Walmart's July 2026 Price Cuts Reveal Tariff Arbitrage Opportunity | Sellers Face Margin Compression

- Walmart reduces prices 12-63% on thousands of items amid tariff-driven inflation; sellers must recalibrate pricing strategies on Walmart Marketplace and competing platforms within 30-60 days

Overview

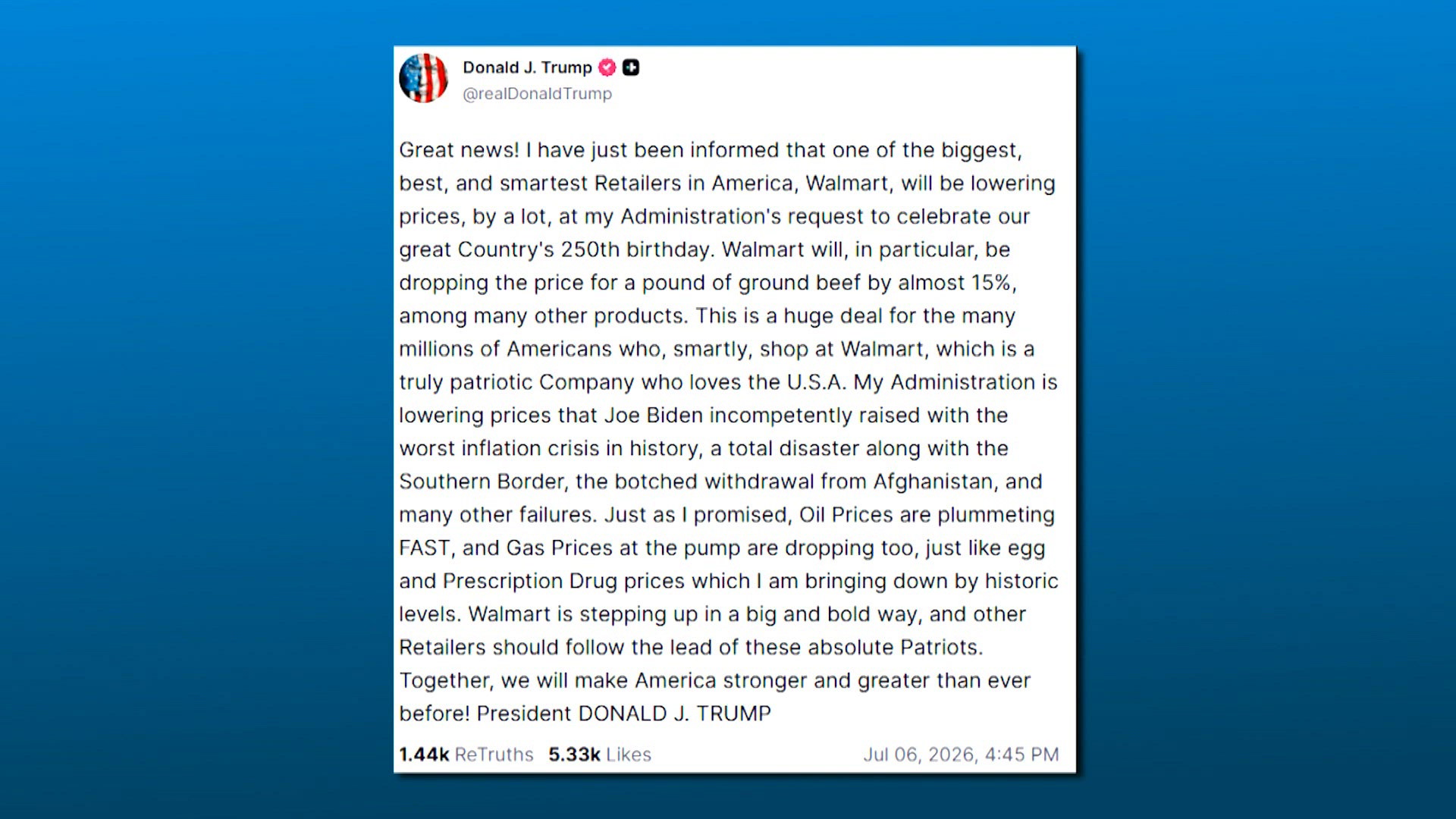

Walmart's July 7, 2026 price reduction initiative across thousands of products—ground beef down 12%, corn 63%, Coca-Cola 33%—signals a critical shift in U.S. retail pricing dynamics driven by tariff policy and supply chain pressures. This announcement follows Walmart's February 2026 price increases on general merchandise due to higher U.S. tariffs on imports, revealing a deliberate tariff arbitrage strategy: absorb tariff costs on essentials (beef, produce) to drive traffic while maintaining margins on imported goods. The underlying economic context is stark: food prices rose 3.1% year-over-year in May 2026, with ground beef prices up 12.8% before Walmart's intervention. The Trump administration's $500 million USDA pledge to support small and midsize meatpackers signals government-backed supply chain intervention, creating a temporary pricing window for retailers willing to absorb margin compression.

For cross-border e-commerce sellers, this creates a three-tier competitive challenge. First, sellers offering competing products on Walmart Marketplace must immediately reassess pricing: Walmart's direct-to-consumer price cuts (ground beef $6.74→$5.94/lb, Coca-Cola 24-pack $14.97→$9.97) establish new price ceilings that marketplace sellers cannot exceed without losing Buy Box eligibility. Second, the 95% consumer perception of an affordability crisis (per Guardian/Harris Poll) means consumers are now price-sensitive across ALL categories, not just groceries—discretionary spending on non-essential items sold through Amazon, eBay, and Shopify will face headwinds as households redirect budgets to essentials. Third, the tariff-driven cost structure creates a sourcing arbitrage opportunity: sellers importing from Vietnam, India, or Mexico (lower tariff rates than China) can undercut competitors still sourcing from China-based suppliers facing 25%+ tariffs on general merchandise.

The operational timeline is compressed. Walmart's price reductions are effective immediately across Walmart.com, SamsClub.com, and 4,600+ physical locations. Sellers have 30-60 days before competing platforms (Amazon, eBay, Shopify) experience cascading price pressure and margin compression. The Consumer Price Index reached its highest level in three years in May 2026, driven by Iran war-related energy costs, but Walmart's strategic pricing suggests the administration is prioritizing visible price relief on staples to manage political narrative around inflation. This creates a window for sellers to: (1) identify which product categories are NOT subject to Walmart's price cuts (specialty items, non-commodity goods), (2) shift inventory sourcing to lower-tariff countries to maintain margins, and (3) reposition on Amazon and other platforms as premium/specialty alternatives rather than competing on price with Walmart's scale advantages.

Strategic sourcing shifts are already underway. The February tariff increases that prompted Walmart's July price cuts indicate sellers should evaluate Vietnam (apparel, electronics), India (textiles, home goods), and Mexico (consumer goods) as alternatives to China sourcing. Tariff rates on these countries are typically 5-15% versus 25%+ on China-origin general merchandise, creating 10-20 percentage point margin recovery opportunities. However, this requires 60-90 day lead time for supply chain reconfiguration. Sellers with existing Vietnam/India relationships can capture market share from competitors still locked into China sourcing. The affordability crisis narrative also signals that value-oriented sellers (budget brands, private label) will outperform premium sellers in the next 6-12 months, suggesting inventory allocation should shift toward lower-price-point SKUs.

Questions 8

How do Walmart's price cuts affect sellers on Walmart Marketplace?

Walmart's July 2026 price reductions establish new price ceilings that directly impact marketplace seller competitiveness. Ground beef reduced to $5.94/lb and Coca-Cola 24-packs to $9.97 mean marketplace sellers offering identical or similar products cannot exceed these prices without losing Buy Box eligibility. Sellers must either absorb margin compression (reducing profit per unit by 8-15%), shift to higher-margin private label alternatives, or exit commodity categories. The announcement affects over 250 items on Sam's Club alone, suggesting Walmart is using price leadership to consolidate market share across essential categories.

What sourcing countries offer tariff advantages over China in 2026?

Vietnam, India, and Mexico offer significant tariff arbitrage opportunities compared to China. Vietnam faces 5-12% tariffs on apparel and electronics versus 25%+ on China-origin general merchandise. India has similar advantages on textiles and home goods (8-15% tariffs). Mexico benefits from USMCA preferential rates (0-5% on many categories). Sellers can recover 10-20 percentage points of margin by shifting sourcing to these countries, though this requires 60-90 day supply chain reconfiguration. The February 2026 tariff increases that prompted Walmart's July price cuts make this shift economically urgent for sellers facing margin pressure.