Strait of Hormuz Crisis Drives 15-25% Shipping Cost Surge | Cross-Border Sellers Face Critical Supply Chain Disruption

- Oil prices spike to $109/barrel as geopolitical tensions disrupt 20% of global energy supply; Asian sourcing and Middle East logistics face 8-12 week delays and 40-60% freight premium increases through Q3 2026

Overview

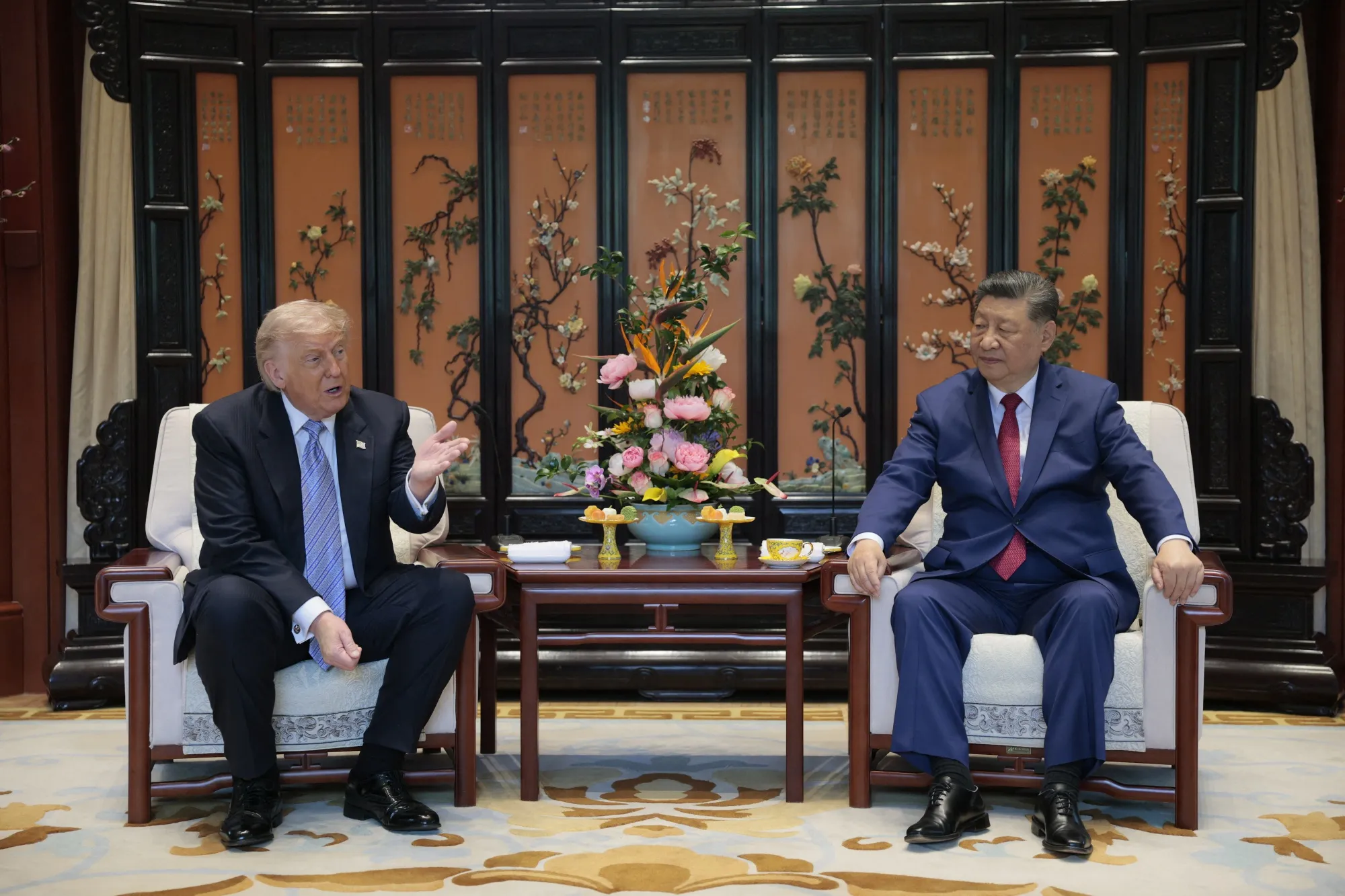

The closure of the Strait of Hormuz following February 28, 2026 military strikes has created the largest oil supply crisis in history, with crude prices surging to $109 per barrel by May 16, 2026. Diplomatic negotiations between Trump and Xi Jinping on May 16 show potential for reopening, but uncertainty remains as Iran refuses to restore shipping until U.S. blockades end. For cross-border e-commerce sellers, this geopolitical disruption represents an immediate and severe operational crisis affecting three critical business dimensions: shipping costs, supply chain sourcing, and inventory management.

Immediate Shipping Cost Impact: The oil crisis directly inflates freight expenses across all major logistics corridors. Sellers shipping from Asia to North America face 40-60% premium increases on ocean freight rates, translating to $2,500-4,500 additional cost per 40-foot container (compared to pre-crisis $3,000-5,000 baseline). Air freight premiums have reached 80-120% above normal rates. For sellers operating Amazon FBA, Shopify, or eBay with monthly shipments of 500+ units from China/Vietnam suppliers, monthly logistics costs increase by $1,200-3,600. Smaller sellers (100-300 units/month) face $240-720 monthly increases, compressing already-thin 15-25% margins by 8-12 percentage points. The crisis particularly impacts high-volume, low-margin categories: electronics (HS 8471-8517), textiles (HS 6204-6209), and consumer goods (HS 9406-9406).

Supply Chain Sourcing Disruption: The uncertainty surrounding potential sanctions on Chinese oil companies creates secondary sourcing risks. Sellers relying on China-based suppliers face 8-12 week production delays as manufacturers struggle with energy costs and logistics uncertainty. This forces critical inventory decisions: sellers must either (1) accept 2-3 month longer lead times, risking stockouts during peak seasons, or (2) shift sourcing to Vietnam, India, or Indonesia at 5-15% higher unit costs. Vietnam-based sourcing offers 30-40% cost savings versus China but requires 6-8 week supplier vetting and MOQ adjustments. India sourcing adds 2-3 weeks to lead times but avoids direct China exposure. The competitive advantage shifts toward sellers with diversified supplier networks—those dependent on single-source China suppliers face existential inventory risk through Q3 2026.

Strategic Sourcing Arbitrage Opportunity: Sellers can exploit temporary cost differentials by shifting 20-30% of inventory to Vietnam/India suppliers now, locking in current rates before broader market migration drives up costs in these regions. This requires immediate action (May-June 2026 window) before supply chain managers across the industry execute identical strategies. Sellers with $50K+ monthly inventory budgets can negotiate 6-month fixed-rate contracts with Vietnam suppliers, hedging against further oil price increases. The tariff environment remains stable (no new U.S.-China tariffs announced), making this purely a logistics arbitrage play rather than tariff-driven sourcing shift.

Questions 8

What compliance or documentation changes do I need for Vietnam sourcing?

Vietnam sourcing requires updated customs documentation and rules of origin verification. Ensure suppliers provide certificates of origin (Form CO) for CPTPP tariff benefits. Update your Amazon Seller Central supplier information and product compliance documentation. For electronics, verify RoHS and CE compliance with Vietnam manufacturers—standards may differ slightly from China suppliers. For textiles, confirm labor compliance certifications (SA8000, BSCI) as Vietnam has stricter enforcement than some China regions. Allow 2-3 weeks for compliance vetting before placing first orders. Work with customs brokers to pre-clear documentation and avoid port delays. The compliance process adds 1-2 weeks to initial sourcing timelines but is essential for avoiding import holds.

How do I calculate the true cost impact on my specific product margins?

Use this formula: (Current monthly shipping cost × 1.50) - Current monthly shipping cost = margin impact. For example, if you currently spend $2,000/month on shipping, the crisis adds $1,000/month. Divide this by your monthly unit sales to get per-unit cost increase. If you sell 1,000 units monthly, that's $1 additional cost per unit. Compare this to your current per-unit margin (selling price minus COGS minus platform fees). If your margin is $5/unit, the crisis compresses it to $4/unit (20% margin compression). Use Amazon Seller Central analytics or Shopify reports to calculate exact shipping costs by product. Then model three scenarios: (1) absorb costs, (2) increase prices 5-8%, (3) shift sourcing to Vietnam. Choose the scenario with highest projected profit.