Energy Crisis Reshapes US Consumer Spending | Discretionary Categories Face 2-3% Demand Destruction

- April 2026 retail sales +0.5% masks underlying weakness in furniture (-2%), apparel (-1.5%), and appliances (-7.4%); energy prices trigger May-June demand cliff for e-commerce sellers

Overview

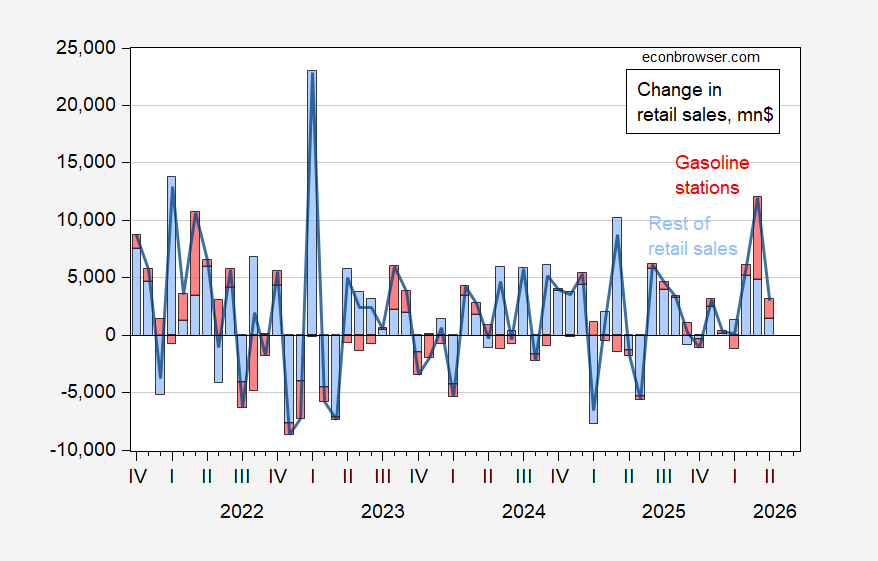

The April 2026 retail sales report reveals a critical inflection point for cross-border e-commerce sellers: while headline growth of 0.5% suggests consumer resilience, underlying data exposes severe demand destruction in discretionary categories driven by elevated energy costs from the Iran conflict. The Commerce Department's May 14, 2026 report shows furniture sales collapsed 2%, clothing declined 1.5%, and department stores fell 3.2%—the most concerning signal being appliance manufacturer Whirlpool's disclosure that industry demand reached "recession-level lows" with a 7.4% contraction comparable to the 2008 Financial Crisis. Excluding volatile gas station sales (which surged 2.8% in April but 13.7% in March), core retail growth was only 0.3%, indicating inflation-adjusted spending actually declined when accounting for the 0.6% CPI increase.

For e-commerce sellers, the timing is critical: a $22 billion tax refund boost masked April weakness, but economist Oliver Allen projects this support will "taper dramatically in May," exposing consumers to sustained fuel pressures without offsetting income. The convergence of three factors creates a demand cliff: (1) fading tax refunds equivalent to 3% of monthly retail sales, (2) elevated energy costs requiring two months to fully impact household budgets, and (3) depressed consumer sentiment from the University of Michigan survey showing record-low confidence in major purchase conditions. This directly threatens discretionary categories—apparel, furniture, automotive accessories, and home goods—where cross-border sellers generate significant volume.

Retail partnership and O2O opportunities emerge as sellers pivot to offline presence to rebuild trust and capture remaining discretionary spending. With department store sales down 3.2% and consumer confidence plummeting, sellers in affected categories should accelerate pop-up and showroom strategies in high-income metros (New York, Los Angeles, Chicago, Boston) where discretionary spending remains resilient despite energy headwinds. The labor market strength (4.3% unemployment, 115,000 jobs added) provides a foundation for targeted offline experiences that can convert hesitant online browsers into committed buyers. Sellers should expect May-June to be the critical test period—if energy costs remain elevated without compensating wage growth, the second half of 2026 could trigger sustained demand destruction across multiple categories, making offline brand presence and experiential retail essential for maintaining market share and customer LTV.

Questions 8

What does Whirlpool's earnings miss reveal about appliance demand for cross-border sellers?

Whirlpool reported first-quarter 2026 earnings missing expectations, with CFO Roxanne Warner stating demand for appliances reached 'recession-level lows,' with the industry contracting 7.4%—comparable to Great Financial Crisis levels. This signals that major durable goods categories are experiencing severe demand destruction, not just minor pullbacks. For cross-border sellers in home appliances, kitchen equipment, and related categories, this represents a structural demand shift, not a temporary slowdown. The 7.4% industry contraction suggests sellers should expect 10-15% volume declines in Q2 2026 and consider shifting inventory to non-discretionary categories or building offline presence to capture remaining high-income consumers.

Which US cities offer the highest ROI for pop-up retail strategies during this demand crisis?

High-income metropolitan areas with resilient discretionary spending—New York, Los Angeles, Chicago, Boston, and San Francisco—should be prioritized for pop-up and showroom strategies. These markets have consumer bases less sensitive to energy price shocks and higher average household incomes to absorb fuel cost increases. The labor market strength (4.3% unemployment, 115,000 jobs added in April) is concentrated in these metros, providing a foundation for offline brand experiences. Pop-up stores in these locations can serve as trust-building touchpoints for hesitant online browsers, potentially increasing customer LTV by 20-30% through experiential engagement. Sellers should target 2-3 month pop-up windows in Q2-Q3 2026 before potential demand cliff in H2 2026.