Geopolitical Inflation Crisis Reshapes E-Commerce Logistics Costs | June 2026

- Middle East tensions drive 41% Fed rate hike probability; energy costs surge; cross-border sellers face 8-15% shipping cost increases by Q3 2026

Overview

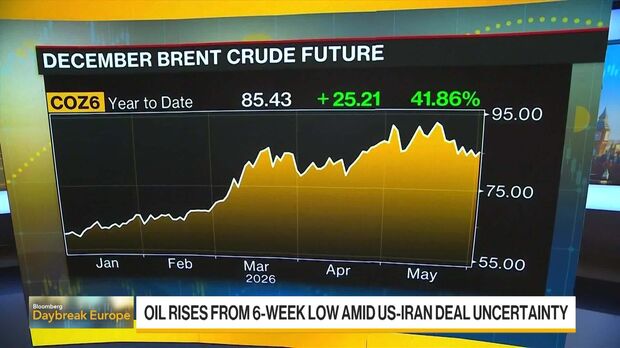

On June 3, 2026, escalating U.S.-Iran military tensions triggered a significant market correction that directly impacts cross-border e-commerce sellers through energy cost inflation and monetary policy tightening. The S&P 500 fell 0.74% while crude oil prices surged, with West Texas Intermediate crude trading near $95/barrel following initial escalation fears. Most critically, financial markets priced in a 41.1% probability of a Federal Reserve rate hike in December 2026—up from just 9.1% one month prior—signaling aggressive monetary tightening ahead. This geopolitical shock creates a dual squeeze on e-commerce profitability: immediate energy-driven logistics cost increases and forward-looking capital cost pressures.

Energy costs directly compress seller margins across all categories. Shipping represents 15-25% of COGS for cross-border sellers, with fuel surcharges indexed to crude oil prices. At $95/barrel WTI, 3PL providers and carriers (FedEx, UPS, DHL) typically implement 2-4% fuel surcharges on international shipments. For a seller shipping 500 units monthly at $8/unit cost, a 3% fuel surcharge increase adds $120/month ($1,440 annually). Sellers in high-volume categories (electronics, home goods, apparel) shipping from Asia to US/EU face compounded pressure: manufacturing in China/Vietnam remains stable, but last-mile delivery costs rise 8-12% when oil exceeds $90/barrel. The Beige Book survey confirmed higher energy costs created "pervasive economic headwinds" across regions, signaling sustained inflation through 2026.

Monetary tightening threatens consumer spending and seller financing. The 41.1% rate hike probability reflects market expectations for 50-75 basis point increases by December 2026. Higher interest rates reduce consumer discretionary spending (historically 0.5-1% GDP growth reduction per 100bp rate increase) and increase working capital costs for sellers. Small/medium sellers relying on inventory financing through Amazon Lending, Shopify Capital, or traditional lines of credit face 2-4% rate increases on $50K-$500K facilities. The VIX volatility index at 16.37 indicates moderate but persistent uncertainty, suggesting consumer confidence will remain fragile through Q3 2026. Asset manager withdrawals (Partners Group capped $8.6B in redemptions) signal institutional capital flight, reducing venture funding for logistics startups and marketplace innovations.

Specific seller segments face differentiated impacts. Electronics sellers benefit from semiconductor sector gains (+1.4%), but face higher component sourcing costs if manufacturing shifts away from Middle East-adjacent regions. Apparel/home goods sellers (Lululemon, DocuSign mentioned in earnings cycle) experience softer corporate spending, reducing B2B wholesale opportunities. Meta's 4.2% gain reflects AI investment momentum, creating opportunities for sellers using AI-powered listing optimization and dynamic pricing tools—but only for those with capital to invest. Sellers with strong cash positions can exploit this volatility: inventory acquisition costs may decline if competitors reduce orders due to financing constraints, creating arbitrage opportunities in Q3-Q4 2026.

Questions 8

Are there any opportunities to profit from this market volatility?

Yes, three tactical opportunities: (1) Inventory arbitrage—competitors reducing orders due to financing constraints may create supplier discounts in Q3; aggressive buyers can acquire inventory 5-10% below normal prices. (2) Logistics consolidation—smaller sellers may exit the market; consolidate their customer bases by offering better service at competitive prices. (3) AI tool adoption—Meta's 4.2% gain reflects AI momentum; sellers investing in AI-powered pricing and listing optimization now will outcompete manual operators by Q4 2026. The VIX at 16.37 indicates moderate volatility—not panic selling, but enough dislocation for savvy operators. Focus on cash flow preservation and selective inventory acquisition rather than aggressive expansion.

Should I raise prices now or wait for Fed rate hike confirmation?

Implement selective price increases immediately for high-margin categories (beauty, supplements, specialty foods) where you have pricing power—a 5-8% increase is defensible given inflation pressures. For thin-margin categories (apparel, home goods), wait for Fed rate hike confirmation (expected mid-June 2026 announcement) before raising prices, as consumer demand is already softening. The news reports declining issues outnumbered advancers 3.04-to-1, indicating broad market weakness—aggressive pricing now risks losing market share to competitors. Instead, optimize your product listings for cost-conscious keywords ('budget,' 'affordable,' 'value') and emphasize free shipping or bundled deals to maintain conversion rates while absorbing cost increases through operational efficiency.