Monday.com Stock Collapse Signals SaaS Disruption Risk | E-Commerce Sellers Face Operational Platform Uncertainty

- 21% stock decline despite revenue beat reveals AI disruption fears; sellers must evaluate workflow automation alternatives and diversify operational dependencies

/Women%20sitting%20on%20roling%20chair%20in%20front%20of%20computer%20monitors%20by%20ThisisEngineering%20via%20Unsplash.jpg)

Overview

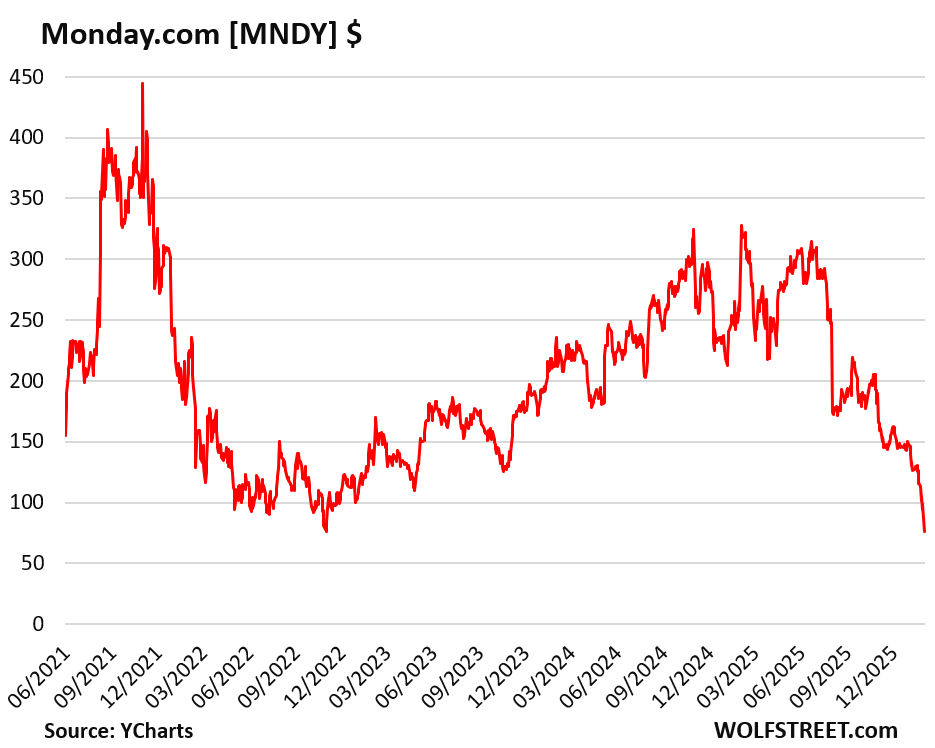

Monday.com's paradoxical Q4 2025 earnings report—beating revenue expectations at $333.9M (+25% YoY) while experiencing a devastating 21% stock decline—exposes critical vulnerabilities in traditional SaaS business models that directly impact e-commerce sellers relying on workflow automation platforms. The company achieved $1.232B in annual revenue (27% YoY growth) with strong enterprise metrics including 1,756 customers with $100K+ ARR (45% increase) and 116% net dollar retention in enterprise segments. However, management's weak 2026 guidance ($1.452-1.462B, representing only 18-19% growth versus expected 19-20%) triggered institutional selling, with the stock losing 47% year-to-date and 75% from its November 2021 peak.

The core issue: AI disruption is fundamentally reshaping software customer acquisition. Co-CEO Roy Mann disclosed a "choppy sales environment" particularly affecting smaller customers through self-serve channels, where customer acquisition costs have surged while ROI has collapsed. William Blair analyst Arjun Bhatia attributed this to "disruption in search engine marketing"—specifically, AI agents and Google AI Overviews are replacing traditional SEO-driven discovery mechanisms. This signals that software companies dependent on self-serve, no-touch sales channels face existential threats as AI reshapes how business users discover and evaluate tools. Monday.com's touch sales (human-driven) remain healthier, suggesting direct sales channels are more resilient to AI disruption.

For e-commerce sellers, this creates three immediate operational risks: First, Monday.com's margin pressure (11-12% non-GAAP operating margins in 2026 guidance versus 14% in 2025) may force feature development slowdowns or pricing increases, affecting sellers' workflow automation capabilities. Second, the company's strategic pivot to emphasize AI-native features (monday vibe achieved $1M ARR in 2.5 months, the fastest product adoption in company history) indicates management is racing to compete with AI-powered alternatives—but investor skepticism suggests this pivot may be insufficient. Third, the broader SaaS sector weakness (iShares Expanded Tech-Software ETF down 22% YoY) indicates this isn't isolated to Monday.com; competitors like Asana, Smartsheet, and Atlassian face similar pressures, creating platform instability across the entire workflow automation ecosystem.

Immediate seller implications: E-commerce teams using Monday.com for supply chain coordination, inventory management, and cross-border team collaboration should immediately audit their dependency on this platform. The 21% stock decline and heavy institutional selling (IBD Accumulation-Distribution Rating of D) signal potential strategic pivots, feature deprecation, or acquisition risk. Sellers should evaluate alternative platforms (Asana, Microsoft Project, Jira) and consider diversifying workflow automation across multiple tools to reduce single-platform risk. The company's foreign exchange headwinds (100-200 basis points margin pressure) may also affect pricing for international sellers. Most critically, the shift from self-serve to touch sales suggests Monday.com will increasingly focus on enterprise customers, potentially deprioritizing SMB seller needs—the core user base for cross-border e-commerce operations.

Questions 8

Should e-commerce sellers diversify away from Monday.com immediately or wait for strategic clarity?

Immediate diversification is prudent given the 21% stock decline, 47% year-to-date loss, and heavy institutional selling (IBD Accumulation-Distribution Rating of D). While Monday.com's enterprise metrics remain strong (116% net dollar retention, 45% growth in $100K+ ARR customers), the company's weak SMB guidance and self-serve channel collapse directly threaten smaller e-commerce sellers. Rather than abandoning Monday.com entirely, sellers should: (1) Audit critical workflows and identify which can migrate to alternatives; (2) Evaluate 2-3 backup platforms for supply chain, inventory, and team collaboration; (3) Monitor Monday.com's Q1 2026 earnings (guidance: $338-340M revenue) for signs of stabilization; (4) Avoid new feature dependencies on Monday.com until strategic clarity emerges. The company's $735M remaining share buyback authorization suggests management confidence, but this doesn't offset investor concerns about competitive positioning against AI-powered alternatives.

Why did Monday.com stock drop 21% despite beating Q4 revenue expectations?

Monday.com's stock decline reflects weak 2026 guidance ($1.452-1.462B versus expected $1.48B) and margin compression (11-12% non-GAAP operating margins versus 14% in 2025). Management disclosed a 'choppy sales environment' with collapsing ROI in self-serve customer acquisition channels due to AI disruption in search engine marketing. Investors fear the company cannot adapt quickly enough to compete with AI-powered alternatives, making it a 'poster child for the AI-killing-software narrative' according to Mizuho analyst Jordan Klein. The stock has lost 47% year-to-date and 75% from its November 2021 peak, indicating broader SaaS sector weakness.