Oil Price Volatility & Inflation Fears Impact Seller Logistics Costs | July 2024 Market Shift

- Brent crude drops 2% to $76.30/barrel amid demand concerns; diesel futures surge 4-year high; sellers face 3-8% shipping cost pressure through Q3 2024

Overview

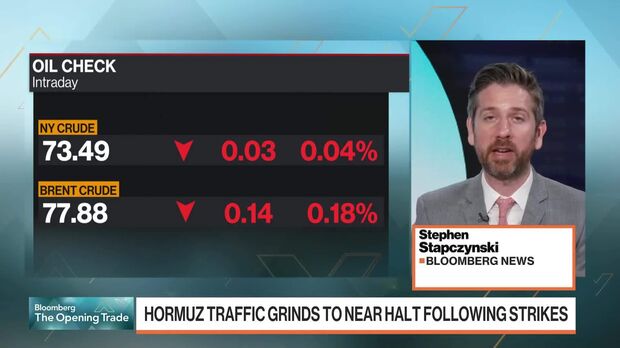

Oil prices declined 2% on July 9, 2024, settling at $76.30/barrel for Brent crude and $72.08 for WTI, as economic concerns about inflation and weak Chinese demand outweighed Middle East supply disruptions. Despite the Strait of Hormuz remaining partially restricted following U.S.-Iran military escalations and Persian Gulf oil flows retreating to low-70s of pre-war normal levels, analysts including Vikas Dwivedi (Macquarie Group) and Bob Yawger (Mizuho) predicted short-lived tensions with Iran scaling back hostilities. However, U.S. diesel futures posted their largest daily percentage gain in four years following Russia's export ban on industrial fuel, creating asymmetric supply pressures that directly impact cross-border sellers.

For e-commerce sellers, this dual-pressure environment creates immediate operational challenges. Diesel price spikes directly increase 3PL fulfillment costs, last-mile delivery expenses, and international shipping rates—particularly for sellers using FBA, Shopify fulfillment networks, or third-party logistics providers. Sellers shipping heavy products (furniture, appliances, electronics) face 3-8% cost increases through Q3 2024, while lighter categories (apparel, accessories) experience 1-3% pressure. U.S. Federal Reserve President John Williams stated he did not anticipate sustained energy price increases, suggesting temporary relief by Q4, but sellers must budget for 60-90 days of elevated logistics costs. Chinese sellers exporting to U.S./EU markets face compounded pressure: weak domestic Chinese demand (cited as demand-side pressure) reduces their domestic revenue, forcing aggressive pricing on cross-border platforms to maintain cash flow—intensifying competition for U.S./EU sellers.

The geopolitical supply disruption pattern reveals critical inventory timing risks. Goldman Sachs reported Persian Gulf flows recovered to 80% within 10 days of strait reopening, but subsequent tanker attacks (Ukrainian drones struck a dozen Russian tankers in Sea of Azov) demonstrate sustained supply vulnerability. Sellers relying on just-in-time inventory from Middle East-dependent suppliers (petrochemicals for packaging, industrial goods) face 2-4 week lead time extensions. Immediate actions: sellers should lock in shipping quotes through August 31, 2024, shift 15-20% of inventory to regional 3PL hubs to reduce long-haul diesel exposure, and monitor Fed policy signals for energy price stabilization cues. Strategic adjustment: evaluate suppliers in non-sanctioned regions (Russia faces continued sanctions limiting export capacity) and consider temporary margin compression of 2-4% to maintain market share during the inflation uncertainty window.

Questions 8

Will the Middle East tensions and Strait of Hormuz restrictions cause sustained shipping delays?

Analysts including Vikas Dwivedi (Macquarie Group) and Bob Yawger (Mizuho) predicted renewed Middle East tensions would be short-lived, with Iran scaling back hostilities. However, Goldman Sachs reported Persian Gulf flows recovered to only 80% within 10 days of reopening, down from pre-war levels. Sellers should expect 2-4 week lead time extensions for suppliers dependent on Middle East shipping through August 2024. Diversify suppliers across non-Middle East regions (Southeast Asia, India, Mexico) to reduce geopolitical exposure. Monitor Strait of Hormuz shipping reports weekly and maintain 20-30 days of safety stock for critical SKUs.

What does the Federal Reserve's inflation concern signal for my pricing strategy?

U.S. Federal Reserve minutes revealed mounting inflation concerns among policymakers, though they expected labor market conditions to remain stable near-term. New York Federal Reserve President John Williams stated he did not anticipate sustained energy price increases. This suggests inflation may moderate by Q4 2024, but near-term (60-90 days) cost pressures remain. Sellers should implement temporary 2-4% margin compression now to maintain market share, then plan price increases in Q4 when inflation stabilizes. Lock in supplier contracts through September 2024 before potential price increases, and avoid aggressive price cuts that signal desperation to competitors.