Nvidia's $78.91B Revenue Beat Signals AI Infrastructure Costs for E-Commerce Sellers

- 80% YoY growth expected but macroeconomic headwinds may suppress stock gains; cloud computing costs for seller tools at risk

Overview

Nvidia's Q1 earnings report (released Wednesday after market close) projects $78.91 billion in revenue with 80% year-over-year growth and EPS more than doubling to $1.75—yet analyst Chris Senyek (Wolfe Research) warns that despite two consecutive years of beating consensus estimates, the stock's post-earnings price action has been "relatively weak." This disconnect between operational excellence and market valuation creates critical implications for cross-border e-commerce sellers relying on AI-powered tools and cloud infrastructure.

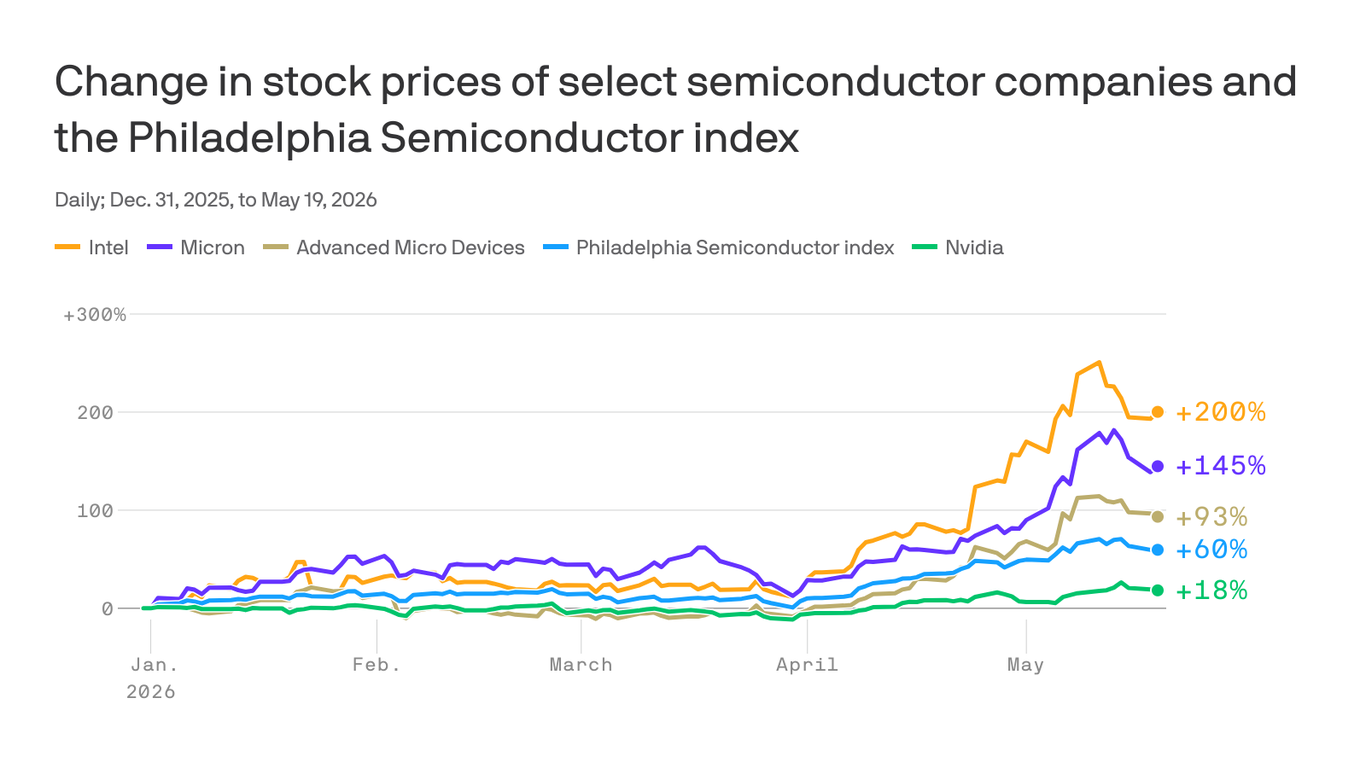

The core issue: macroeconomic headwinds (rising bond yields, interest rates) now dominate market sentiment more than earnings fundamentals. Nvidia's $5.4 trillion market cap positions it as the world's largest company, yet retail traders have diversified away—Intel surged 150% since March, Micron and AMD doubled, while Nvidia gained only 26.5% year-to-date. This investor rotation signals potential underinvestment in AI infrastructure, which directly impacts the cost and availability of AI tools sellers depend on: inventory management systems, dynamic pricing engines, customer service automation, and product research platforms. All these tools run on Nvidia GPU infrastructure through cloud providers like AWS, Google Cloud, and Azure.

For sellers, the immediate risk is cost inflation for AI-powered services. If Nvidia's stock underperforms despite strong fundamentals, the company may reduce R&D spending on next-generation GPU architectures, slowing innovation cycles. This creates supply constraints for cloud providers, who typically pass costs to end-users. Sellers using AI tools for listing optimization, competitor analysis, and demand forecasting could face 8-15% price increases on SaaS subscriptions within 6-12 months. Additionally, Bank of America analysts note that Nvidia may need to implement "increased stock buybacks or enhanced cash returns" to reignite investor enthusiasm—capital allocation that could reduce investment in data center GPU production, further tightening supply.

The strategic opportunity lies in AI tool adoption timing. Sellers should evaluate their current AI tool stack (Helium 10, Jungle Scout, Keepa, ChatGPT for content) and lock in multi-year contracts NOW before potential price increases. The earnings report serves as a barometer for AI investment momentum; if Nvidia's guidance disappoints despite strong current results, cloud infrastructure costs will rise 6-12 months later. Conversely, if the company commits to aggressive capital expenditure, sellers benefit from stable or declining AI tool costs through 2025.

Questions 8

How does Nvidia's $5.4 trillion market cap affect cross-border seller operations?

Nvidia's dominance in GPU infrastructure means its financial health directly influences cloud computing costs globally. As the world's largest company by market cap, Nvidia sets pricing power for data center GPUs used by AWS, Google Cloud, and Azure—the platforms hosting AI tools for 2M+ e-commerce sellers worldwide. If Nvidia's stock continues underperforming (despite strong fundamentals), investor pressure may force cost-cutting that reduces GPU production or innovation. For cross-border sellers, this translates to higher cloud infrastructure costs, which platform providers pass to sellers through increased FBA fees, Shopify transaction fees, or SaaS subscription increases. Monitor Nvidia's quarterly guidance as a leading indicator of technology cost inflation 6-12 months ahead.

What specific AI tools should sellers prioritize before potential price increases?

Prioritize tools that directly impact profitability: (1) Dynamic pricing engines (RepricerIt, Keepa) that optimize margins in real-time, (2) Inventory forecasting systems (Helium 10, Jungle Scout) that reduce overstock costs, and (3) Customer service automation (Intercom, Zendesk) that reduce labor costs. These tools generate 15-30% ROI through margin improvement and operational efficiency. If Nvidia's underperformance leads to cloud cost inflation, these high-ROI tools will see price increases first. Negotiate 24-36 month contracts now at current rates; the cost of a 2-year commitment ($2,000-5,000 annually) is far lower than absorbing 10-15% annual increases over 3 years.