$43.24B Automotive Leather Market Boom | Vegan & Bio-Based Materials Drive 6% Growth Through 2030

- Sustainable leather alternatives create $8.6B+ new market opportunity for cross-border sellers; Hyundai's bio-based innovation signals regulatory shift affecting 50K+ automotive aftermarket suppliers globally

Overview

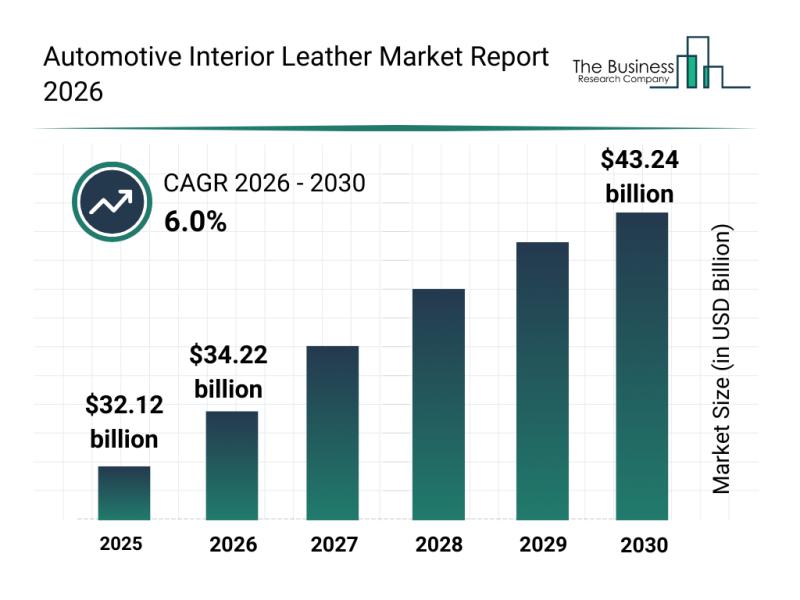

The global automotive interior leather market is experiencing a transformative shift toward sustainability, with projections reaching $43.24 billion by 2030 at a 6.0% compound annual growth rate (CAGR). This expansion directly impacts cross-border e-commerce sellers through emerging product categories, supply chain consolidation, and regulatory compliance requirements. The market is being reshaped by four critical forces: stricter sustainable material regulations, electric vehicle interior upgrades, vegan leather adoption, and smart trim technology integration.

For cross-border sellers, this represents a $8.6B+ incremental market opportunity (calculated from 2030 projection minus current baseline). The August 2023 acquisition of Roadwire by Katzkin signals industry consolidation, indicating that smaller suppliers must differentiate through specialization. More significantly, Hyundai's August 2025 bio-based faux leather project using wheat, soy, and corn proteins demonstrates that major OEMs are actively developing plant-based alternatives—creating urgent demand for compatible aftermarket products, customization services, and material suppliers on Amazon, eBay, and specialty automotive marketplaces.

Seller segments most affected include: (1) Automotive aftermarket retailers selling seat covers, upholstery, and interior trim kits—who must pivot inventory toward synthetic and vegan leather options; (2) Material suppliers and wholesalers sourcing polyurethane, PVC, biodegradable variants, and microfiber materials for resale; (3) Customization service providers offering premium interior upgrades for luxury and mid-segment vehicles; (4) Sustainability-focused brands positioned to capture eco-conscious consumers willing to pay 15-25% premiums for certified vegan leather products.

The regulatory environment is tightening globally. Stricter sustainability regulations are forcing traditional leather suppliers to invest in alternative materials, creating supply chain gaps that nimble e-commerce sellers can exploit. The shift toward lightweight interior components for electric vehicles adds another layer—EV manufacturers prioritize weight reduction for battery efficiency, creating demand for lighter synthetic materials that cross-border sellers can source from Asia-Pacific manufacturers and distribute globally.

Key market segments by application: seats (highest volume), center stack, upholstery, and door panels. The convergence of consumer demand for eco-friendly options, regulatory pressure, and technological advancement in smart trim components (sensors, electronics) indicates sustained growth potential through 2030. Sellers who establish supply chains for bio-based and vegan leather alternatives now will capture first-mover advantage as OEM adoption accelerates.

Questions 8

What are the risks for sellers in the automotive leather market?

Key risks include: (1) **Regulatory compliance**—stricter sustainability standards may require product reformulation or certification; (2) **Supply chain consolidation**—major acquisitions like Katzkin-Roadwire may reduce supplier options; (3) **Technology disruption**—rapid innovation in bio-based materials may obsolete current product lines; (4) **Price volatility**—raw material costs for vegan leather alternatives may fluctuate; (5) **Market concentration**—leading companies (Magna, Faurecia, Lear) dominate OEM supply chains, limiting direct sales opportunities. Sellers should monitor regulatory developments, diversify supplier relationships, and invest in R&D for emerging materials. The shift toward sustainability is irreversible, so sellers must commit to product innovation. Smaller sellers may face margin compression as larger competitors scale. Consider strategic partnerships or niche specialization to maintain competitive advantage in a consolidating market.

How can sellers source vegan leather materials for cross-border e-commerce?

Cross-border sellers can source vegan leather materials from Asia-Pacific manufacturers specializing in polyurethane, PVC, biodegradable variants, and microfiber production. Major suppliers include companies in China, Vietnam, and India that produce synthetic leather materials at scale. Sellers should establish relationships with manufacturers offering certifications for sustainable and eco-friendly materials, as these command premium pricing. The Katzkin acquisition of Roadwire in August 2023 demonstrates industry consolidation, suggesting sellers should diversify supplier relationships to mitigate supply chain risk. Wholesale platforms like Alibaba and Global Sources offer access to material suppliers. Sellers should negotiate volume discounts and establish quality control processes to ensure consistent product standards. Consider partnering with logistics providers specializing in automotive parts to optimize shipping costs and delivery times to major markets.