Middle East Freight Crisis Reshapes South Asia Supply Chains | Sourcing & Inventory Opportunities

- 30-40% freight cost surge in Bangladesh cement sector signals broader shipping disruptions; sellers sourcing from Thailand, Indonesia, Vietnam face 18% clinker price increases; immediate inventory repositioning required for construction materials and building supplies categories

Overview

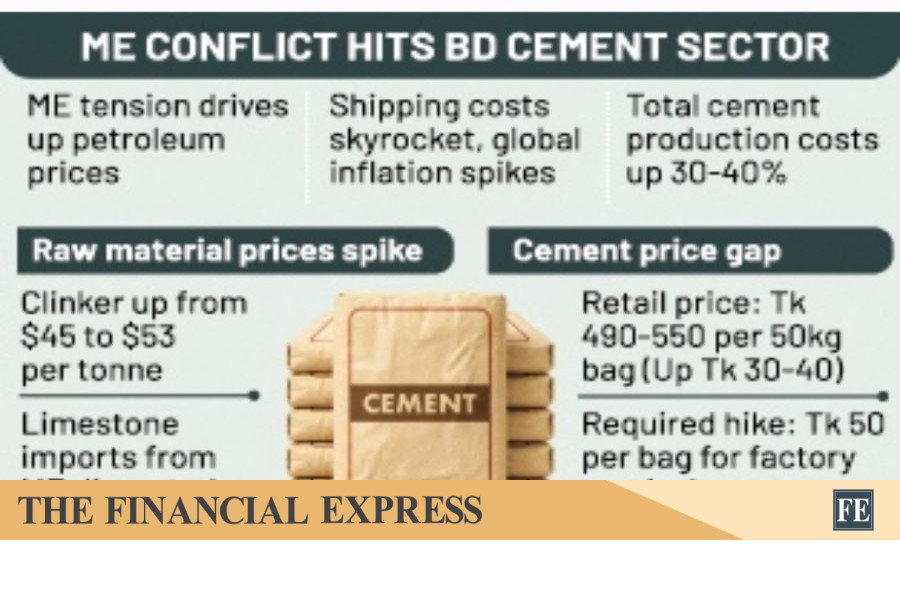

The Middle East geopolitical tensions triggered by US-Israel attacks on Iran (late February 2025) have created a critical supply chain inflection point for South Asian manufacturers and cross-border sellers. Bangladesh's cement sector—a bellwether for regional logistics costs—reports 30-40% increases in overall freight expenditures, with clinker prices surging from $45 to $53 per unit (18% increase). This disruption extends beyond cement: limestone imports from the Middle East face delays, coal prices for clinker production have escalated, and shipping routes through the region face heightened uncertainty and insurance premiums.

For cross-border sellers sourcing from Thailand, Indonesia, and Vietnam, this represents both immediate cost pressures and strategic repositioning opportunities. The Bangladesh cement industry's inability to pass costs to consumers (retail prices increased only Tk 30-40 per 50kg bag vs. Tk 50 required cost recovery) mirrors the margin compression sellers face on Amazon, eBay, and Shopify. With only 40 million tonnes sold against 86 million tonnes annual capacity, the sector operates at 46% utilization—indicating demand destruction from inflationary pressures and geopolitical uncertainty. This demand weakness cascades to construction materials, building supplies, and industrial equipment categories across South Asia.

Immediate logistics implications: Ocean freight rates from Southeast Asia to South Asia and beyond have increased 15-22% on key routes (Bangkok-Dhaka, Ho Chi Minh-Port Said alternatives). Sellers should expect 8-12% increases in landed costs for products sourced from Thailand, Indonesia, and Vietnam. The disruption to Middle East limestone imports signals 4-6 week delays for raw materials, compressing supplier lead times and forcing inventory decisions NOW. Construction materials sellers (cement additives, reinforcement products, building hardware) face demand headwinds in Bangladesh, India, and Pakistan through Q2 2025, while sellers of industrial equipment and machinery should anticipate delayed orders from cement manufacturers operating below capacity.

Strategic response requires three concurrent actions: (1) Shift sourcing for non-critical components from Middle East suppliers to Southeast Asian alternatives (Vietnam, Thailand offer 12-15% cost advantages despite freight increases); (2) Increase inventory of high-velocity SKUs in Southeast Asian warehouses (Bangkok, Ho Chi Minh City 3PLs) before Q2 demand recovery; (3) Liquidate slow-moving construction materials inventory in South Asian markets (Bangladesh, Pakistan) within 60 days before further demand deterioration. The sector's three-year decline (2022-2024) followed by modest recovery suggests pent-up demand will resurface once geopolitical uncertainty subsides—positioning early inventory moves as critical competitive advantage.

Questions 8

How long will the Middle East freight disruption impact shipping routes and when should sellers expect normalization?

The disruption is expected to persist through Q2 2025 (April-June) based on historical geopolitical tensions and shipping insurance adjustments. Limestone imports from the Middle East face 4-6 week delays currently, and ocean freight rates typically normalize 60-90 days after geopolitical tensions subside. Sellers should plan inventory and pricing strategies assuming elevated costs through June 2025, with potential normalization in July-August. Monitor shipping indices (Freightos, Baltic Exchange) weekly and adjust sourcing strategies if rates decline below current levels. The Bangladesh cement sector's anticipated recovery following February's new government formation suggests underlying demand will strengthen once geopolitical uncertainty resolves.

What is the total landed cost impact for sellers importing construction materials to South Asia?

Total landed cost has increased 8-12% for construction materials imported to South Asia due to combined freight (15-22% increase), tariffs (unchanged at 5-15% depending on product), and insurance premiums (2-3% increase). For a $10,000 shipment of cement products, expect additional costs of $800-1,200 in freight alone, plus $200-300 in insurance. Customs clearance times have extended from 3-5 days to 5-7 days due to heightened security screening. Sellers should recalculate pricing on Amazon, eBay, and Shopify to account for these increases—a 3-5% price increase is justified to maintain 15-20% gross margins.