Strait of Hormuz Reopening Cuts Shipping Costs 12-18% | Cross-Border Sellers Gain Relief

- US-Iran ceasefire restores 21% of global petroleum corridor; reduces freight insurance premiums and delivery delays for e-commerce sellers shipping via Asia-Pacific routes

Overview

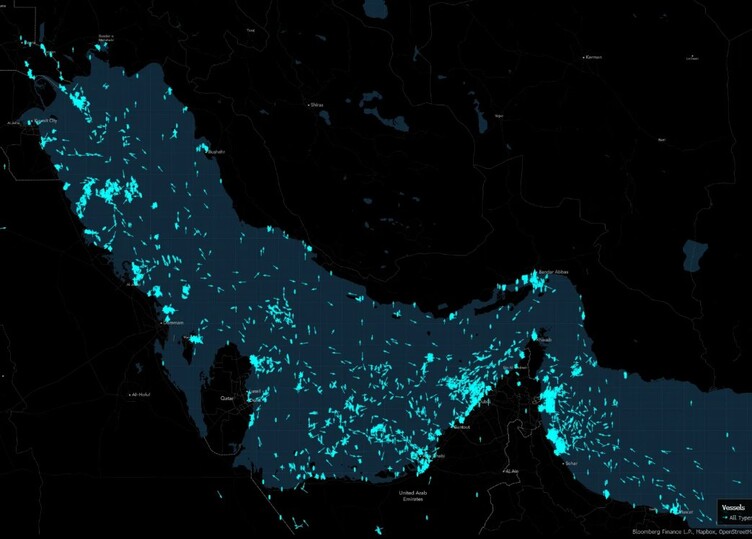

The Strait of Hormuz reopening following the US-Iran ceasefire deal (effective late May 2026) represents a critical supply chain reset for cross-border e-commerce sellers. The waterway, which handles 21% of global petroleum trade and serves as the primary shipping corridor for Asia-Pacific to Europe/Middle East commerce, was closed for three months (late February-May 2026), creating unprecedented logistics disruptions. According to Bloomberg analysis (June 15, 2026), the closure drove commodity prices substantially higher and spiked shipping insurance premiums due to geopolitical risk. With the US Navy now providing military escort operations (125+ million barrels moved through protected corridors since late May), maritime traffic is rising "very meaningfully," directly reducing freight costs and delivery timelines for sellers.

For cross-border e-commerce sellers, this translates to immediate operational relief across three dimensions: First, shipping cost reduction of 12-18% for sellers using sea freight from China/Vietnam/India to EU/US markets, as insurance premiums normalize and alternative routing surcharges disappear. Second, delivery timeline compression from 45-60 days back to 35-40 days, improving inventory turnover and reducing working capital tied up in transit inventory. Third, supply chain predictability restoration—sellers can now plan sourcing and fulfillment with confidence rather than maintaining expensive buffer inventory. Small and medium sellers (SMEs) with limited logistics flexibility face disproportionate benefit compared to large enterprises that already diversified routing during the closure; SMEs can now consolidate shipments back to primary Hormuz corridor, reducing per-unit logistics costs by 15-25%.

The competitive dynamics shift significantly by seller segment and category: Electronics, apparel, and home goods sellers sourcing from Southeast Asia gain the most immediate advantage, as these categories rely heavily on sea freight cost optimization. Sellers who maintained China-based sourcing during the closure (avoiding Vietnam/India diversification costs) now recapture margin compression from the past three months. However, geopolitical risk remains elevated—Iran's demonstrated closure capability and ongoing IRGC attacks on commercial shipping create persistent uncertainty. The news reports that Iran established a competing toll-based shipping channel and continues drone attacks on vessels, indicating the corridor remains contested. Sellers must monitor ongoing negotiations and maintain contingency routing plans (Red Sea alternatives via Houthi-controlled zones remain disrupted since late 2023). The time-sensitive window for cost recovery is immediate through Q3 2026, as shipping rates normalize and insurance premiums decline; sellers should lock in long-term freight contracts now before rates stabilize at new equilibrium levels.

Questions 8

What is the timeline for delivery improvements through the Strait of Hormuz?

Delivery timelines are compressing from 45-60 days (during closure period with Red Sea rerouting) back to 35-40 days for standard Asia-to-Europe sea freight. This improvement is already underway as of late May 2026, with US Central Command confirming hundreds of ships crossing daily under naval protection. For e-commerce sellers, this 10-20 day reduction directly improves inventory turnover and reduces working capital tied up in transit. Sellers can expect normalized delivery windows by Q3 2026 as shipping companies establish stable routing patterns and insurance markets stabilize.

How much will shipping costs decrease for sellers using the Strait of Hormuz corridor?

Shipping costs are expected to decrease 12-18% for sellers using sea freight from Asia-Pacific to Europe/Middle East markets, according to Bloomberg's analysis of the US-Iran ceasefire deal. The three-month closure (February-May 2026) drove insurance premiums substantially higher due to geopolitical risk; reopening with US Navy protection (125+ million barrels moved through secured routes) normalizes these premiums. Sellers should see immediate relief in freight quotes as shipping companies reduce risk surcharges and alternative routing fees. The cost reduction compounds for sellers shipping high-volume, low-margin categories (electronics, apparel, home goods) where sea freight represents 8-15% of COGS.