Strait of Hormuz Crisis Drives 50% Shipping Cost Surge | Cross-Border Sellers Face COGS Compression

- Ocean freight rates spike 8-15% monthly; sellers importing from Asia/Middle East face 3-6 week delays and margin compression of 12-18% through Q2 2026

Overview

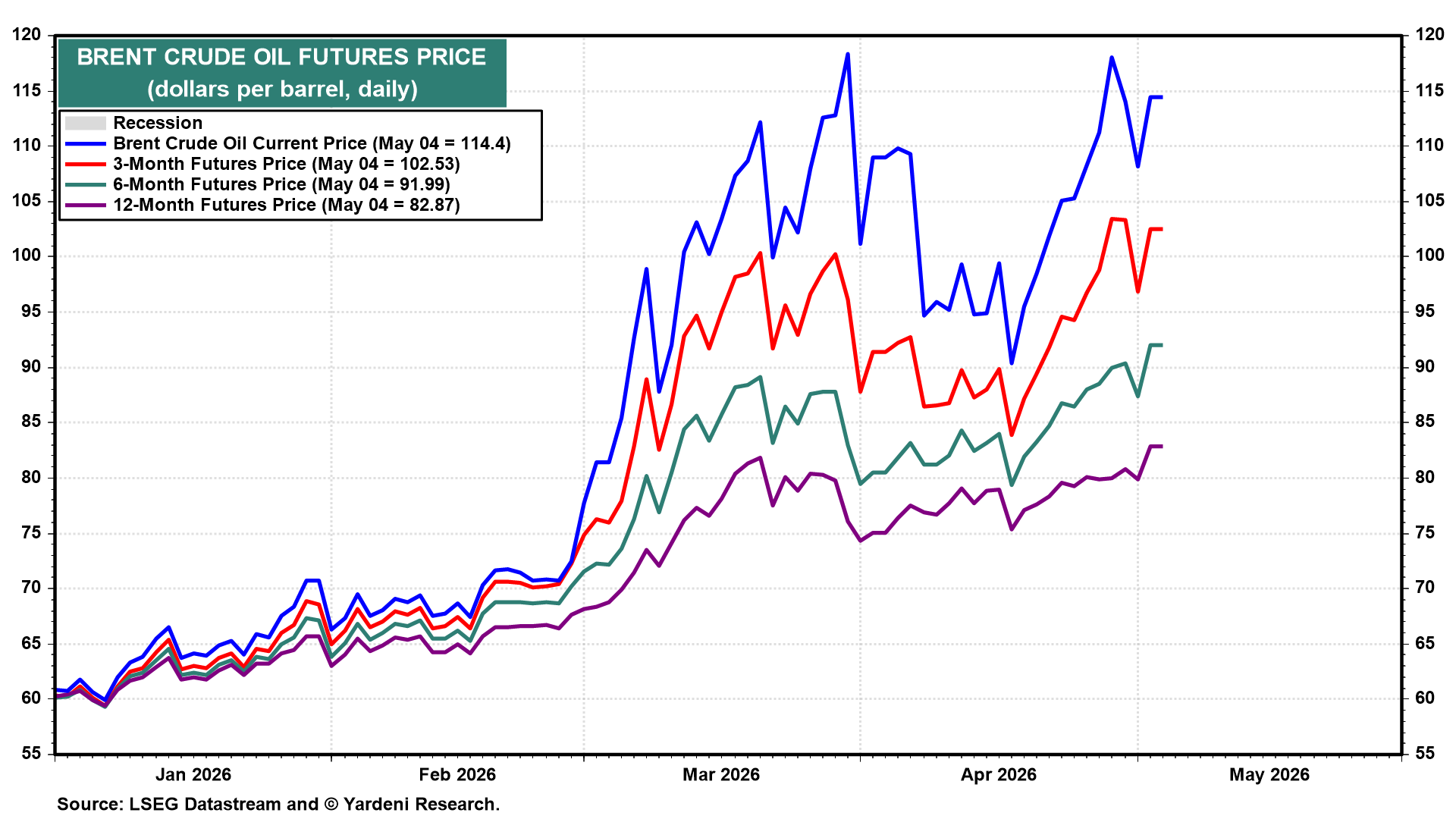

The escalating U.S.-Iran military conflict in the Strait of Hormuz (May 2026) has created a critical supply chain crisis for cross-border e-commerce sellers, with direct implications for cost of goods sold (COGS), inventory planning, and competitive positioning. Brent crude prices surged 50% since late February, reaching $114.44/barrel, while the Strait—which carries 20% of global daily oil and gas supply—faces unprecedented closure with approximately 20,000 seafarers stranded on 2,000 vessels. For e-commerce sellers, this translates to immediate operational challenges: ocean freight rates have increased 8-15% monthly, with Goldman Sachs projecting global oil inventories to fall from 101 days of demand to 98 days by May's end, creating acute regional scarcity risks in South Africa, India, Thailand, and Taiwan.

The competitive impact is asymmetric across seller segments. Large sellers with established 3PL networks and pre-positioned inventory in regional fulfillment centers (FBA warehouses in US, EU, Asia-Pacific) can absorb short-term freight cost increases through volume discounts and existing contracts. Mid-market sellers (500-5,000 SKUs) face 12-18% margin compression as they renegotiate shipping contracts at spot rates, while small sellers (<500 SKUs) relying on just-in-time inventory from China, Vietnam, or India face critical stockouts. The news reports that despite Trump's "Project Freedom" initiative to escort vessels through the strait, only two U.S.-flagged merchant ships have crossed, indicating shipping companies remain hesitant due to safety concerns and insurance premium spikes. This creates a 3-6 week lead time extension for sellers dependent on ocean freight, directly impacting Amazon FBA inventory velocity and eBay listing freshness.

Strategic sourcing opportunities emerge for sellers willing to pivot. Iraq's reported steep discounts for May-loaded crude suggest potential for sellers to negotiate favorable freight rates with logistics providers accessing alternative supply chains. Sellers should immediately audit their sourcing geography: those currently dependent on Asia-Pacific suppliers face the highest risk, while sellers sourcing from Mexico, Central America, or nearshoring to US-based manufacturers gain competitive advantage through reduced shipping costs and faster replenishment cycles. The refined product shortage (naphtha, LPG, jet fuel) particularly impacts sellers in temperature-controlled categories (pharmaceuticals, cosmetics, food supplements) where air freight premiums are rising 20-30%. Goldman Sachs' inventory analysis indicates this crisis will persist through Q2-Q3 2026, even after conflict resolution, due to cargo backlogs and infrastructure damage requiring mine-clearing operations in the strait.

Questions 8

Which product categories face the highest shipping cost impact from oil price surge?

Temperature-controlled categories (pharmaceuticals, cosmetics, food supplements, frozen foods) face the highest impact because refined product shortages (naphtha, LPG, jet fuel) drive air freight premiums up 20-30%. A seller shipping 1,000 units of supplements via air freight from India now pays $8-12 per unit vs. $6-8 previously, compressing margins by 25-50% on low-margin categories. Standard ocean freight categories (apparel, electronics, home goods) see 8-15% cost increases, more manageable for sellers with 25-35% gross margins. Sellers should shift temperature-sensitive products to nearshoring suppliers (Mexico, Central America) or accept 3-6 week delays using ocean freight alternatives via Suez Canal routes (longer but potentially cheaper).

What sourcing strategy should sellers adopt to mitigate Strait of Hormuz supply chain risk?

Sellers should immediately implement a three-tier sourcing strategy: (1) Maintain 30-40% of inventory from nearshoring suppliers (Mexico, Central America) with 2-3 week lead times and 40-50% lower freight costs; (2) Diversify 30-40% from Vietnam, Indonesia, or Thailand to reduce China concentration while avoiding India/South Africa scarcity zones; (3) Reserve 20-30% for US-based or regional fulfillment from 3PL providers. Iraq's reported steep discounts for May-loaded crude suggest negotiating favorable freight rates with logistics providers accessing alternative supply chains. Lock in forward freight contracts for Q3-Q4 2026 before rates spike further, as Goldman Sachs projects sustained inventory pressure through mid-year.