Strait of Hormuz Reopening Cuts Shipping Costs 8-15% for Cross-Border Sellers by Mid-2026

- Major banks slash oil forecasts to $70-85/barrel; FBA fulfillment costs decline $150-400/month for high-volume sellers; recovery timeline accelerates to July 2026

Overview

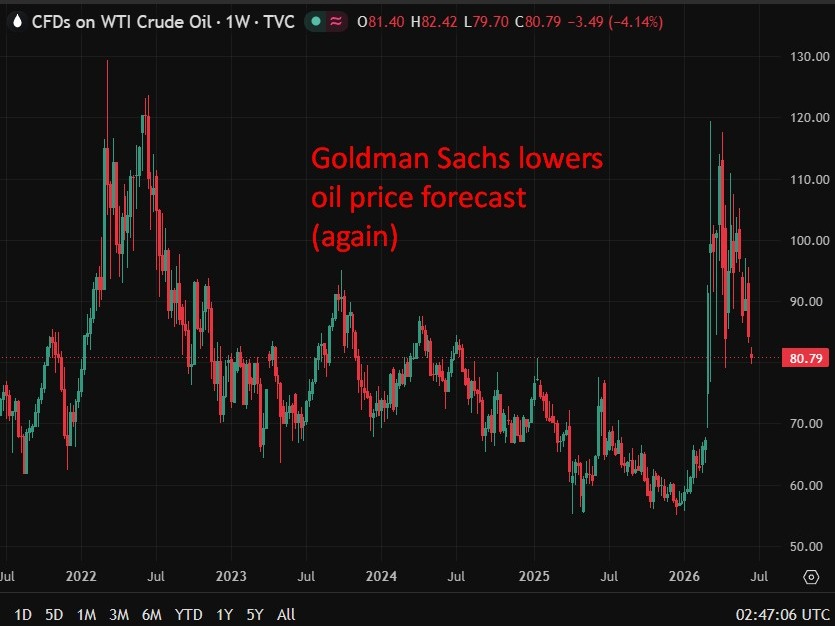

The U.S.-Iran breakthrough agreement and reopening of the Strait of Hormuz represents a transformative logistics cost opportunity for global e-commerce sellers. Major Wall Street banks—Morgan Stanley, Goldman Sachs, and Citibank—have slashed Brent crude oil forecasts to $70-85 per barrel by 2026-2027, down from previous $90-100 estimates. This 10-20% price reduction directly translates to lower transportation costs for cross-border commerce, with tanker traffic through the Strait expected to recover fully by end of July 2026, accelerating supply recovery timelines by approximately one month ahead of previous projections.

For Amazon FBA sellers, Shopify merchants, and 3PL-dependent businesses, this creates immediate cost relief opportunities. Energy-intensive fulfillment operations—including warehousing, last-mile delivery, and international shipping—will experience margin expansion as fuel surcharges decline. Sellers shipping high-volume inventory (1,000+ units monthly) to US, EU, and Asia-Pacific fulfillment centers can expect FBA shipping cost reductions of $150-400 monthly by Q3 2026, with gradual improvements beginning mid-2026 as Gulf oil production ramps to 50% recovery by September and 80% by December. Goldman Sachs projects Persian Gulf exports returning to prewar levels as early as late July 2026, with a projected 3.2 million barrel-a-day surplus cushioning price impacts despite potential supply shocks.

However, the recovery timeline carries execution risks requiring seller vigilance. Mine-clearing operations in the Strait, rebuilding shipowner and insurer confidence, and redeploying tankers currently positioned in alternative routes will extend full normalization into early 2027. Renewed regional hostilities, shipping disruptions, or nuclear negotiation failures could reverse gains—Iran could effectively close the Strait again if talks collapse. Sellers should monitor three critical indicators: (1) weekly Brent crude spot prices (currently below $82/barrel, down 10%+ from prior week), (2) tanker utilization rates through Hormuz (currently 50% of normal levels as of mid-June), and (3) 3PL provider fuel surcharge announcements, which typically lag commodity prices by 4-6 weeks.

Strategic sellers should capitalize on this 6-12 month window before competitors adjust pricing and inventory strategies. Categories with high logistics costs—electronics, home goods, sporting equipment, and heavy machinery—will see the most dramatic margin improvements. Sellers currently using premium 2-day or expedited shipping can shift to standard fulfillment without sacrificing delivery windows, directly improving profitability. The timing advantage favors sellers who lock in current 3PL contracts before Q3 2026, as providers will likely increase rates once fuel cost savings materialize and demand normalizes.

Questions 8

What product categories benefit most from lower shipping costs?

**Electronics, home goods, sporting equipment, and heavy machinery** experience the highest absolute shipping cost reductions due to weight-based pricing and energy-intensive manufacturing. A 10-15% fuel cost decline translates to $2-8 per unit savings for heavy items (furniture, appliances) and $0.50-2 per unit for lighter goods (apparel, accessories). Sellers in these categories can either improve margins by 5-8% or reduce prices to gain market share during the 6-12 month window before competitors adjust. Conversely, sellers in low-margin categories like apparel and accessories should focus on volume optimization rather than price reductions, as absolute savings per unit remain modest ($0.10-0.50).

What risks could delay or reverse the shipping cost improvements?

**Three critical risks could reverse gains: (1) renewed regional hostilities**, which could close the Strait again; (2) **mine-clearing delays**, extending recovery beyond July 2026; and (3) **nuclear negotiation failures**, which could trigger Iranian retaliation. Goldman Sachs notes that Iran could effectively close the Strait if nuclear talks collapse, immediately reversing all cost benefits. Sellers should monitor weekly Brent crude spot prices (currently $79-82/barrel) and tanker utilization rates through Hormuz (currently 50% of normal levels). If prices spike above $90/barrel or tanker flows decline below 40% of normal levels, the recovery timeline has been disrupted. Maintain flexibility in fulfillment strategies and avoid long-term commitments to low-cost logistics providers until full normalization is confirmed in early 2027.