Walmart Q1 Earnings Miss Signals Consumer Pullback | Seller Margin Pressure Ahead

- Walmart's 7% stock decline and weakened FY2027 guidance reveal $175M fuel cost headwinds; sales growth expected to decelerate from 7.3% to 4-5% as consumer spending contracts amid 52% gas price surge

Overview

Walmart's May 16, 2024 earnings report reveals a critical inflection point for U.S. retail and cross-border e-commerce sellers. Despite beating revenue expectations at $177.75 billion (up 7% YoY), the retail giant's weaker-than-expected guidance—projecting FY2027 adjusted EPS of $2.75-$2.85 versus consensus $2.91—signals deteriorating consumer health. The company absorbed a $175 million fuel cost headwind in Q1 with expectations for larger impacts in Q2, while forecasting sales growth to decelerate from 7.3% YoY in Q1 to just 4-5% in the May-July period.

The root cause: geopolitical fuel inflation compressing household budgets. Gasoline prices surged 52% from $3.00 to $4.56 per gallon due to Middle East tensions, forcing American households to cut discretionary spending. Finance Chief John David Rainey explicitly warned that fading tax refund effects mean consumers will "feel more pressure from higher fuel prices" starting in May 2024. This creates a dual squeeze on cross-border sellers: (1) consumer demand contraction particularly in discretionary categories, and (2) logistics cost escalation from fuel surcharges affecting fulfillment fees and shipping margins.

However, Walmart's earnings reveal critical divergence in consumer behavior. Global e-commerce sales surged 26% while the advertising business jumped 37%—indicating that value-conscious shoppers and higher-income consumers are shifting online. Same-store sales climbed 4.1%, showing resilience in physical retail. This bifurcation matters for sellers: budget-conscious consumers are consolidating purchases online and at Walmart, while discretionary categories face headwinds. Sellers relying on Walmart Marketplace or traditional fulfillment networks face margin compression from rising logistics costs, while those selling value-oriented products (essentials, budget items) may see demand acceleration.

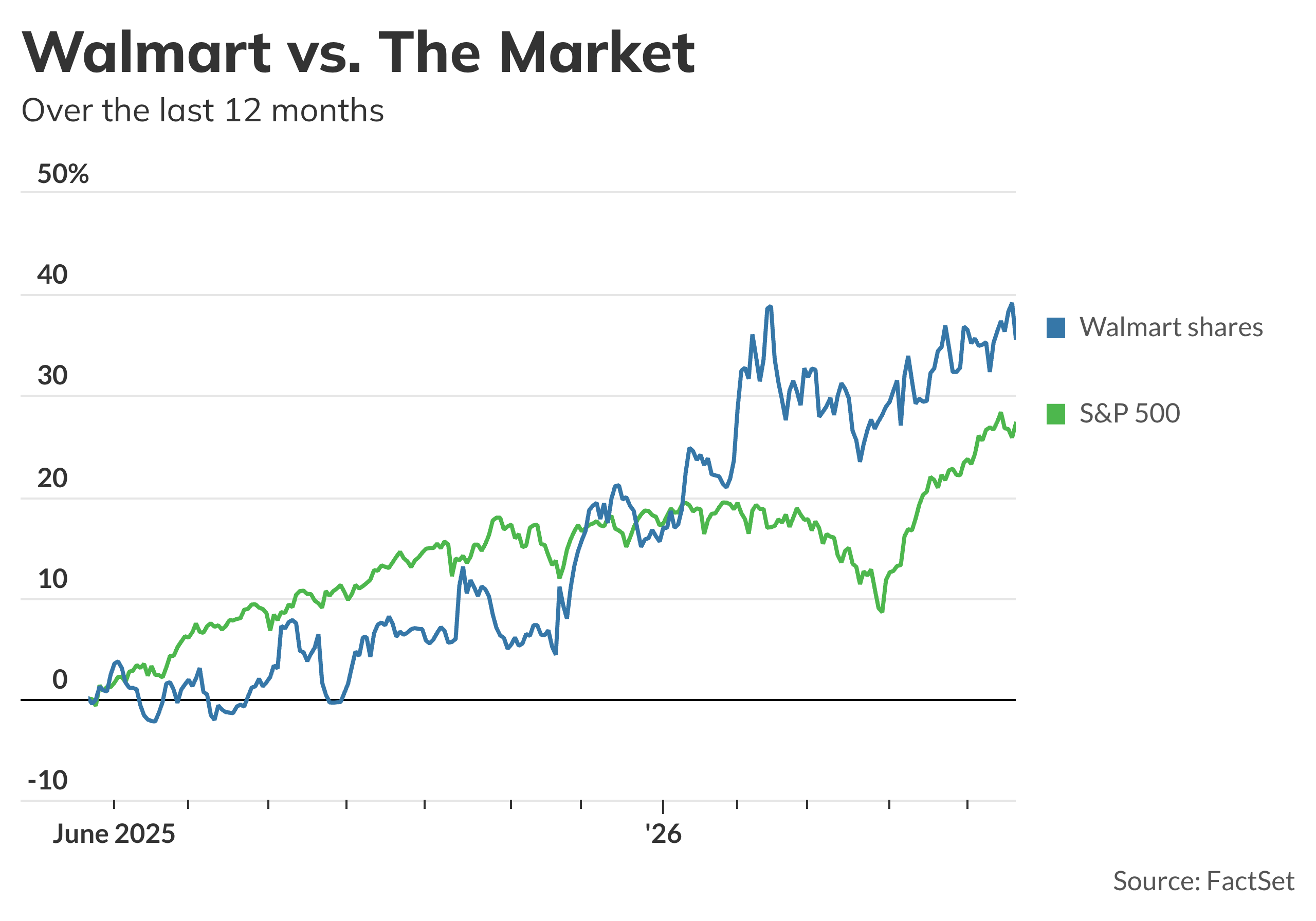

The broader context amplifies urgency. Consumer sentiment hit record lows in May 2024, sticky inflation persists, and interest rates remain elevated. Walmart's stock declined 7% on the earnings miss, signaling investor concerns about consumer spending sustainability. For sellers, this translates to: (1) inventory risk in discretionary categories through Q3 2024, (2) fulfillment cost increases of 8-15% if fuel prices persist, (3) stricter payment terms from retailers facing margin pressure, and (4) reduced promotional support from platforms managing profitability. The company's warning about potential food price increases from Strait of Hormuz disruptions adds supply chain risk for sellers sourcing agricultural products or food-adjacent categories.

Questions 8

What supply chain risks should sellers monitor following Walmart's Strait of Hormuz warning?

Walmart warned of potential food price increases and agricultural input shortages (fertilizer, nitrogen, phosphates) if the Strait of Hormuz closure persists. Sellers sourcing from Asia or dependent on agricultural inputs face: (1) 15-25% cost increases in fertilizer-dependent products by Q3 2024, (2) 2-4 week shipping delays if alternative routes are required, (3) inventory availability risks for food-adjacent categories. Sellers should diversify sourcing by January 2025, build 60-90 day safety stock in affected categories, and monitor geopolitical developments weekly. Consider shifting to domestic suppliers or alternative sourcing regions (India, Southeast Asia) to mitigate Suez Canal/Strait of Hormuz disruption risk.

Should sellers adjust pricing strategies as consumer sentiment hits record lows?

Yes. Walmart's guidance explicitly signals consumer financial stress, with sentiment hitting record lows in May 2024. Sellers should implement tiered pricing strategies: (1) reduce prices 5-10% on value-oriented products to capture market share from competitors, (2) maintain or increase prices 2-5% on premium/discretionary items targeting higher-income segments (which Walmart notes are more resilient), (3) introduce budget product lines to capture price-sensitive shoppers. Avoid aggressive price increases on essentials; instead, optimize margins through volume growth. Monitor competitor pricing weekly through Q3 2024, as margin-pressured retailers will likely implement aggressive discounting.