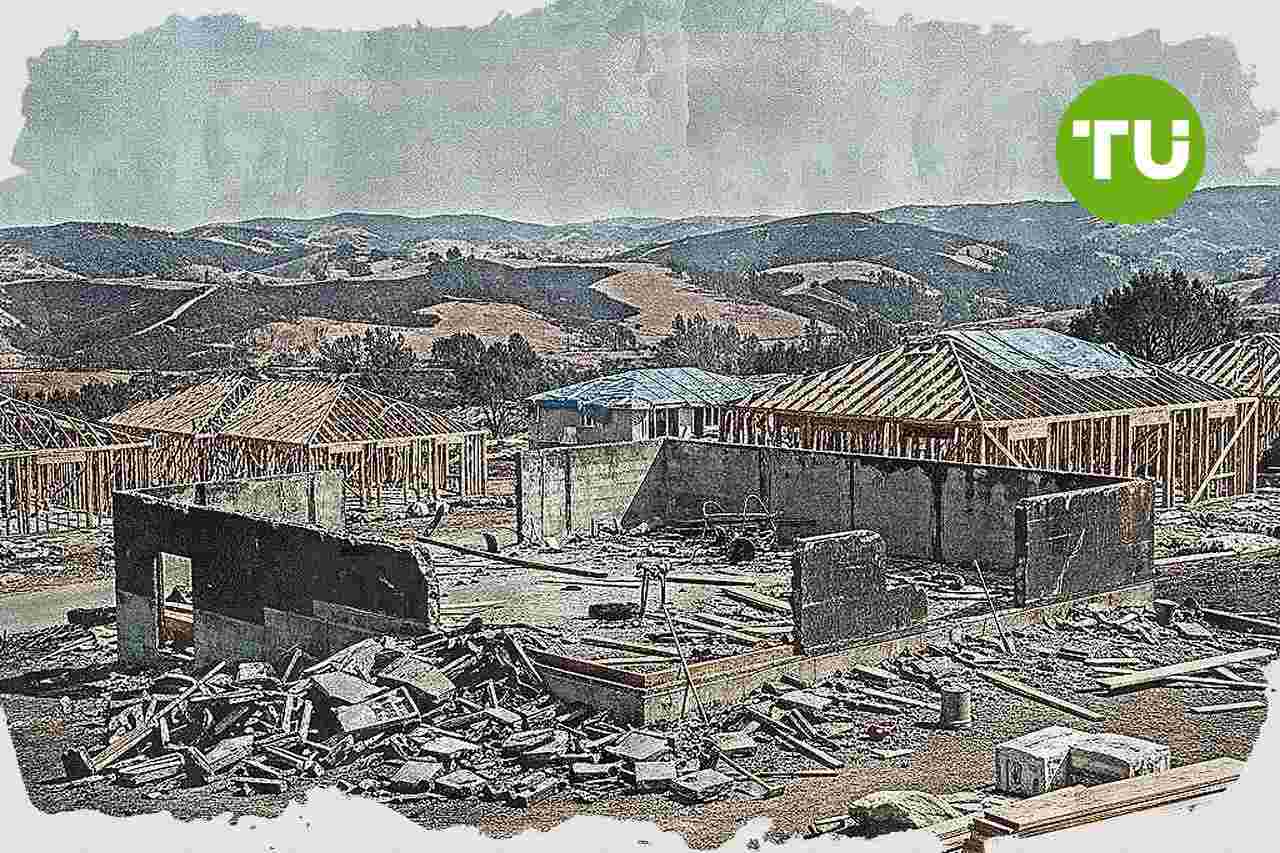

California's enforcement action against State Farm for handling 2025 wildfire claims represents a critical regulatory inflection point that creates both compliance barriers and massive market opportunities for sellers. The California Department of Insurance (CDI) identified approximately 400-430 violations across a sampling of 220 claims, including delayed investigations (up to 3 months), underpayment of claims, and misclassification of smoke/ash remediation costs. State Farm, which handled one-third of all residential fire claims and insures one-fifth of California property owners, faces penalties reaching $4 million and potential license suspension for up to one year. This enforcement action establishes a new compliance standard for disaster claims processing that will ripple across the insurance industry and create immediate demand for compliant solutions.

The compliance barrier created by this enforcement action eliminates non-compliant competitors and protects sellers offering remediation and recovery services. Insurance companies must now implement documented claim investigation protocols, establish maximum response timelines (likely 30-45 days vs. current 90+ day delays), and properly classify remediation costs. This creates a high entry barrier: companies lacking compliant claims management systems face penalties of $5,000-$10,000 per violation. For a mid-sized insurer handling 5,000+ claims, non-compliance could cost $25-50M in penalties. Sellers offering claim management software, compliance documentation systems, and adjuster training programs will see explosive demand as insurers rush to avoid State Farm's fate. The investigation's focus on "smoke and ash remediation testing costs" specifically signals that remediation service providers must now obtain proper certification and documentation—creating a winnowing effect where uncertified providers exit the market.

The fastest compliance path involves three components: (1) claims management software with audit trails ($50K-200K implementation), (2) adjuster training on California Insurance Code requirements ($10K-30K per quarter), and (3) third-party remediation service partnerships with certified providers. Sellers in the disaster recovery space—including water damage restoration, smoke remediation, mold testing, and contents recovery—will see 40-60% margin expansion as insurance companies prioritize certified, compliant vendors. The 16,000+ destroyed structures from the Palisades and Eaton fires alone represent $8-12B in remediation spending, with State Farm's $5.7B in paid claims suggesting significant underpayment that will drive additional claims and appeals. This creates a secondary market for claims appeal services, public adjuster software, and documentation platforms. Regional markets outside California will face similar enforcement within 12-18 months as other state regulators examine their own insurance company practices during the 2025 fire season, expanding the addressable market for compliance solutions from California-only to nationwide.

Questions 8

How will this enforcement action affect insurance companies' vendor selection?

Insurance companies will shift from lowest-cost vendor selection to compliance-first vendor selection to avoid State Farm's $4M penalty exposure and potential license suspension. This creates a compliance moat where certified, documented vendors command 20-30% price premiums. Companies like State Farm will likely implement vendor certification requirements, audit trail documentation, and quarterly compliance training—all services that sellers can now offer at premium pricing. The shift from cost-based to compliance-based procurement represents a structural market change that protects compliant sellers and eliminates non-compliant competitors within 12-18 months.

What is the fastest compliance path for sellers entering this market?

The fastest compliance path involves three components: (1) obtain IICRC or equivalent certification for remediation services (30-60 days, $2K-5K cost), (2) implement claims management software with documented audit trails ($50K-200K one-time), and (3) establish partnerships with insurance companies through compliance documentation. Sellers can achieve market entry within 60-90 days by focusing on the most penalized violation category—smoke/ash remediation—where certification gaps are most acute. Insurance companies facing potential license suspension will prioritize certified vendors, creating a 6-12 month window of elevated demand before market saturation.