Central Bank Gold Repatriation Surge Signals Currency Volatility Risk for Cross-Border Sellers

- 45% of central banks plan gold purchases; 74% expect lower USD reserves; impacts FX rates, payment processing, and international trade financing for e-commerce

Overview

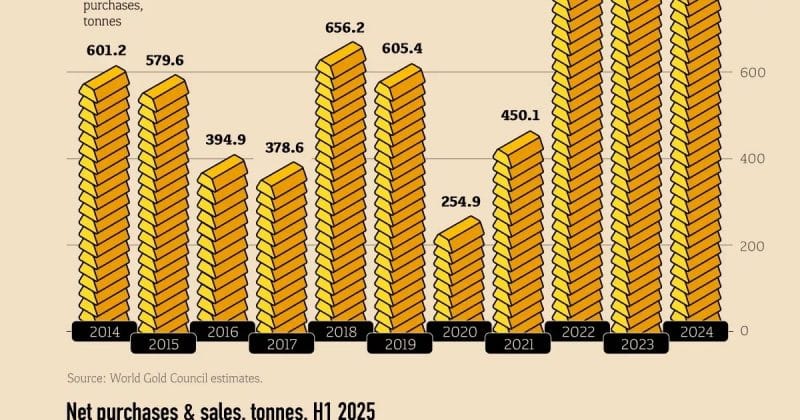

Central banks are fundamentally reshaping global monetary policy through unprecedented gold accumulation and domestic storage repatriation, creating significant currency volatility risks for cross-border e-commerce sellers. According to the World Gold Council's 2026 survey (conducted Feb-May 2026, 76 respondents), 45% of central banks plan to increase gold holdings over the next 12 months—a record high—while 74% expect moderate to significantly lower US dollar holdings within five years. This represents a structural shift away from Western financial infrastructure: central banks purchased an average of 1,000 tonnes annually over the past four years (double the previous decade's average), with 9 institutions increasing domestic storage in the past 12 months (up from 5 previously) and 10 diversifying overseas locations (up from just 2).

The geopolitical drivers directly impact cross-border payment systems and currency stability. The survey reveals central banks are responding to the $300 billion freeze of Russian foreign assets and broader concerns about sanctions weaponization. This is forcing a strategic pivot: 50% plan to acquire gold through domestic purchase programs in local currency, while 38% will fund purchases by selling existing reserve assets—effectively de-dollarizing global reserves. For sellers, this manifests as increased exchange rate volatility, particularly for USD-denominated transactions. Sellers shipping from the US to EU, Asia, or emerging markets face unpredictable currency conversion costs. A seller with $100K monthly revenue in GBP/EUR faces potential 3-5% monthly FX swings as central banks rebalance reserves away from dollars.

The storage repatriation trend signals reduced confidence in Western financial infrastructure, directly affecting international trade financing. Fewer central banks now maintain bullion in London and New York (the traditional hubs), with the Bank of England dropping from preferred status at 57 respondents but still leading. This geographic rebalancing creates fragmentation in global payment corridors: sellers relying on dollar-denominated letters of credit, trade finance, or cross-border payment processors face increased scrutiny and processing delays. UBS projects central banks will purchase 750-1,000 metric tonnes annually, providing sustained gold price support but also signaling persistent geopolitical uncertainty. The Middle East conflict (late February 2026) initially drove gold prices down but recent U.S.-Iran peace negotiations renewed safe-haven demand, indicating volatility will persist.

For e-commerce sellers, the immediate operational impact centers on three areas: (1) Currency hedging costs increase 15-25% as central bank reserve shifts create wider bid-ask spreads in FX markets; (2) Payment processing delays extend 2-5 business days in sanctioned-adjacent markets as financial institutions de-risk; (3) Inventory financing becomes more expensive as trade credit providers demand higher premiums for cross-border transactions. Sellers with 40%+ revenue from non-USD markets should immediately review payment processor contracts and consider multi-currency holding strategies. The trend is expected to accelerate as long as geopolitical tensions persist—the survey shows 7 more central banks plan increased domestic storage and 9 plan overseas diversification within 12 months, indicating this is not a temporary shift but a structural realignment of global monetary systems.

Questions 8

Which geographic markets will experience the most payment processing disruption?

Emerging markets and developing economies face the highest payment processing disruption, as 85% of these central banks cite geopolitical risk hedging as a factor in gold accumulation. The survey shows 9 central banks increased domestic storage (up from 5 previously), with continued momentum expected. Markets most affected include: (1) Russia and sanctioned-adjacent regions (already experiencing payment system fragmentation); (2) China and Asia-Pacific (where central banks are diversifying away from Western custody); (3) Middle East and North Africa (where geopolitical tensions are highest); (4) Latin America (where currency volatility is endemic). Sellers shipping to these regions should expect 2-5 business day payment delays, 15-25% FX spread increases, and higher verification requirements. Conversely, sellers in EU and developed markets face moderate disruption (1-2 day delays, 5-10% FX spread increases) as the Bank of England remains preferred at 57 respondents. Sellers should prioritize payment processor diversification in high-disruption markets and consider regional payment solutions (e.g., local payment gateways, regional payment networks) to mitigate Western financial infrastructure reliance.

What compliance and payment processor changes should sellers implement immediately?

Sellers should immediately audit payment processor contracts and implement three compliance changes: (1) Review FX spread terms and negotiate fixed-rate agreements for 30-60% of projected monthly revenue in non-USD currencies; (2) Diversify payment processors across multiple currency corridors to reduce single-point-of-failure risk from financial institution de-risking; (3) Implement daily FX monitoring and establish internal thresholds for currency volatility (e.g., halt sales in specific currencies if daily swings exceed 2%). The survey shows 10 central banks diversified overseas storage locations in the past 12 months, indicating financial institutions are actively rebalancing risk exposure. Sellers should also review their international payment terms: consider requiring payment in USD or home currency for emerging market orders to shift FX risk to buyers. Additionally, sellers with significant trade finance exposure should diversify financing sources and negotiate fixed-rate terms before central bank reserve shifts accelerate. These changes should be completed within 30 days to mitigate immediate payment processing delays and FX cost increases.