Copper Prices Must Double by 2030 | Critical Supply Shortage Reshapes Electronics & EV Supply Chains

- University of Michigan study projects 37-92M ton annual demand by 2050 vs. 23M current production; sellers in electronics, hardware, and EV components face 15-25% COGS increases within 24 months

概览

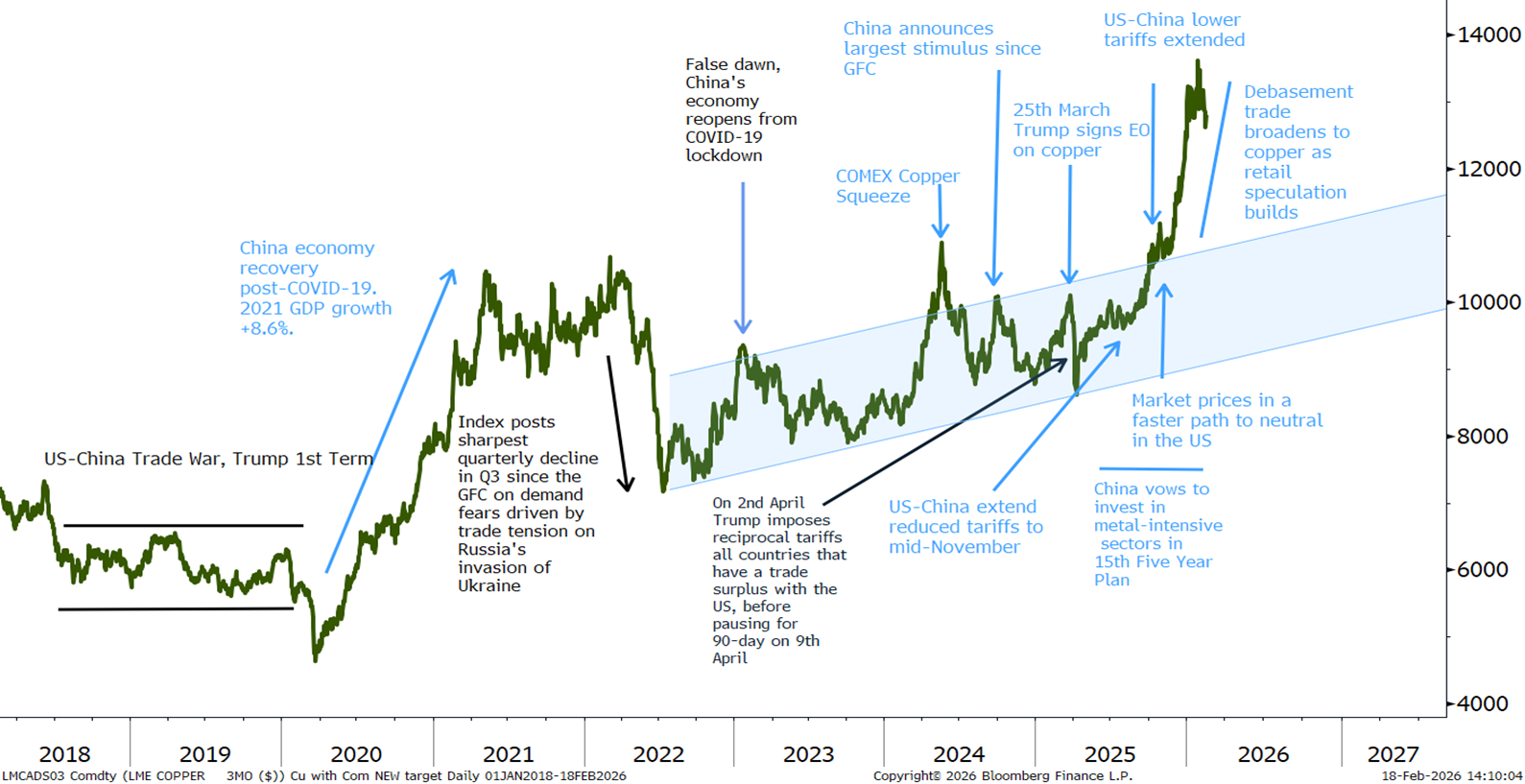

A University of Michigan-led research team has determined that copper prices must at least double from current levels of approximately $13,000 per ton to stimulate development of new mines necessary to meet global demand through 2050. Published in Energy Research & Social Science, the analysis reveals a critical supply-demand mismatch: annual copper requirements will surge from 23 million tons in 2025 to 37 million tons by 2050 under standard business scenarios, with renewable energy and electric vehicle adoption potentially driving demand to 91.7 million tons annually. The research examined project data from mining operations in Mongolia ($18,916/ton development cost), Panama ($31,318/ton), and the United States ($29,614/ton), finding that new copper mine development typically costs over $22,000 per ton of annual output—substantially exceeding current market prices. Co-author Adam Simon emphasized that "the world is not running out of copper; it is running out of time to produce it," highlighting the critical timeline challenge.

For cross-border e-commerce sellers, this supply constraint creates immediate cost pressures across multiple product categories. Copper is essential in electronics manufacturing (HS codes 8504-8548: electrical machinery, transformers, motors), packaging materials (HS 7410: copper foil, sheets), and logistics infrastructure (shipping containers, handling equipment). Rising copper costs will increase product sourcing expenses for sellers dealing in electronics, hardware, power tools, telecommunications equipment, and items requiring copper components. Sellers sourcing from Asia-Pacific regions (Vietnam, India, China) will face 15-25% COGS increases within 24 months as manufacturers pass through commodity cost inflation. Additionally, higher copper prices affect shipping container production and logistics equipment costs, potentially impacting fulfillment expenses by 8-12% for sellers using 3PL providers. The research identifies that recycling could provide only 13.4 million tons by 2050 (roughly one-third of basic needs), while mining low-grade ore and leaching copper from mining residues could contribute an additional 4 million tons annually—insufficient to bridge the gap.

Strategic sourcing shifts are already underway. Manufacturers in India and developing nations face particular challenges, as copper infrastructure per capita remains critically low compared to high-income nations. This geographic inequality creates opportunities for sellers to source from alternative suppliers in regions with lower copper-intensive production (aluminum substitutes, plastic components) before prices spike further. The research team advocates for accelerated mining approvals and more predictable regulatory processes without compromising environmental or community protections. Current permitting processes require years or decades for mine approval, creating temporal bottlenecks. Twenty-six new copper mines expected to begin operations by 2030 will average $22,359 per ton in development costs. Without substantial policy changes and public support for mining expansion, global climate goals and infrastructure development will face severe constraints, directly impacting the EV and renewable energy sectors that drive demand for copper-intensive products.

問題 7

How much will copper prices increase and when will sellers see cost impacts?

University of Michigan research indicates copper prices must double from current $13,000/ton levels to approximately $26,000/ton to incentivize new mine development. This price doubling is necessary by 2030 to meet 37 million ton annual demand (vs. current 23 million tons). Sellers in electronics, hardware, and EV components will experience 15-25% COGS increases within 12-24 months as manufacturers pass through commodity inflation. For a seller sourcing $100,000 monthly in copper-intensive electronics, this translates to $15,000-25,000 additional monthly costs. The timeline is critical: 26 new copper mines averaging $22,359/ton development costs are expected to begin operations by 2030, but current permitting delays of years or decades create supply bottlenecks.

Which product categories face the highest copper cost exposure?

Copper-intensive product categories include: (1) Electronics & Electrical Machinery (HS 8504-8548): transformers, motors, power supplies, telecommunications equipment—typically 5-15% copper content; (2) Hardware & Tools (HS 7307-7326): fasteners, fittings, plumbing supplies—2-8% copper; (3) EV Components (HS 8704-8708): charging infrastructure, wiring harnesses, battery terminals—8-12% copper; (4) Packaging Materials (HS 7410): copper foil, sheets, laminates—high copper concentration. Sellers in these categories should anticipate 15-25% COGS increases. Conversely, sellers in apparel, furniture, and non-electrical goods face minimal direct copper exposure but may see 8-12% indirect cost increases through logistics (shipping containers, handling equipment) and 3PL fulfillment fees.