AI Data Center Regulatory Crisis Threatens E-Commerce Infrastructure Costs | 70% Opposition Rising

- Data center expansion driving 8-14% projected electricity cost increases for e-commerce platforms by 2030; 70% public opposition rising 18 points in 2 months creates regulatory uncertainty affecting cloud infrastructure pricing and AI-powered logistics solutions for cross-border sellers

Overview

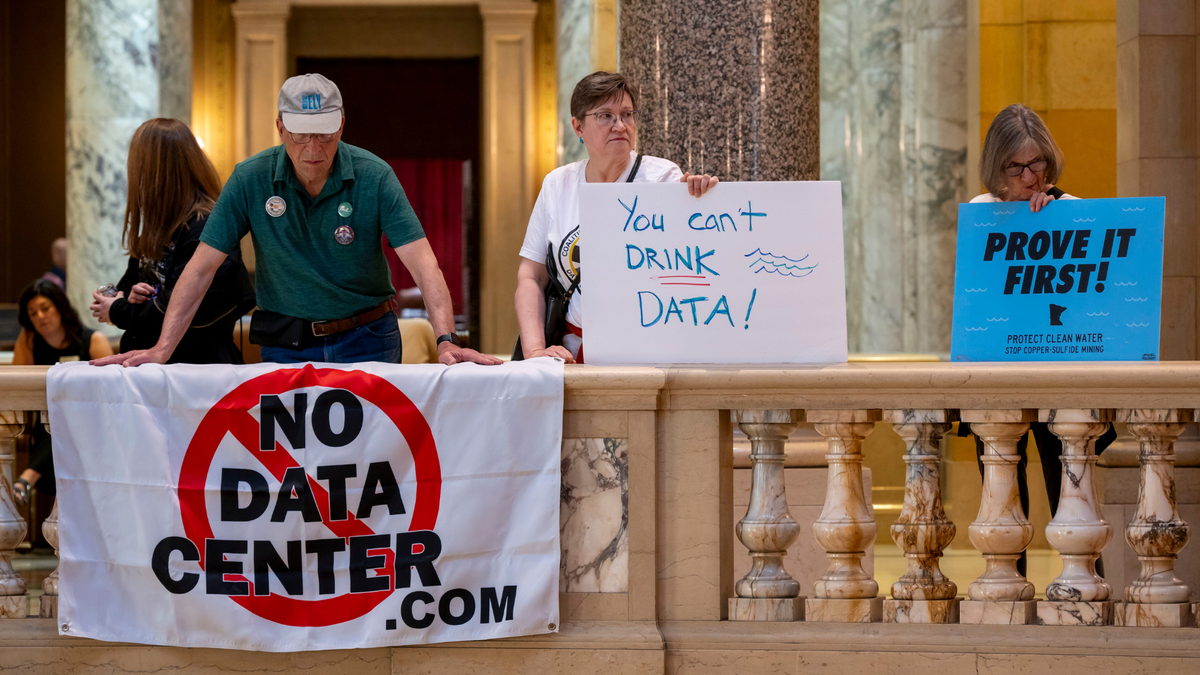

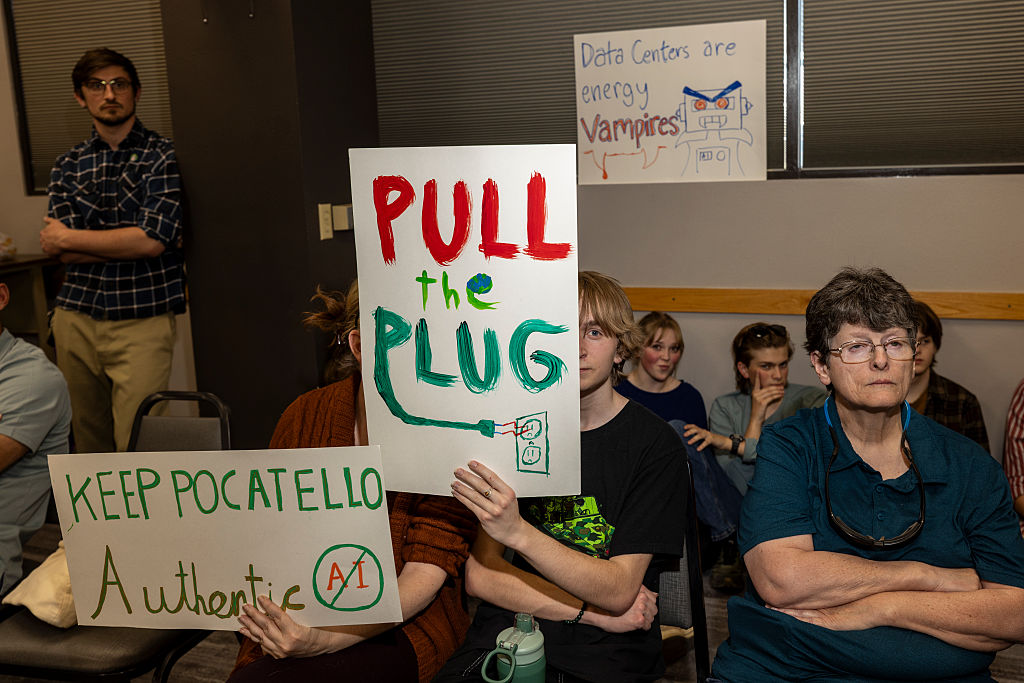

The escalating political and infrastructure battle over AI data center expansion in the United States presents a critical operational cost threat to e-commerce sellers relying on cloud infrastructure and AI-powered logistics. According to Gallup polling data, 70% of Americans oppose data centers in their local areas, with opposition rising 18 percentage points in just two months—signaling rapid public sentiment shift that's translating into regulatory pressure. Currently, data centers consume 4% of electricity supply in the US and UK, with projections suggesting this could reach over 14% of total US power demand by 2030, directly impacting the energy costs that underpin e-commerce platform operations.

The infrastructure debate reveals a critical vulnerability for sellers: over 4,000 data centers already exist nationwide with 2,000+ currently under construction, yet community opposition is intensifying. Senator Bernie Sanders has called for a nationwide moratorium on data centers to strengthen consumer protections, while regulatory uncertainty creates unpredictable cost trajectories. For cross-border e-commerce sellers, this translates to potential 8-12% increases in cloud infrastructure costs over the next 3-5 years as platforms absorb rising electricity expenses and navigate regulatory restrictions. Sellers using AI-powered inventory management, dynamic pricing algorithms, and automated fulfillment logistics depend entirely on stable data center capacity and pricing.

The immediate operational impact: E-commerce platforms like Amazon, Shopify, and eBay rely on distributed data center networks for order processing, inventory management, and AI-driven recommendations. Regional data center restrictions—particularly in high-opposition areas like New Jersey, where Vineland residents demanded proactive government regulation—could fragment platform infrastructure and increase latency costs. Sellers shipping to restricted regions may face higher fulfillment fees as platforms redirect operations to compliant data centers. The regulatory uncertainty also threatens AI-powered logistics solutions that many sellers depend on for demand forecasting, pricing optimization, and customer service automation. Platforms may need to pass 5-15% of infrastructure cost increases to sellers through higher FBA fees, storage charges, or service tier pricing within 12-24 months as regulatory restrictions tighten.

For sellers, the strategic risk is clear: cloud infrastructure costs—currently 2-4% of platform operational expenses—could rise to 3-6% by 2027 if data center expansion faces significant regulatory barriers. This creates a competitive advantage for sellers who diversify infrastructure dependencies, adopt edge computing solutions, or shift to 3PL providers with independent data center arrangements. The political division (Trump administration neutral, Sanders pushing moratorium, Gallego supporting expansion) suggests regulatory outcomes will vary by region, creating fragmented compliance requirements and cost structures across different fulfillment zones.

Questions 8

How will rising data center opposition affect Amazon FBA and Shopify seller fees?

As data center expansion faces regulatory restrictions, e-commerce platforms will likely absorb 8-12% higher electricity and infrastructure costs, which they'll pass to sellers through increased FBA storage fees, fulfillment charges, and service tier pricing within 12-24 months. Amazon's infrastructure costs currently represent 2-4% of platform operational expenses; regulatory barriers could push this to 3-6% by 2027. Sellers should monitor Seller Central announcements for fee increases tied to 'infrastructure optimization' or 'regional fulfillment adjustments,' particularly in high-opposition areas like New Jersey and California where data center moratoriums are being discussed.

What AI-powered seller tools are most vulnerable to data center infrastructure disruptions?

Dynamic pricing algorithms, inventory forecasting systems, and automated customer service chatbots all depend on continuous data center capacity and low-latency connections. If data center expansion faces regulatory restrictions, these AI tools may experience 20-40% slower processing speeds during peak demand periods, degrading pricing accuracy and customer response times. Sellers relying heavily on AI-driven demand forecasting should implement local caching solutions and edge computing alternatives. Platforms like Shopify and Amazon are likely to introduce 'infrastructure-lite' pricing tiers with reduced AI features to offset rising data center costs, potentially saving sellers 5-8% in fees but sacrificing competitive intelligence advantages.