China Consumer Spending Collapse | Critical Market Shift for Cross-Border Sellers

- Retail sales decline to single digits; Chinese consumers shift to budget products; supply chain disruption risk for sellers sourcing from China

Overview

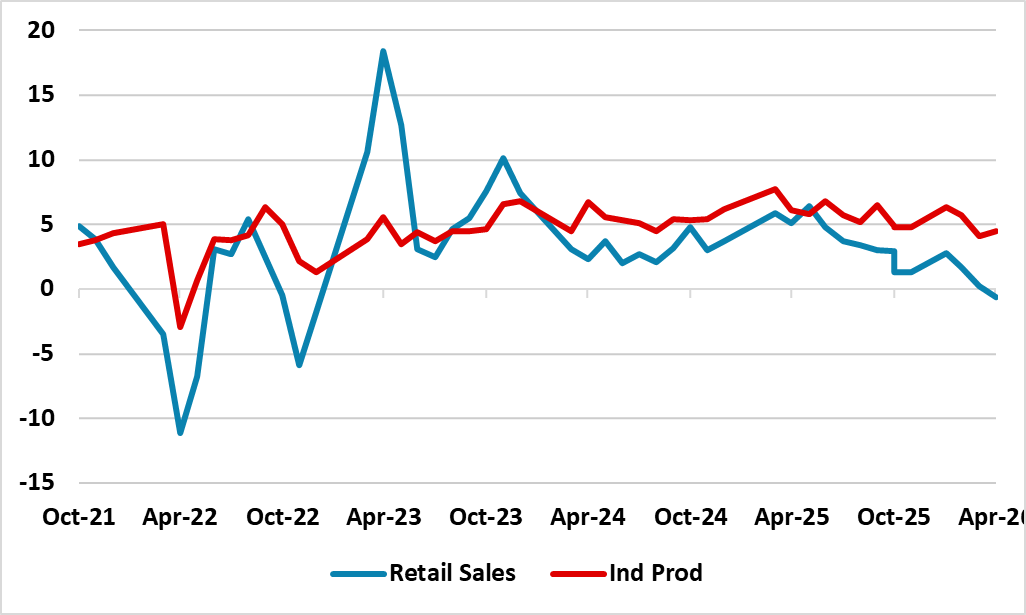

China's consumer spending has entered a structural slowdown that fundamentally reshapes cross-border e-commerce dynamics. Retail sales growth has collapsed to single-digit percentages—with May 2026 marking the first monthly decline (-0.6%) in over three years—signaling a critical market inflection point for sellers. The National Bureau of Statistics data released June 16 reveals a two-speed economy: while industrial output accelerated to 4.5% year-over-year (driven by AI manufacturing and exports), domestic consumption contracted sharply. Fixed-asset investment fell 4.1% in the first five months of 2026, while property investment deepened its contraction to 16.2% year-over-year, destroying the wealth effect that previously fueled consumer spending.

For cross-border sellers, this creates a dual crisis: demand destruction in the Chinese consumer market AND supply-side disruption from Chinese manufacturers. Chinese households are reducing discretionary purchases and increasing savings rates amid property market uncertainties, youth unemployment concerns (8%+ youth jobless rates), and wage growth stagnation. The spending contraction particularly impacts automobiles (eighth consecutive monthly decline), electronics, and fashion retail—categories that generated significant cross-border sales volume. Sellers targeting Chinese buyers should expect 15-25% order volume reductions and intensified price competition as consumers prioritize essential goods over luxury items. Simultaneously, Chinese exporters and manufacturers supplying cross-border platforms face margin compression and inventory buildup, potentially triggering supply chain delays, quality compromises, and supplier bankruptcies through 2025-2026.

The opportunity window exists for sellers offering value-oriented alternatives and essential goods. Budget-friendly product categories (home essentials, practical tools, basic electronics, affordable apparel) are gaining share as Chinese consumers shift from discretionary to necessity-based purchasing. Sellers with cost-competitive sourcing and efficient supply chains can capture market share from premium brands. However, government stimulus measures have shown limited effectiveness in restoring confidence, indicating this slowdown will persist through 2025. Sellers must simultaneously: (1) reduce inventory exposure to Chinese consumer demand; (2) diversify sourcing away from Chinese suppliers facing margin pressure; (3) pivot marketing toward value propositions and discount-driven campaigns; (4) monitor Chinese export surge (high-tech manufacturing +15.1%) for potential trade tensions with Europe that could disrupt supply chains further.

Questions 8

How does China's retail sales decline affect cross-border sellers sourcing from China?

The 0.6% May 2026 retail sales decline—the first monthly drop in over three years—signals severe margin pressure on Chinese manufacturers and exporters. As domestic demand collapses, Chinese suppliers face inventory buildup and cash flow stress, increasing bankruptcy risk and forcing quality compromises to maintain volume. Sellers relying on Chinese sourcing should expect 10-20% longer lead times, minimum order quantity increases, and potential supplier failures through 2026. Diversifying sourcing to Vietnam, India, or Mexico becomes critical to mitigate supply chain disruption risk.

What product categories should sellers prioritize given China's consumer spending slowdown?

Chinese consumers are shifting from luxury and discretionary items (automobiles, high-end electronics, fashion) toward essential goods and budget-friendly alternatives. Sellers should prioritize: home essentials (cleaning supplies, basic tools), practical electronics (phone accessories, chargers), affordable apparel (basics, workwear), and value-oriented home goods. These categories typically see 8-15% volume growth during consumer spending slowdowns. Avoid inventory buildup in premium categories, which face 20-30% demand destruction as property wealth effects evaporate and youth unemployment (8%+) reduces discretionary spending.