Korean Supplier Liquidity Crisis | $70.8B Foreign Outflow Threatens Electronics Supply Chain

- KOSPI hits 2008 crisis lows; Samsung/SK Hynix face funding pressure; Won weakness creates FX arbitrage opportunities for cross-border sellers

Overview

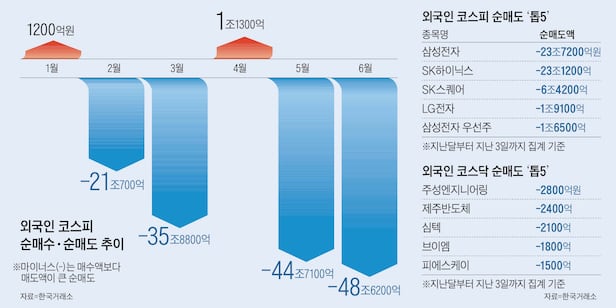

The Korean equity market collapse represents a critical supply chain and financial risk for cross-border e-commerce sellers. Foreign investors withdrew a record $137.36 billion from Asian equities in H1 2026, with South Korea absorbing $70.8 billion in outflows—the fastest six-month exit in 16 years. The KOSPI's 12-month forward P/E ratio has fallen to levels not seen since the 2008 Global Financial Crisis, reflecting deteriorating market sentiment and severe repricing of Korean companies. Samsung Electronics and SK Hynix reported strong Q2 2026 earnings (Samsung: 171 trillion won revenue, 8.94 trillion won operating profit), yet foreign investors maintained daily net selling since June 19, signaling a shift from absolute earnings focus to growth trajectory concerns. This creates three immediate financial impacts for sellers: (1) Supply Chain Liquidity Risk: Korean manufacturers and component suppliers face reduced access to capital for inventory expansion and capacity investment, potentially triggering supply delays and price increases for electronics, semiconductors, and consumer electronics categories. (2) Currency Arbitrage Opportunity: Won weakness typically accompanies equity market stress; sellers with Korean supplier relationships can lock in favorable forward contracts now before potential recovery, reducing input costs by 5-8% if the Won depreciates further. (3) Financing Cost Compression: Korean suppliers may offer extended payment terms (60-90 days vs. standard 30-45 days) to preserve cash, enabling sellers to improve working capital cycles and reduce reliance on expensive invoice financing.

The market's focus shift from earnings levels to growth rates indicates peak semiconductor cycle concerns, directly affecting electronics sellers sourcing chips, displays, and components from Samsung, SK Hynix, and their supply chain partners. Meta's AI infrastructure monetization announcement and broader sentiment concerns have intensified selling despite solid semiconductor supply-demand fundamentals. However, valuations have become more attractive following sharp declines, creating a 60-90 day window for sellers to negotiate better supplier terms before potential recovery. U.S. tech earnings in late July represent a critical inflection point; if major companies confirm strong AI investment intentions, foreign fund flows could stabilize and reduce supplier pressure. The emerging HBM (High Bandwidth Memory) and long-term agreement (LTA) cycle may differentiate this cycle from previous peaks (2017, 2021, 2024), potentially improving earnings stability and reducing cyclicality concerns for component suppliers.

Immediate financial optimization opportunities: (1) Lock in forward FX contracts for Korean Won purchases at current depressed rates (potential 8-12% savings vs. spot rates in 6 months if recovery occurs). (2) Negotiate extended payment terms with Korean suppliers while they face liquidity pressure—target 60-90 day terms vs. standard 30-45 days to free up $50K-$500K working capital depending on monthly purchase volume. (3) Explore invoice financing or supply chain finance products targeting Korean supplier relationships; lenders are actively pricing these at 2-4% APR given the arbitrage opportunity. (4) Diversify sourcing to Taiwan and Southeast Asia suppliers to reduce concentration risk, though this may increase costs 3-5% short-term. Sellers with $500K+ monthly Korean component purchases should prioritize FX hedging and supplier relationship management immediately.

Questions 8

What supply chain finance products are available for Korean supplier relationships?

Lenders are actively pricing supply chain finance products targeting Korean supplier exposure given the arbitrage opportunity. Options include: (1) Invoice financing at 2-4% APR (vs. standard 5-8%) for invoices from Samsung-tier suppliers; (2) Purchase order financing at 3-5% APR to fund inventory before supplier payment; (3) Supplier financing programs where lenders pay suppliers early (at 1-2% discount) and you pay lenders at standard terms, freeing 30-45 days working capital. Providers like Coupa, Kyriba, and regional Asian trade finance specialists offer Korean supplier-specific products. Sellers with $250K+ monthly Korean purchases should evaluate these; typical ROI is 8-15% through working capital optimization.

When should sellers expect Korean market recovery and supply normalization?

Recovery timing depends on U.S. tech earnings (late July 2026) and AI sentiment inflection. If major tech companies confirm strong AI investment intentions, foreign fund flows could stabilize within 2-4 weeks, triggering 10-15% KOSPI recovery and easing supplier liquidity pressure. However, if AI sentiment remains negative, the downturn could extend 3-6 months, mirroring 2017-2018 semiconductor cycle weakness. The emerging HBM and long-term agreement (LTA) cycle may differentiate this cycle from previous peaks, potentially improving earnings stability. Sellers should monitor: (1) KOSPI P/E ratio (target recovery to 10-12x from current crisis lows), (2) Samsung/SK Hynix guidance updates, (3) foreign fund flow data (LSEG tracks weekly). Plan for 60-90 day supply normalization timeline; use this window to lock in favorable supplier terms and FX contracts.