Chinese Memory Chip Arbitrage Collapse | DDR4/DDR5 Sourcing Strategy Overhaul for PC Component Sellers

- Geographic pricing parity eliminates $50-150/unit margin advantage; DDR4 contracts surge 800% YoY to $11.50/8Gb; CXMT reallocates 20% capacity to HBM3, forcing seller sourcing pivot by H2 2025

概览

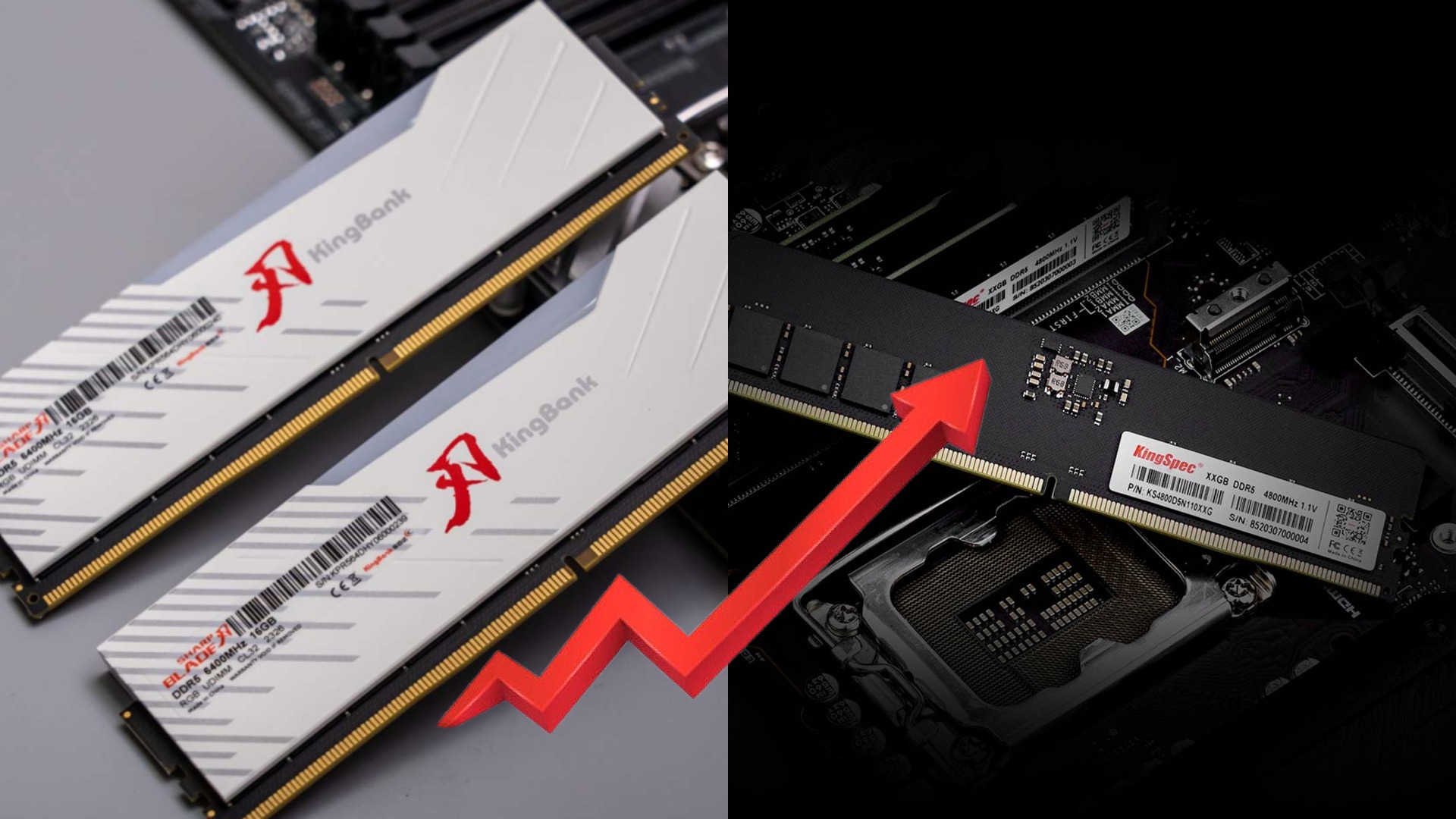

The semiconductor memory market has undergone a fundamental structural shift that eliminates the geographic arbitrage strategy that previously defined profitability for cross-border e-commerce sellers sourcing computer components. Chinese RAM pricing has converged with global market rates, with CXMT's KingBank DDR5-6000 32GB modules now retailing at 3,629 yuan ($530 USD) on JD.com—matching Western prices from G.Skill, Kingston, and Corsair. This represents a complete collapse of the cost-reduction advantage that attracted sellers to Chinese memory imports over the past 3-5 years.

The root cause stems from AI infrastructure consolidation by OpenAI, Google, and Meta, which have secured exclusive long-term agreements (LTAs) with Samsung, SK Hynix, and Micron for high-bandwidth memory (HBM) production. This cascade effect has halted consumer DDR5 production entirely, causing retail prices to surge 4.3x in three months (October 2025: $115→$490 for G.Skill Trident Z Neo DDR5-6000 CL30 32GB kits). Simultaneously, CXMT is strategically reallocating production capacity away from consumer memory—converting approximately 60,000 wafers monthly (20% of Shanghai plant capacity) to HBM3 production, with mass production targeted for 2026. This supply reallocation is driven by enterprise profit margins that substantially exceed consumer-segment returns, leaving minimal incentive for competitive pricing.

For sellers in the PC components, gaming peripherals, and pre-built systems categories, this creates a critical sourcing crisis. Legacy DDR4 pricing presents a temporary tactical opportunity: CXMT is aggressively pricing DDR4 8Gb chips at approximately 50% below market rates (DRAMeXchange data shows contracts averaged $11.50 by January 2025, up 23.7% month-over-month and 800% year-over-year since January 2024—the highest level since June 2016). HP, Dell, Asus, and Acer are conducting quality evaluations of CXMT DDR4 products, indicating OEM validation. However, this advantage is temporary and limited to legacy segments; DDR5 remains supply-constrained with minimal pricing flexibility.

The competitive landscape is shifting dramatically: YMTC has captured 10% global NAND flash market share in 2024 through competitively-priced mobile products and is constructing a third fabrication plant in Wuhan with capacity allocated to legacy DRAM and potential HBM expansion. Apple is evaluating CXMT and YMTC as alternative suppliers to reduce Samsung/SK Hynix/Micron dependence, which will further strain consumer availability. The "RAMaggedon" shortage is expected to persist through 2026 as major suppliers prioritize higher-margin AI infrastructure contracts. Sellers should recognize that geographic arbitrage on memory products is no longer viable for DDR5, and DDR4 opportunities exist only through direct OEM partnerships or bulk enterprise contracts—not through consumer retail channels.

問題 7

What is the current opportunity for sellers sourcing DDR4 memory from China?

CXMT is aggressively pricing legacy DDR4 8Gb chips at approximately 50% below market rates, with DRAMeXchange contracts averaging $11.50 by January 2025 (up 800% year-over-year since January 2024). HP, Dell, Asus, and Acer are conducting quality evaluations of CXMT DDR4 products, indicating OEM validation. However, this advantage is limited to bulk enterprise contracts and direct OEM partnerships—not consumer retail channels. Sellers should prioritize DDR4 sourcing through direct manufacturer relationships rather than consumer distribution, as CXMT is converting 20% of Shanghai plant capacity to HBM3 production by H2 2025.

How long will the DDR5 memory shortage and high prices persist?

Industry analysts expect the 'RAMaggedon' shortage to continue through 2026 as major suppliers (SK Hynix 34%, Samsung 33%, Micron 26%) prioritize higher-margin AI infrastructure contracts over consumer-grade memory production. CXMT's HBM3 mass production is targeted for 2026, and new consumer DDR5 capacity is unlikely until AI demand stabilizes or manufacturers complete capacity expansion. Sellers should plan for sustained supply constraints and elevated pricing through at least mid-2026. The only relief mechanism is if CXMT successfully scales HBM3 production and reallocates excess DDR5 capacity, but current timelines suggest this remains distant.