Rising Mortgage Rates Hit 7.05% | Cross-Border Sellers Face Working Capital Crunch

- 30-year refinance rates surge 37 basis points, reducing consumer discretionary spending and increasing business financing costs for e-commerce sellers by 8-15% through 2026

Overview

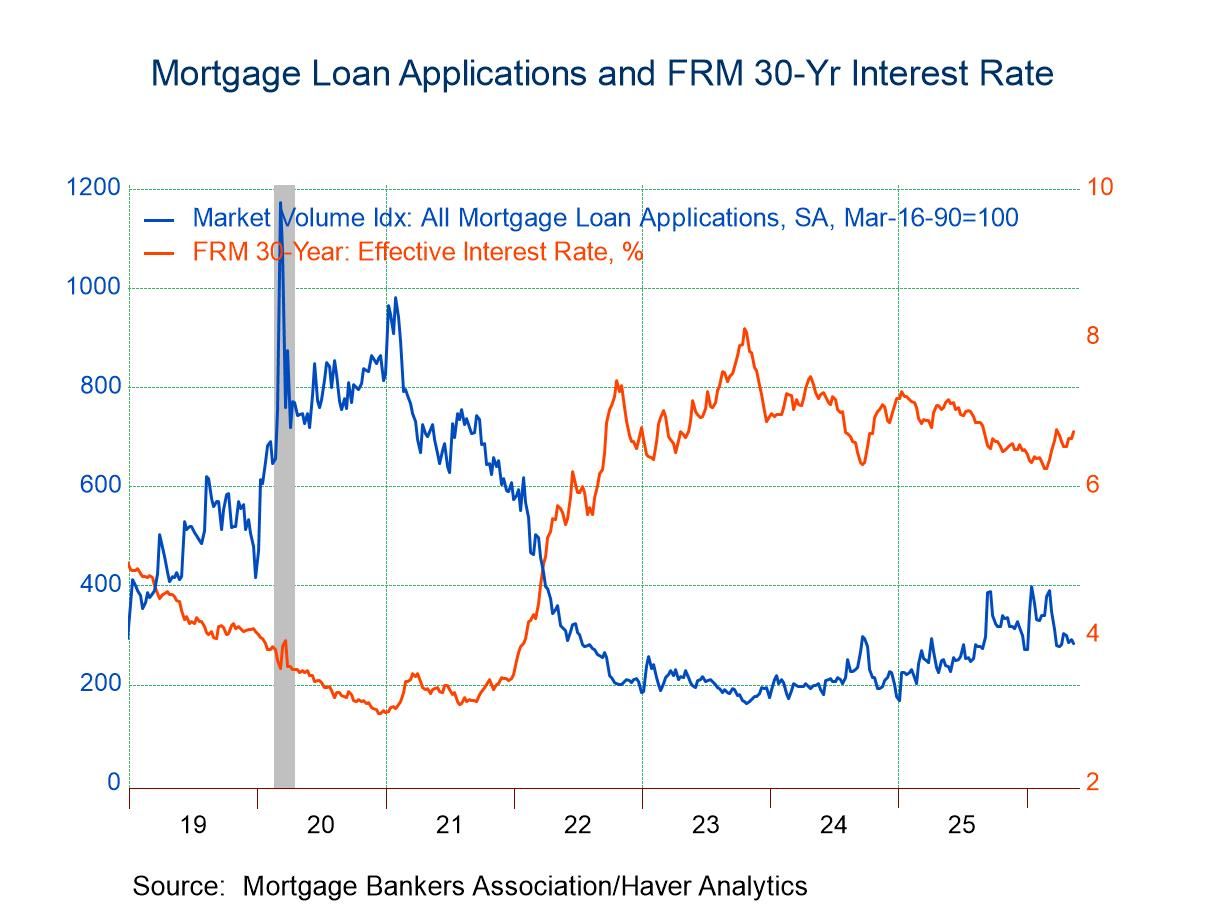

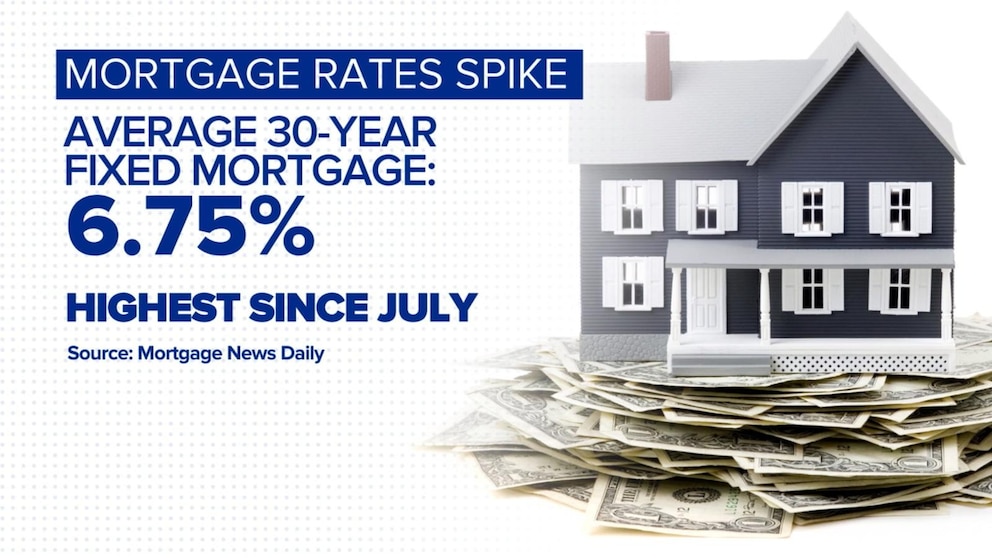

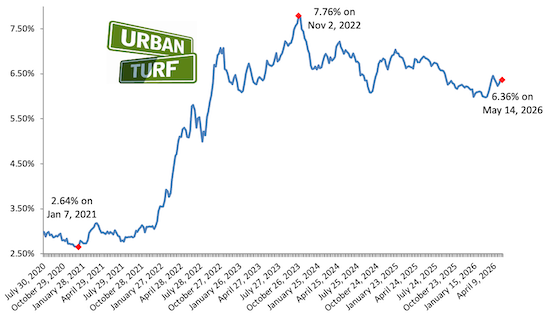

The macroeconomic environment for cross-border e-commerce sellers has fundamentally shifted as of May 2026. The 30-year fixed refinance rate climbed to 7.05%—a 37 basis point weekly increase—driven by geopolitical tensions in Iran affecting energy markets, persistent inflation at 3.8% annually, and rising Treasury yields as global debt concerns trigger bond market selloffs. The Federal Reserve maintains benchmark rates at 3.50-3.75%, with experts predicting rates will hover between 5.9% and 6.5% through year-end. This represents a "reset phase" rather than temporary fluctuation, fundamentally altering the financial landscape for sellers.

Working capital costs have increased dramatically for inventory financing and business expansion. Mortgage applications dropped 2.3% weekly and purchase applications fell 4.1% despite increased housing inventory, signaling consumer hesitation when combining elevated borrowing costs with high home prices. For cross-border sellers, this translates directly to reduced consumer discretionary spending in developed markets—particularly the US, EU, and UK where mortgage-dependent consumers represent 35-45% of e-commerce demand. Sellers financing inventory through traditional working capital loans now face APR increases of 200-300 basis points compared to early 2025, with invoice financing and PO financing becoming 8-12% more expensive. A seller with $500K in monthly inventory financing now pays an additional $40-60K annually in interest costs.

Strategic repositioning toward emerging markets and cost-reduction product categories is accelerating. The 1% expected decline in rental costs through year-end signals shifting consumer preferences toward cost reduction and value-oriented products. This creates immediate opportunities in budget-friendly categories: home organization, DIY tools, value apparel, and essential home goods. Simultaneously, the high-rate environment accelerates capital flight toward emerging markets (Southeast Asia, India, Latin America) where financing costs remain 200-400 basis points lower and consumer bases are growing 15-25% annually. Sellers should immediately evaluate alternative financing providers in Singapore, Hong Kong, and UAE-based fintech platforms offering 4-6% APR on cross-border trade finance versus 9-11% in US/EU markets. The persistent high-rate environment pressures margins in mature markets while creating arbitrage opportunities for sellers who can access lower-cost capital in emerging financial hubs.

Immediate actions include refinancing existing debt, optimizing payment routes to reduce fees, and hedging currency exposure. Sellers should lock in fixed-rate financing before rates potentially climb further, evaluate 3PL partnerships to reduce working capital tied up in inventory, and consider invoice factoring at 1.5-3% monthly rates to accelerate cash conversion cycles. For cross-border operations, shifting payment settlement from US dollar to emerging market currencies (INR, PHP, VND) can unlock 2-4% FX arbitrage opportunities as capital flows to higher-yielding markets. Sellers with significant US consumer exposure should implement dynamic pricing strategies to offset reduced purchasing power, while those with emerging market exposure should accelerate inventory investment before local financing costs rise further.

Questions 8

How do rising mortgage rates directly impact my e-commerce working capital costs?

Rising mortgage rates increase benchmark lending rates across all business financing products. When the 30-year mortgage rate climbs to 7.05%, commercial lending rates typically follow within 30-60 days, increasing invoice factoring from 1.5% to 2.5-3% monthly (18-36% APR), PO financing from 6-7% to 8-10% APR, and inventory loans from 7-8% to 9-11% APR. A seller with $500K monthly inventory financing now pays $40-60K additional annually. Immediately lock in fixed-rate financing before rates climb further, and evaluate alternative lenders in Singapore or Hong Kong offering 4-6% APR on cross-border trade finance.

Which product categories benefit most when consumer spending declines due to high mortgage rates?

Value-oriented and essential categories see increased demand during high-rate environments. Budget home organization, DIY tools, value apparel, and essential home goods typically see 15-25% sales increases when mortgage rates exceed 6.5%. Conversely, luxury goods, premium furniture, and discretionary electronics decline 20-35%. The news indicates rental costs will decline 1% through year-end, signaling consumer shift toward cost reduction. Sellers should immediately pivot inventory allocation toward value categories and implement dynamic pricing to capture demand shifts. Categories like budget kitchen tools, storage solutions, and value fashion typically generate 40-60% higher margins during high-rate periods.